Analysts at Lodging Econometrics (LE) report that at the close of the first quarter of 2020*, the top five U.S. markets with the largest total hotel construction pipelines are: Los Angeles with 166 projects/27,752 rooms; Dallas with 164 projects/19,999 rooms; New York City with 152 projects/26,111 rooms; Atlanta with 143 projects/19,423 rooms; and Houston with 132 projects/13,316 rooms.

Nationally, under construction project counts hit a new all-time high with 1,819 projects with 243,100 rooms. Markets with the greatest number of projects already in the ground are led by New York City with 108 projects/18,434 rooms. Atlanta follows with 48 projects/6,002 rooms, and then Dallas with 46 projects/5,603 rooms, Los Angeles with 43 projects/6,851 rooms, and Orlando with 39 projects/9,394 rooms. Collectively, these five markets account for 16% of the total number of projects currently under construction in the U.S.

In the first quarter, Dallas had the highest number of new projects announced into the pipeline with 13 projects/1,461 rooms. Washington DC follows with 8 projects/1,145 rooms, then Phoenix with 8 projects/904 rooms, Los Angeles with 7 projects/1,103 rooms, and Atlanta with 7 projects/774 rooms.

As has been widely reported, the majority of hotels across America are experiencing an extreme decrease in occupancy and some have even closed temporarily. Many companies are using this time to complete updates, plan or start renovations or reposition their assets. LE recorded renovation and conversion totals of 1,385 active projects/232,288 rooms in the first quarter of 2020. The markets with the largest count of renovation and conversion projects combined are Chicago with 32 projects/5,565 rooms, Washington DC with 26 projects/5,491 rooms, Los Angeles with 26 projects/4,271 rooms, New York City with 21 projects/8,151 rooms and San Diego with 21 projects/4,456 rooms.

FOOTNOTE:

*COVID-19 (coronavirus) did not have a full impact on first quarter 2020 U.S. results reported by LE. Only the last 30 days of the quarter were affected. LE’s market intelligence department has and will continue to gather the necessary global intelligence on the supply side of the lodging industry and make that information available to our subscribers. It is still early to predict the full impact of the outbreak on the lodging industry. We will have more information to report in the coming months.

Related Stories

Market Data | Apr 20, 2021

Demand for design services continues to rapidly escalate

AIA’s ABI score for March rose to 55.6 compared to 53.3 in February.

Market Data | Apr 16, 2021

Construction employment in March trails March 2020 mark in 35 states

Nonresidential projects lag despite hot homebuilding market.

Market Data | Apr 13, 2021

ABC’s Construction Backlog slips in March; Contractor optimism continues to improve

The Construction Backlog Indicator fell to 7.8 months in March.

Market Data | Apr 9, 2021

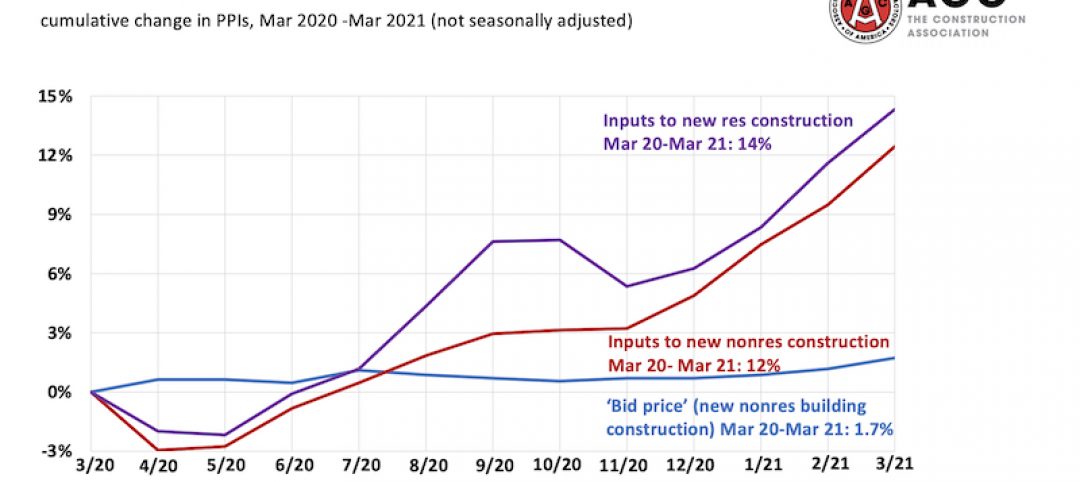

Record jump in materials prices and supply chain distributions threaten construction firms' ability to complete vital nonresidential projects

A government index that measures the selling price for goods used construction jumped 3.5% from February to March.

Contractors | Apr 9, 2021

Construction bidding activity ticks up in February

The Blue Book Network's Velocity Index measures month-to-month changes in bidding activity among construction firms across five building sectors and in all 50 states.

Industry Research | Apr 9, 2021

BD+C exclusive research: What building owners want from AEC firms

BD+C’s first-ever owners’ survey finds them focused on improving buildings’ performance for higher investment returns.

Market Data | Apr 7, 2021

Construction employment drops in 236 metro areas between February 2020 and February 2021

Houston-The Woodlands-Sugar Land and Odessa, Texas have worst 12-month employment losses.

Market Data | Apr 2, 2021

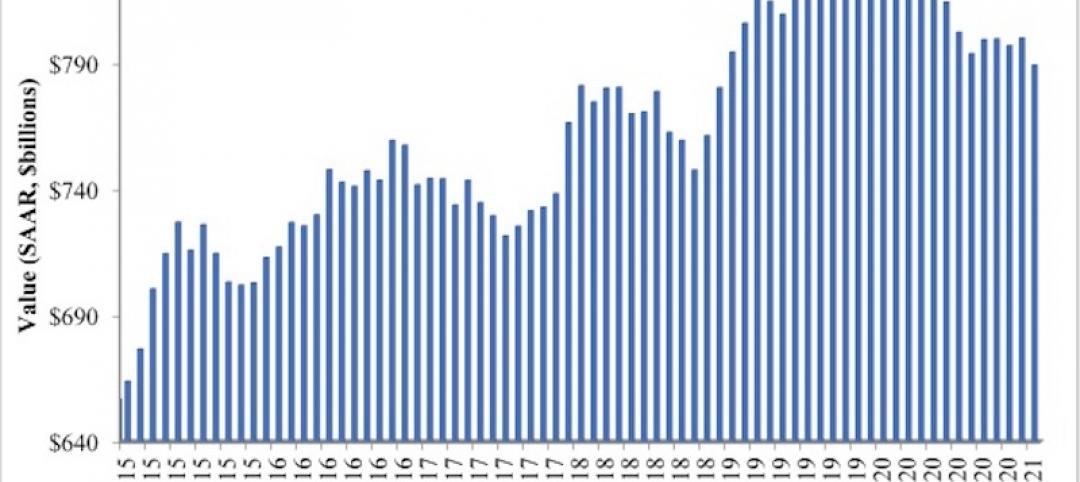

Nonresidential construction spending down 1.3% in February, says ABC

On a monthly basis, spending was down in 13 of 16 nonresidential subcategories.

Market Data | Apr 1, 2021

Construction spending slips in February

Shrinking demand, soaring costs, and supply delays threaten project completion dates and finances.

Market Data | Mar 26, 2021

Construction employment in February trails pre-pandemic level in 44 states

Soaring costs, supply-chain problems jeopardize future jobs.