Gilbane has released its Spring 2014 edition of the periodic report "Construction Economics: Market Conditions in Construction" (download the full report).

Among the findings from the Executive Summary:

CONSTRUCTION GROWTH IS LOOKING UP

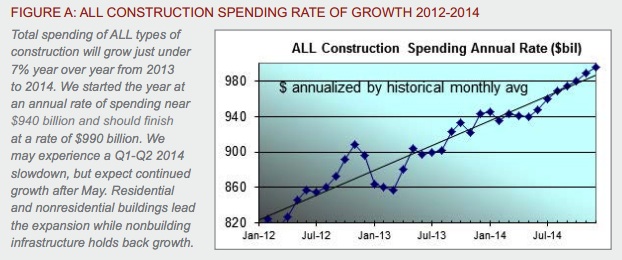

- Construction Spending for 2014 will finish the year 6.6% higher than 2013. Nonresidential buildings will contribute substantially to the growth.

- The Architecture Billings Index (ABI) in 2013 dropped below 50 in April, November and December briefly, indicating declining workload. Overall the ABI portrays a good leading indicator for future new construction work.

- Selling price data for 2013 shows contractors adding to their margins.

- Construction jobs grew by 156,000 in 2013, less than anticipated. However, hours worked also grew by 3%, the equivalent of another 150,000+ jobs.

SOME ECONOMIC FACTORS ARE STILL NEGATIVE

- We are experiencing a slight slowdown in construction spending that could last through May, influenced by a slight dip in nonresidential buildings and a brief flattening in residential, but more so by a steep decline in nonbuilding infrastructure spending. The monthly rate of spending for nonbuilding infrastructure may decline by 10% through Q3 2014.

- The construction workforce and hours worked is still 22% below the 2006 peak. At peak average growth rates, it will take a minimum of five more years to return to previous peak levels.

- Construction volume is 23% below peak inflation adjusted spending, which was almost constant from 2000 through 2006. At average peak growth rates of 8% per year, and factoring out inflation to get real volume growth, it will take eight more years to regain previous peak volume levels.

- As workload expands in the next few years, a shortage of available skilled workers may have a detrimental effect on cost, productivity and the ability to readily increase construction volume.

THE EFFECTS OF GROWTH

- Construction spending during the first five months of 2013 declined from the rate of spending in Q4 2012. Growth has been inconsistent, even in the booming residential sector, which has seen recent declines. We see more consistent growth in 2014 for buildings.

- As spending continues to increase, contractors gain more ability to pass along costs and increase margins. The growth in contractor margins slowed since last year. However, expected increases in volume should reverse that in 2014.

- ENR’s Third Quarter 2013 Cost Report shows general purpose and material cost indices increased on average about 2% to 2.5% year over year. However, selling price indices increased 4% on average. The difference between these indices is increased margins.

IMPACT OF RECENT EVENTS

- There are several reasons why spending is not rapidly increasing: public sector construction remains depressed as sequestration continues; the government is spending less on schools and infrastructure; lenders are just beginning to loosen lending criteria; consumers are still cautious about increasing debt load, including the consumers’ share of public debt and we may be constrained by a skilled labor shortage.

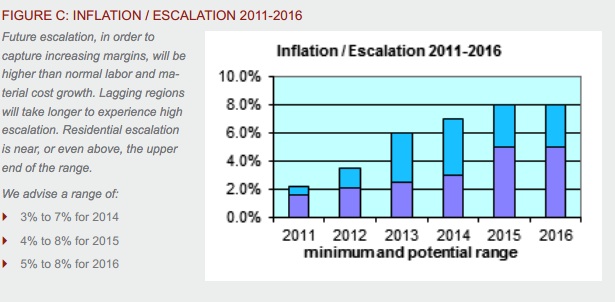

- Supported by overall positive growth trends for year 2014, Gilbane expects margins and overall escalation to climb more rapidly than we have seen in six years.

- Growth in nonresidential buildings and residential construction in 2014 will lead to more significant labor demand, resulting in labor shortages and productivity losses. Margins regained a positive footing in 2012 and extended those gains in 2013. Expect margins to grow stronger in 2014. When activity picks up in all sectors, escalation will begin to advance rapidly.

Click here to download the complete report and a list of data sources.

ABOUT THIS REPORT

Gilbane Inc. is a full service construction and real estate development company, composed of Gilbane Building Company and Gilbane Development Company. The company (www.gilbaneco.com) is one of the nation’s largest construction and program managers providing a full slate of facilities related services for clients in education, healthcare, life sciences, mission critical, corporate, sports and recreation, criminal justice, public and aviation markets. Gilbane has more than 50 offices worldwide, with its corporate office located in Providence, Rhode Island. The information in this report is not specific to any one region.

Related Stories

| Dec 13, 2010

Energy efficiency No. 1 priority for commercial office tenants

Green building initiatives are a key influencer when tenants decide to sign a commercial real estate lease, according to a survey by GE Capital Real Estate. The survey, which was conducted over the past year and included more than 2,220 office tenants in the U.S., Canada, France, Germany, Sweden, the UK, Spain, and Japan, shows that energy efficiency remains the No. 1 priority in most countries. Also ranking near the top: waste reduction programs and indoor air.

| Dec 7, 2010

Are green building RFPs more important than contracts?

The Request for Proposal (RFP) process is key to managing a successful LEED project, according to Green Building Law Update. While most people think a contract is the key element to a successful construction project, successfully managing a LEED project requires a clear RFP that addresses many of the problems that can lead to litigation.

| Dec 7, 2010

Blue is the future of green design

Blue design creates places that are not just neutral, but actually add back to the world and is the future of sustainable design and architecture, according to an interview with Paul Eagle, managing director of Perkins+Will, New York; and Janice Barnes, principal at the firm and global discipline leader for planning and strategies.

| Dec 7, 2010

Green building thrives in shaky economy

Green building’s momentum hasn’t been stopped by the economic recession and will keep speeding through the recovery, while at the same time building owners are looking to go green more for economic reasons than environmental ones. Green building has grown 50% in the past two years; total construction starts have shrunk 26% over the same time period, according to “Green Outlook 2011” report. The green-building sector is expected to nearly triple by 2015, representing as much as $145 billion in new construction activity.

| Dec 7, 2010

USGBC: Wood-certification benchmarks fail to pass

The proposed Forest Certification Benchmark to determine when wood-certification groups would have their certification qualify for points in the LEED rating systemdid not pass the USGBC member ballot. As a result, the Certified Wood credit in LEED will remain as it is currently written. To date, only wood certified by the Forest Stewardship Council qualifies for a point in the LEED, while other organizations, such as the Sustainable Forestry Initiative, the Canadian Standards Association, and the American Tree Farm System, are excluded.

| Dec 7, 2010

Prospects for multifamily sector improve greatly

The multifamily sector is showing signs of a real recovery, with nearly 22,000 new apartment units delivered to the market. Net absorption in the third quarter surged by 94,000 units, dropping the national vacancy rate from 7.8% to 7.1%, one of the largest quarterly drops on record, and rents increased for the second quarter in a row.

| Dec 7, 2010

Hot rumor: Norman Foster designing Apple’s new campus

Lord Norman Foster, reportedly has been selected to design Apple’s new campus in Cupertino, Calif. If the news is true, Foster is a good match for Apple say experts. Foster built his celebrity by marrying big gestures to technological wizardry. And, unlike some starchitects, he has glommed onto the environmental revolution—something Apple has made a point of embracing, too.

| Dec 7, 2010

10 megacities of the near future

With Beijing, Shanghai, and Mumbai already on the global radar, where can the next wave of construction be found? Far beyond China, India, and even Brazil it’s predicted. The world’s next future megacities could include Istanbul, Turkey; Ho Chi Minh City, Vietnam; and Khartoum, Sudan, among others. Read about these emerging and little-known behemoths.