Prices for inputs to construction fell 0.5% in August but are 8.1% higher than at the same time one year ago, according to an Associated Builders and Contractors analysis of Bureau of Labor Statistics data released today. Nonresidential construction input prices fell 0.4% in August but are up 8.3% year-over-year. Softwood lumber prices plummeted 9.6% in August yet are up 5% on a yearly basis (down from a 19.5% increase year-over-year in July).

“Stakeholders will be tempted to look upon this month’s inputs to the construction Producer Price Index report as evidence that the cycle of rapidly rising prices is nearing an end,” said ABC Chief Economist Anirban Basu. “Prices of key inputs have been high for quite some time, which would tend to induce a larger supply of these items and, in turn, moderate prices.

“Some may also conclude that ongoing progress in trade negotiations with nations including Mexico and Canada has helped to moderate input prices. Still others might point to growing economic turmoil in nations like Turkey and Argentina. Economists would also note the likely impact of a strong U.S. dollar on import and commodity prices. While all of these are potential explanations, another possibility is that the August data are largely statistical aberrations. Metal prices continue to move higher on a monthly basis, with recently enacted tariffs representing a likely explanation.

“Softwood lumber, the subject of an ongoing trade dispute with the Canadians, experienced a significant dip in price on a monthly basis,” said Basu. “The price of softwood may have fallen in response to a weakening single-family residential construction market, as home builders have been wrestling with a combination of labor shortages, higher land prices and weakening demand due to higher mortgage rates.

“In the final analysis, the falling input prices trend likely won’t continue,” said Basu. “The economy is still strong, and ABC’s Construction Backlog Indicator remains elevated in both public and private construction segments. Inflation expectations have shifted, with purchasers of construction services now anticipating price increases and therefore more willing to accommodate them. Moreover, issues related to tariffs and trade wars persist. Accordingly, estimators and construction companies continue to consider the likelihood of additional input price increases for the balance of 2018 and into 2019.”

Related Stories

Market Data | Oct 31, 2016

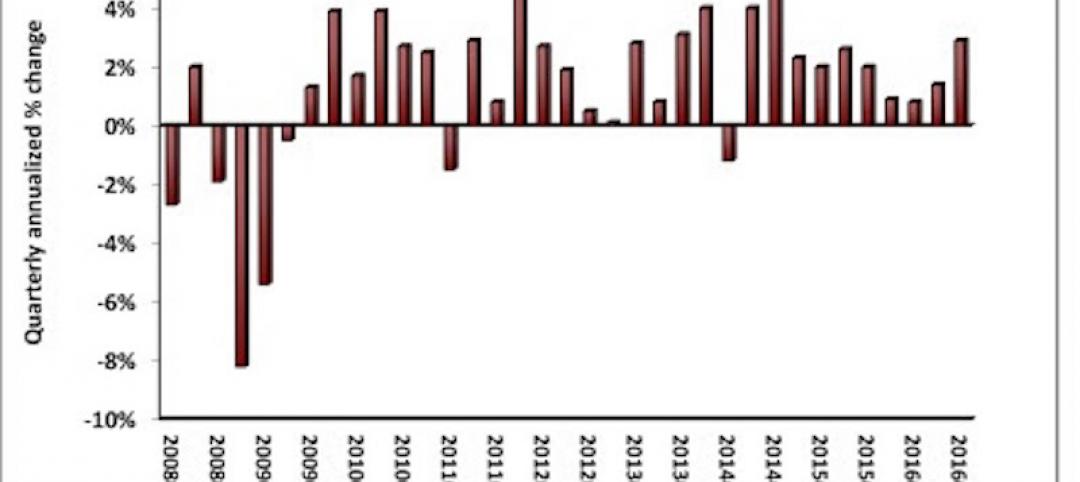

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.

Industry Research | Sep 27, 2016

Sterling Risk Sentiment Index indicates risk exposure perception remains stable in construction industry

Nearly half (45%) of those polled say election year uncertainty has a negative effect on risk perception in the construction market.