The coronavirus has harmed the construction industry, prompting project delays and cancellations, layoffs and furloughs, yet it remains difficult for a majority of firms to find craft workers to hire, according to the results of a workforce survey conducted by the Associated General Contractors of America and Autodesk. The survey paints a picture of an industry in need of immediate recovery measures and longer-term workforce development support, association officials added.

“Few firms have survived unscathed from the pandemic amid widespread project delays and cancellations,” said Ken Simonson, the association’s chief economist. “Ironically, even as the pandemic undermines demand for construction services, it is reinforcing conditions that have historically made it hard for many firms to find qualified craft workers to hire.”

Sixty percent of responding firms report having at least one future project postponed or canceled because of the coronavirus, while 33% report having projects that were already underway halted because of the pandemic. The share of firms reporting canceled projects has nearly doubled since the survey AGC conducted in June, when 32% of respondents reported cancellations.

The coronavirus has also undermined the sector’s productivity levels as firms across the country change the way they operate to protect workers and the public from the disease. Forty-four percent of responding firms report that it has taken longer to complete projects and 32% say it has cost more to complete ongoing projects because of the coronavirus. As a result, 40% report they have adopted new hardware or software to alleviate labor shortages they have experienced.

“The results of the AGC and Autodesk workforce study reveal that the construction industry is still grappling with the changes and consequences of the coronavirus pandemic,” said Allison Scott, director of construction thought leadership and customer marketing at Autodesk. “The long-term effects of the current crisis have yet to play out, and firms that double down on innovation efforts, whether an increased focus on lean construction, workforce training or technology that facilitates remote collaboration will be well poised for enduring resilience.”

The coronavirus has also negatively affected many firms’ confidence in future demand for projects. Only 42% of firms report their volume of business has returned to year-ago levels or is expected to do so in the next six months, compared to 52% who held this view in AGC’s June survey. Another 37% expect returning to normal levels of business will take more than six months, while the remainder don’t know.

While the pandemic has led to project delays and cancellations nationwide, contractor expectations of recovery do vary by region. Forty-five percent of respondents in the Northeast expect it will take more than six months for their firm’s volume of business to return to normal, compared to only 34% of respondents in the West, 35% in the South, and 41% in the Midwest.

There are also some differences by project type and revenue size. For instance, highway and transportation contractors report the greatest difficulty in filling hourly craft positions, with nearly three out of four (73%) reporting an unfilled craft position on June 30. About two-thirds (69%) of utility infrastructure and federal and heavy construction firms had unfilled craft positions then, along with 58% of building construction firms.

Small firms were less likely to have experienced cancellations of upcoming projects. Fifty-six percent of firms with revenues of $50 million or less report a project has been postponed or canceled, compared with 71% of midsized firms (revenue between $50.1 million and $500 million) and 69% of large firms (revenue exceeding $500 million).

Roughly a third of responding firms furloughed or terminated employees as a result of the pandemic and shutdowns ordered by government officials or project owners. Most of those firms have asked at least some laid-off workers to return to work. But 44% of firms that recalled employees report that some have refused to return, citing a preference for unemployment benefits, virus concerns, or family responsibilities, among other reasons.

The pandemic has also made it difficult for many firms to fill open positions, especially for hourly craft jobs. A majority (52%) of respondents report having a hard time filling some or all hourly craft positions, especially openings for laborers, carpenters and equipment operators. Sixty percent of firms had at least one unfilled hourly craft position as of June 30. In addition, 28% of respondents report difficulty filling salaried positions—in particular, project managers and supervisors.

In addition to turning to diverse technologies to alleviate labor shortages, 38% of firms report having increased base pay rates to attract and retain workers. In contrast, only 3% of firms have reduced pay, in spite of the downturn in business.

Construction firms also identified a series of measures that Washington officials could take to help the industry. Fifty-five percent of responding firms, for example, said they were looking to Congress to increase funding for all forms of public infrastructure and facilities. Fifty-three percent of firms want Congress and the Trump administration to enact liability reforms to shield companies who are protecting workers from the coronavirus from needless lawsuits. And 41% want Congress to address unemployment benefits that serve as artificial barriers to returning people to work.

Association officials unveiled new plans to encourage more people to pursue high-paying careers in construction to ease hiring challenges and find a way to attract recently unemployed people into the construction industry. Among other steps, the association is launching a new “Construction is Essential” campaign to highlight the many benefits of construction careers.

“There is a lot that Washington officials can do to help boost demand for construction projects and get more people back to work rebuilding the economy,” said Stephen E. Sandherr, the association’s chief executive officer, noting the association was pushing Congress and the administration to enact new recovery measures. “The challenge is that the coronavirus has put many contractors in the position of looking for work and workers at the same time.”

The association and Autodesk conducted the Workforce Survey between August 4 and 26. Over 2000 firms completed the survey from a broad cross-section of the construction industry, including union and open shop firms of all sizes. The 2020 Workforce Survey is the association’s eighth annual workforce-related survey.

Click here for survey materials including national, regional and state fact sheets, survey analysis and event remarks.

Related Stories

Apartments | Aug 22, 2023

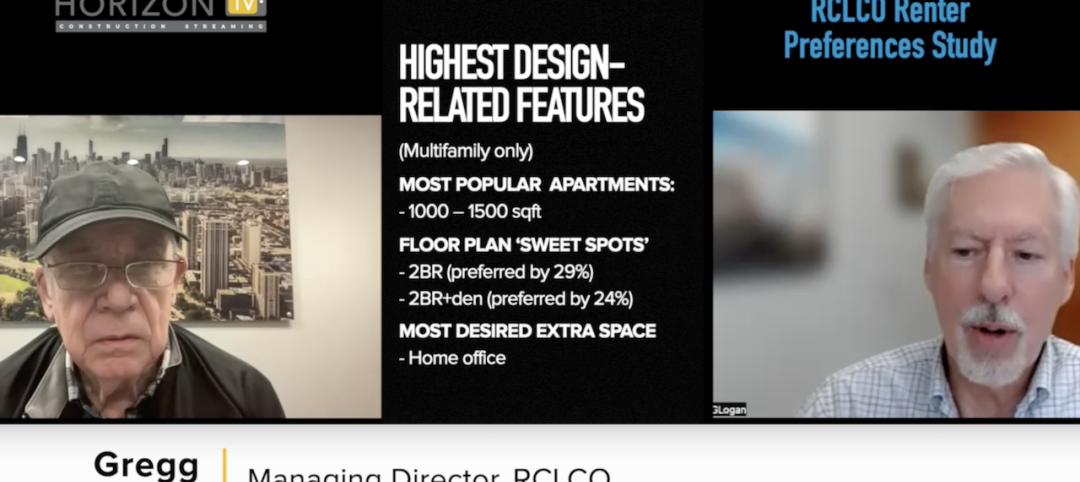

Key takeaways from RCLCO's 2023 apartment renter preferences study

Gregg Logan, Managing Director of real estate consulting firm RCLCO, reveals the highlights of RCLCO's new research study, “2023 Rental Consumer Preferences Report.” Logan speaks with BD+C's Robert Cassidy.

Market Data | Aug 18, 2023

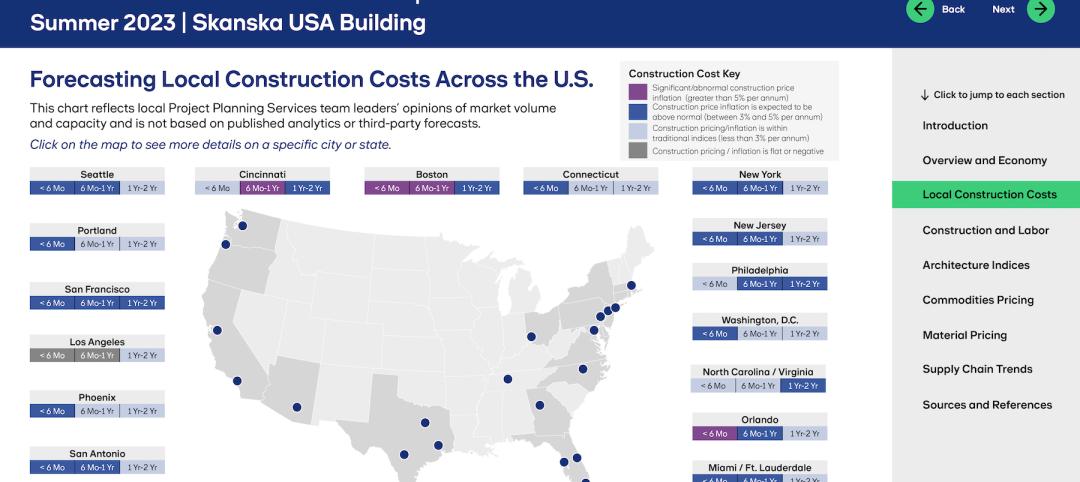

Construction soldiers on, despite rising materials and labor costs

Quarterly analyses from Skanska, Mortenson, and Gordian show nonresidential building still subject to materials and labor volatility, and regional disparities.

Apartments | Aug 14, 2023

Yardi Matrix updates near-term multifamily supply forecast

The multifamily housing supply could increase by up to nearly 7% by the end of 2023, states the latest Multifamily Supply Forecast from Yardi Matrix.

Hotel Facilities | Aug 2, 2023

Top 5 markets for hotel construction

According to the United States Construction Pipeline Trend Report by Lodging Econometrics (LE) for Q2 2023, the five markets with the largest hotel construction pipelines are Dallas with a record-high 184 projects/21,501 rooms, Atlanta with 141 projects/17,993 rooms, Phoenix with 119 projects/16,107 rooms, Nashville with 116 projects/15,346 rooms, and Los Angeles with 112 projects/17,797 rooms.

Market Data | Aug 1, 2023

Nonresidential construction spending increases slightly in June

National nonresidential construction spending increased 0.1% in June, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. Spending is up 18% over the past 12 months. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.07 trillion in June.

Hotel Facilities | Jul 27, 2023

U.S. hotel construction pipeline remains steady with 5,572 projects in the works

The hotel construction pipeline grew incrementally in Q2 2023 as developers and franchise companies push through short-term challenges while envisioning long-term prospects, according to Lodging Econometrics.

Hotel Facilities | Jul 26, 2023

Hospitality building construction costs for 2023

Data from Gordian breaks down the average cost per square foot for 15-story hotels, restaurants, fast food restaurants, and movie theaters across 10 U.S. cities: Boston, Chicago, Las Vegas, Los Angeles, Miami, New Orleans, New York, Phoenix, Seattle, and Washington, D.C.

Market Data | Jul 24, 2023

Leading economists call for 2% increase in building construction spending in 2024

Following a 19.7% surge in spending for commercial, institutional, and industrial buildings in 2023, leading construction industry economists expect spending growth to come back to earth in 2024, according to the July 2023 AIA Consensus Construction Forecast Panel.

Contractors | Jul 13, 2023

Construction input prices remain unchanged in June, inflation slowing

Construction input prices remained unchanged in June compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices were also unchanged for the month.

Contractors | Jul 11, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of June 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator remained unchanged at 8.9 months in June 2023, according to an ABC member survey conducted June 20 to July 5. The reading is unchanged from June 2022.