On Wednesday, the U.S. Treasury Department and the Internal Revenue Service released new regulations and guidelines for investments in the 8,700 distressed or lower-income census tracts that governors across the country have designated as Opportunity Zones (OZs).

The new regulations, which expand upon the initial round that came out last October, are meant to provide greater clarity for investors and developers about how funds raised for such investments might qualify for tax breaks.

“This round of regulations removes some of the most significant impediments keeping capital on the sidelines, especially as it relates to operating businesses,” John Lettieri, president of the Economic Innovation Group, a Washington research organization that developed and championed the Opportunity Zone concept, told the New York Times.

The new round of regs is timely, as the maximum tax benefit of the legislation requires an Opportunity Zone investment be completed by December 31.

While the federal government has projected $100 billion in Opportunity Zone investments, some developers so far have held back from jumping into this program—which was part of the tax overhaul that Congress approved in 2017—because of uncertainties about qualifications of both buildings and businesses to invest in.

The logic behind OZs is that wealth generated by capital gains could be better used for investments in neighborhoods that typically lack access to that money for redevelopment. The goal of OZs is to spur economic growth. But some skeptics had contended that the program’s regulatory structure was too lax, and that the government, through tax breaks, would end up subsidizing developments in areas that were already attractive to investors.

There are also concerns about gentrification, as the Opportunity Zone concept hasn’t always worked as intended, or at least to the direct benefit of low-income residents. Zillow Economic Research reported in March that prices for homes within Opportunity Zones rose by 25.3% last year, versus 8.4% for census tracts that were eligible but not selected as OZs, and 2.5% for tracts not eligible.

HUD’s Secretary Ben Carson told The Real Deal last month that his agency cannot mandate affordable housing in the zones. It will, however, give preference for developers who apply for certain federal grants to build affordable housing within Opportunity Zones.

Money flowing to Opportunity Zones has mostly gone toward real estate investments, particularly on both coasts. Treasury Secretary Steven Mnuchin has emphasized that the program is also geared toward other types of businesses as well.

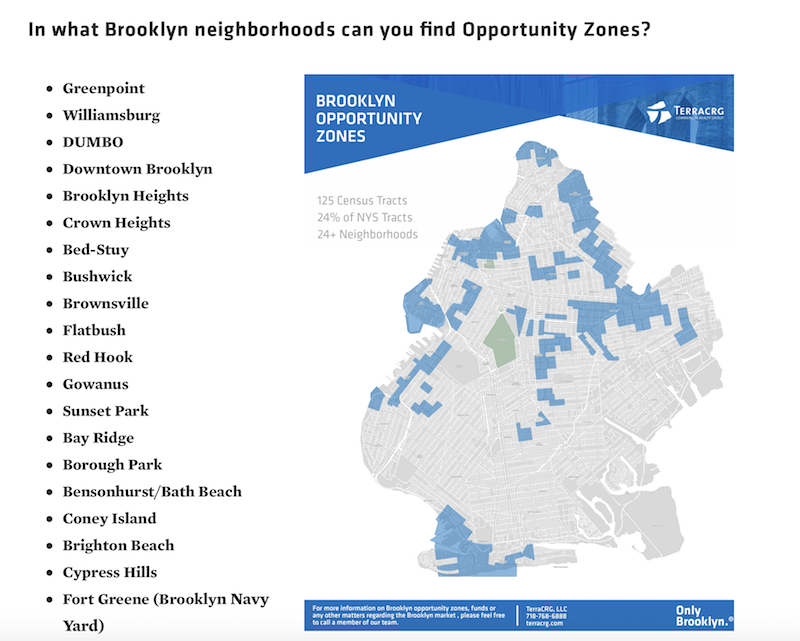

The New York City borough of Brooklyn is where New York State has designated 125 of its 514 Opportunity Zones. Nationwide, governors have designated 8,700 OZs. Image: TerraCRG

The new regulations spell out in greater detail the program’s investment and tax-break mechanism.

For one thing, new regulations create tax benefits for leased property, according to Law.com. Investors essentially can take their capital gains from any venture, real estate or otherwise, and put them into a qualified opportunity zone fund that then, likely through a fund manager, seeks eligible projects. The earlier version gave investors 180 days from the date they realized capital gains to put the money into an opportunity zone fund. If they keep their money in the fund for five years, 10% of their deferred gain is eliminated. An additional 5% of their capital gains would be untaxed if they keep their money in the fund for seven years.

The biggest tax benefit from this program accrues to investors and developers who hold their money in an Opportunity Zone for at least a decade. By doing so, they forgo paying tax on capital gains from those investments altogether.

Opportunity Funds raised by investors get a 12-month grace period to sell assets in Opportunity Zones and then reinvest those proceeds in the Zone. There was some concern previously that this reinvestment had to be made immediately.

The Times reports that investors will be allowed to share their stakes in funds that invest in the zones, and to sell, say, a start-up in an Opportunity Zone as long as the money is reinvested in another qualifying business or asset. Real estate investors will be allowed to lease and refinance their properties.

However, the proposal also allows Treasury officials to revoke a tax break for any Opportunity Zone project “if a significant purpose of a transaction is to achieve a tax result that is inconsistent with the purposes” of the program.

Investors have been concerned about earlier guidance that stated a business that wanted to qualify for the Opportunity Zone program had to derive at least half of its gross income from the Zone itself. Joshua Pollard, a contributing writer for Forbes, points out that the new guidance assuages those concerns by creating four distinct tests for businesses to qualify:

•Total hours worked by employees or independent contractors in a Zone must equal at least 50% of the company’s total hours worked;

•Half of total dollars paid to those employees or contractors must be for services performed in the Zone. The Times reports that provisions in the new regulations allow investors to qualify for tax breaks even if the businesses they fund export goods or services, or if the domestic market for those goods is outside of the zone.

•A business’s management and operational staff, and the tangible property of the business, that are in the Opportunity Zone must be essential to at least half of the business’s gross income; and

•A fourth, intentionally ambiguous, category, “Facts and circumstances,” leaves a lot of wriggle room for businesses to make their case to the IRS, says Pollard.

Pollard notes that outside of the 169-page guidance document, the White House Opportunity and Revitalization Council, made up of nearly 20 federal agencies, has added so-called “preference points,” or tie-breaker considerations, for projects and applicants in Opportunity Zones this year, with the explicit goal of eliminating federal bureaucracy. Ultimately this could give a leg up to as many as 150 programs.

Related Stories

| Oct 15, 2013

15 great ideas from the Under 40 Leadership Summit – Vote for your favorite!

Sixty-five up-and-coming AEC stars presented their big ideas for solving pressing social, economic, technical, and cultural problems related to the built environment. Which one is your favorite?

| Oct 8, 2013

Government shutdown closes E-Verify, could hamper construction hiring

E-Verify, the online federal program used to check the immigration status of prospective hires, has been closed due to the federal government shutdown.

| Oct 3, 2013

Florida contractors worry that regulations will hamper their ability to hire

Regulations such as the E-Verify rule and the Affordable Care Act could hinder contractors from hiring additional workers, according to some Florida contractors.

| Oct 3, 2013

Fall protection violations top OSHA citations list

Violations of fall-protection standards in fiscal 2013 are again the most frequent source of citations from the Occupational Safety and Health Administration, according to its top 10 list.

| Sep 26, 2013

OSHA encourages comments on respirable crystalline silica rules

The Occupational Safety and Health Administration’s proposed rulemaking for respirable crystalline silica has been published in the Federal Register.

| Sep 18, 2013

Proposed Boston casino development approval will depend partly on sustainability

The movement toward green building has been slow to catch on in the casino industry, but that could change with Suffolk Downs, which plans to build a $1 billion casino in Boston.

| Sep 18, 2013

Regulations could ease firefighters’ fear of roof solar panels

The local fire chief says solar panels are partly to blame after a 300,000 sf refrigerated warehouse in Delanco, N.J., burned down.

| Sep 11, 2013

Disability, vet hiring standards for contractors are goals, not quotas

Contractors that fall short of new federal hiring rules concerning veterans and disabled persons will not necessarily incur penalties, says Patricia Shiu, director of the Office of Federal Contract Compliance Programs.

| Sep 5, 2013

Construction industry groups create coalition to respond to new OSHA silica rule

A group of 11 construction trade associations has created the Construction Industry Safety Coalition in response to the Occupational Safety and Health Administration’s (OSHA) proposed rule on silica for the construction industry.

| Sep 5, 2013

Red tape delays California county jail construction projects

California authorized $1.2 billion for jail construction in 2007, but not a single county in the state has completed a jail project since then.