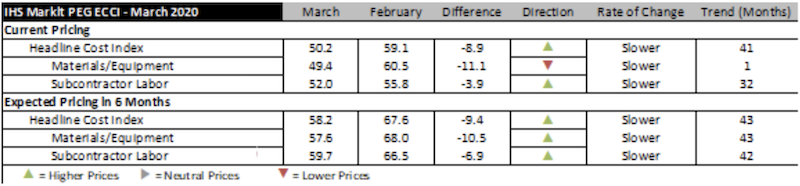

Construction costs increased once again in March, according to IHS Markit (NYSE: INFO) and the Procurement Executives Group (PEG). The current headline IHS Markit PEG Engineering and Construction Cost Index registered 50.2, a figure barely above the neutral mark. The last time the headline index registered an almost flat pricing was in November 2016. After 40 months, the materials and equipment index came in at 49.4, indicating falling prices. The sub-contractor labor index showed continued price increases, with an index reading of 52.0.

Survey respondents reported falling prices for five out of the 12 components within the materials and equipment sub-index. These included ocean freight (Asia to U.S. and Europe to U.S.), fabricated structural steel, carbon steel pipe, copper-based wire and cable. Prices for five categories rose while prices for two categories (alloy steel pipe and exchangers) remained the same. Index figures for all categories dropped relative to February, indicating that a greater proportion of the respondents are observing lower prices. The sharpest drops were reported for ocean freight.

“Ocean freight has taken a notable hit with the onset of coronavirus,” said Deni Koenhemsi, senior economist with IHS Markit. “As China tried to contain COVID-19, industrial production contracted substantially, and the transportation of goods nearly came to a halt. In the first two months of 2020, U.S. imports from Asia dropped 6.2 percent year-over-year, and imports from China were down 15.5 percent. Although the number of blank sailings is beginning to taper off-meaning we will see higher imports from China to United States-the rapid spread of the virus in Europe and North America could cause the downward trend to continue.”

The sub-index for current subcontractor labor costs came in at 52.0 for March. For the United States, labor cost remained flat in the Northeast, Midwest and West, but increased in the South. For Canada, the labor cost index was flat in western Canada but rose for eastern Canada.

The six-month headline expectations for future construction costs index reflected increasing prices for the 43rd consecutive month, registering 58.2, a sharp decline from February’s reading of 67.6. The six-month materials and equipment expectations index came in at 57.6 this month, down from 68.0 last month. Prices for all materials, equipment and freight are expected to rise with the exception of carbon steel pipe and exchangers, which are expected to see flat pricing. Expectations for sub-contractor labor slipped to 59.7 in March. All regions of the U.S. are expected to see higher labor costs; labor costs in Canada are expected to stay flat.

In the survey comments, respondents noted lower demand conditions due to the coronavirus.

To learn more about the IHS Markit PEG Engineering and Construction Cost Index or to obtain the latest published insight, please click here.

Related Stories

Market Data | Nov 30, 2016

Marcum Commercial Construction Index reports industry outlook has shifted; more change expected

Overall nonresidential construction spending in September totaled $690.5 billion, down a slight 0.7 percent from a year earlier.

Industry Research | Nov 30, 2016

Multifamily millennials: Here is what millennial renters want in 2017

It’s all about technology and convenience when it comes to the things millennial renters value most in a multifamily facility.

Market Data | Nov 29, 2016

It’s not just traditional infrastructure that requires investment

A national survey finds strong support for essential community buildings.

Industry Research | Nov 28, 2016

Building America: The Merit Shop Scorecard

ABC releases state rankings on policies affecting construction industry.

Multifamily Housing | Nov 28, 2016

Axiometrics predicts apartment deliveries will peak by mid 2017

New York is projected to lead the nation next year, thanks to construction delays in 2016

Market Data | Nov 22, 2016

Construction activity will slow next year: JLL

Risk, labor, and technology are impacting what gets built.

Market Data | Nov 17, 2016

Architecture Billings Index rebounds after two down months

Decline in new design contracts suggests volatility in design activity to persist.

Market Data | Nov 11, 2016

Brand marketing: Why the B2B world needs to embrace consumers

The relevance of brand recognition has always been debatable in the B2B universe. With notable exceptions like BASF, few manufacturers or industry groups see value in generating top-of-mind awareness for their products and services with consumers.

Industry Research | Nov 8, 2016

Austin, Texas wins ‘Top City’ in the Emerging Trends in Real Estate outlook

Austin was followed on the list by Dallas/Fort Worth, Texas and Portland, Ore.

Market Data | Nov 2, 2016

Nonresidential construction spending down in September, but August data upwardly revised

The government revised the August nonresidential construction spending estimate from $686.6 billion to $696.6 billion.