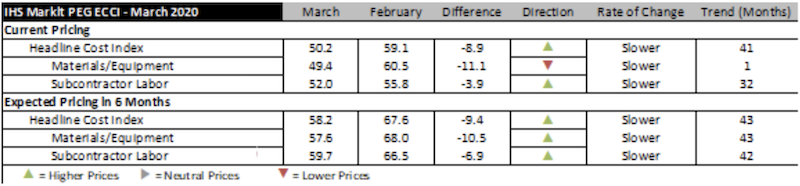

Construction costs increased once again in March, according to IHS Markit (NYSE: INFO) and the Procurement Executives Group (PEG). The current headline IHS Markit PEG Engineering and Construction Cost Index registered 50.2, a figure barely above the neutral mark. The last time the headline index registered an almost flat pricing was in November 2016. After 40 months, the materials and equipment index came in at 49.4, indicating falling prices. The sub-contractor labor index showed continued price increases, with an index reading of 52.0.

Survey respondents reported falling prices for five out of the 12 components within the materials and equipment sub-index. These included ocean freight (Asia to U.S. and Europe to U.S.), fabricated structural steel, carbon steel pipe, copper-based wire and cable. Prices for five categories rose while prices for two categories (alloy steel pipe and exchangers) remained the same. Index figures for all categories dropped relative to February, indicating that a greater proportion of the respondents are observing lower prices. The sharpest drops were reported for ocean freight.

“Ocean freight has taken a notable hit with the onset of coronavirus,” said Deni Koenhemsi, senior economist with IHS Markit. “As China tried to contain COVID-19, industrial production contracted substantially, and the transportation of goods nearly came to a halt. In the first two months of 2020, U.S. imports from Asia dropped 6.2 percent year-over-year, and imports from China were down 15.5 percent. Although the number of blank sailings is beginning to taper off-meaning we will see higher imports from China to United States-the rapid spread of the virus in Europe and North America could cause the downward trend to continue.”

The sub-index for current subcontractor labor costs came in at 52.0 for March. For the United States, labor cost remained flat in the Northeast, Midwest and West, but increased in the South. For Canada, the labor cost index was flat in western Canada but rose for eastern Canada.

The six-month headline expectations for future construction costs index reflected increasing prices for the 43rd consecutive month, registering 58.2, a sharp decline from February’s reading of 67.6. The six-month materials and equipment expectations index came in at 57.6 this month, down from 68.0 last month. Prices for all materials, equipment and freight are expected to rise with the exception of carbon steel pipe and exchangers, which are expected to see flat pricing. Expectations for sub-contractor labor slipped to 59.7 in March. All regions of the U.S. are expected to see higher labor costs; labor costs in Canada are expected to stay flat.

In the survey comments, respondents noted lower demand conditions due to the coronavirus.

To learn more about the IHS Markit PEG Engineering and Construction Cost Index or to obtain the latest published insight, please click here.

Related Stories

Market Data | Jun 22, 2018

Multifamily market remains healthy – Can it be sustained?

New report says strong economic fundamentals outweigh headwinds.

Market Data | Jun 21, 2018

Architecture firm billings strengthen in May

Architecture Billings Index enters eighth straight month of solid growth.

Market Data | Jun 20, 2018

7% year-over-year growth in the global construction pipeline

There are 5,952 projects/1,115,288 rooms under construction, up 8% by projects YOY.

Market Data | Jun 19, 2018

ABC’s Construction Backlog Indicator remains elevated in first quarter of 2018

The CBI shows highlights by region, industry, and company size.

Market Data | Jun 19, 2018

America’s housing market still falls short of providing affordable shelter to many

The latest report from the Joint Center for Housing Studies laments the paucity of subsidies to relieve cost burdens of ownership and renting.

Market Data | Jun 18, 2018

AI is the path to maximum profitability for retail and FMCG firms

Leading retailers including Amazon, Alibaba, Lowe’s and Tesco are developing their own AI solutions for automation, analytics and robotics use cases.

Market Data | Jun 12, 2018

Yardi Matrix report details industrial sector's strength

E-commerce and biopharmaceutical companies seeking space stoke record performances across key indicators.

Market Data | Jun 8, 2018

Dodge Momentum Index inches up in May

May’s gain was the result of a 4.7% increase by the commercial component of the Momentum Index.

Market Data | Jun 4, 2018

Nonresidential construction remains unchanged in April

Private sector spending increased 0.8% on a monthly basis and is up 5.3% from a year ago.

Market Data | May 30, 2018

Construction employment increases in 256 metro areas between April 2017 & 2018

Dallas-Plano-Irving and Midland, Texas experience largest year-over-year gains; St. Louis, Mo.-Ill. and Bloomington, Ill. have biggest annual declines in construction employment amid continuing demand.