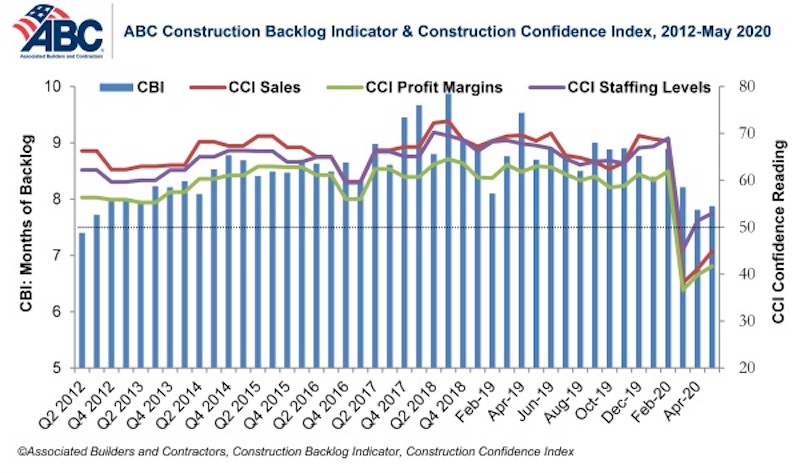

Construction Backlog Indicator rose to 7.9 months in May, an increase of less than 0.1 months from April’s reading. Furthermore, based on an ABC member survey conducted May 20-June 3, results indicate that confidence among U.S. construction industry leaders continued to rebound from the historically low levels observed in the March survey.

Nonresidential construction backlog is down 0.8 months compared to May 2019 and declined year over year in every industry, classification and region. Backlog in the heavy industrial category, however, increased by nearly one month in May after reaching its lowest level in the history of the series in April.

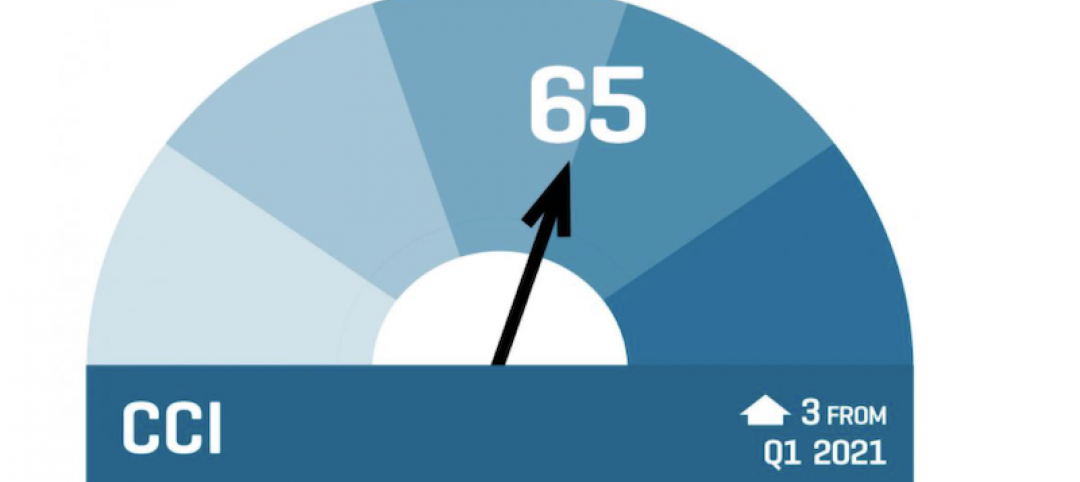

ABC’s Construction Confidence Index readings for sales, profit margins and staffing levels expectations all increased in May, although sales and profit margin expectations remain below the threshold of 50, indicating ongoing anticipation of contraction. The staffing level index remained above that threshold, with more than 38% of contractors expecting to expand their staff during the next six months.

More than 45% of contractors expect their sales to decline during the next six months while 35% expect sales to increase. More than 48% of contractors expect their profit margins to decrease over the next two quarters.

- The CCI for sales expectations increased from 41.1 to 44.9 in May.

- The CCI for profit margin expectations increased from 39.8 to 41.7.

- The CCI for staffing levels increased from 51.4 to 53.

“Given the depth of the economic downturn and myriad other issues facing America today, backlog and contractor confidence data have held up better than one might have anticipated,” said ABC Chief Economist Anirban Basu. “But the marketplace is still tilted toward pessimism. For instance, more contractors expect sales and profit margins to decline than increase over the next six months, which is consistent with anecdotal information suggesting that many project owners are considering postponing projects and possibly rebidding them.

“After falling meaningfully in April, backlog remained relatively unchanged in May, hinting at a stable nonresidential construction marketplace,” said Basu. “However, the underlying survey received fewer responses compared to earlier months in the COVID-19 crisis, perhaps suggesting that some contractors are no longer operating at previous capacity, inducing available work to move toward better-positioned contractors. To the extent that these stronger contractors are reflected in the survey, this would tend to bolster average backlog even in the context of a subdued marketplace.

“Contractors still expect to boost staffing levels over the next six months,” said Basu. “But this may simply be a function of jobsites reopening as construction shutdowns end. Almost 70% of respondents had jobsites shut down due to government mandates and other reasons, and with labor shortages in place before the pandemic, contractors may have residual staffing needs. It remains to be seen whether expected employment growth going forward coincides with speedy recovery in overall contractor confidence and backlog.”

Note: The reference months for the Construction Backlog Indicator and Construction Confidence Index data series were revised on May 12 to better reflect the survey period. CBI quantifies the previous month’s work under contract based on the latest financials available, while CCI measures contractors’ outlook for the next six months.

Related Stories

Market Data | Jul 19, 2021

Construction employment trails pre-pandemic level in 39 states

Supply chain challenges, rising materials prices undermine demand.

Market Data | Jul 15, 2021

Producer prices for construction materials and services soar 26% over 12 months

Contractors cope with supply hitches, weak demand.

Market Data | Jul 13, 2021

ABC’s Construction Backlog Indicator and Contractor Confidence Index rise in June

ABC’s Construction Confidence Index readings for sales, profit margins and staffing levels increased modestly in June.

Market Data | Jul 8, 2021

Encouraging construction cost trends are emerging

In its latest quarterly report, Rider Levett Bucknall states that contractors’ most critical choice will be selecting which building sectors to target.

Multifamily Housing | Jul 7, 2021

Make sure to get your multifamily amenities mix right

One of the hardest decisions multifamily developers and their design teams have to make is what mix of amenities they’re going to put into each project. A lot of squiggly factors go into that decision: the type of community, the geographic market, local recreation preferences, climate/weather conditions, physical parameters, and of course the budget. The permutations are mind-boggling.

Market Data | Jul 7, 2021

Construction employment declines by 7,000 in June

Nonresidential firms struggle to find workers and materials to complete projects.

Market Data | Jun 30, 2021

Construction employment in May trails pre-covid levels in 91 metro areas

Firms struggle to cope with materials, labor challenges.

Market Data | Jun 23, 2021

Construction employment declines in 40 states between April and May

Soaring material costs, supply-chain disruptions impede recovery.

Market Data | Jun 22, 2021

Architecture billings continue historic rebound

AIA’s Architecture Billings Index (ABI) score for May rose to 58.5 compared to 57.9 in April.

Market Data | Jun 17, 2021

Commercial construction contractors upbeat on outlook despite worsening material shortages, worker shortages

88% indicate difficulty in finding skilled workers; of those, 35% have turned down work because of it.