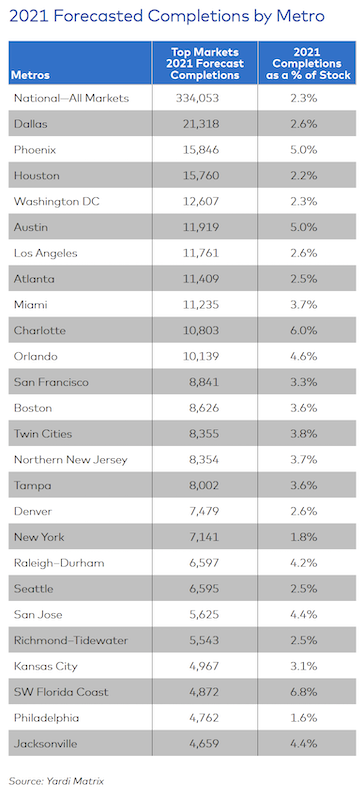

Having weathered the coronavirus pandemic somewhat better than the single-family home construction sector, new supply of multifamily housing delivered in 2021 is expected to increase by around 17% to 334,000 units, according to Yardi Matrix’s latest U.S. Outlook.

“Some 174,000 units were absorbed nationally through May, which puts 2021 on track to be among the hottest years since the 2008 recession,” states the report.

As of mid-year, some 863,500 multifamily units were under construction, representing 6% of the existing U.S. stock. That’s good and bad news, suggests Yardi Matrix, because such a large number of projects could impede the overall rent recovery in so-called “gateway” markets like Miami, whose forecasted deliveries are projected to equal 3.7% of its existing stock; Boston (3.6% of existing stock), San Francisco (3.3%), Los Angeles (2.6%), Washington D.C. (2.3%), New York (1.8%) and Chicago (1.3%).

“These new projects might have a difficult time leasing up, as there is already much supply in these metros with limited new demand, especially in the Lifestyle segment,” states the report.

The leaders in multifamily completions over the past 12 months include Austin (4.4% of total stock), Charlotte (4.3%), Minneapolis-St. Paul (3.7%) and Raleigh (3.6%). Yardi Matrix points out that among these four metros, Charlotte has been the only one able to sustain strong rent growth and deliveries simultaneously. Still, rents in all four metros have picked up in recent months, driven by a surge in migration and demand for apartments.

Yardi Matrix foresees Dallas leading the country in multifamily completions this year. Image: Yardi Matrix

SMALLER MARKETS, BIGGER DEMAND

Yardi Matrix looked at 136 markets, and found robust growth in tertiary metros like Northwest Arkansas (home to Walmart’s headquarters city of Bentonville) that led the list with 8.8% of its stock expected to be delivered this year from new construction. Next were Wilmington, N.C. (with 7% of its stock expected to be delivered), and the Southwest Florida Coast (6.8%). These metros had limited existing multifamily housing stock to begin with.

Measured by sheer units, Dallas is forecast to have the highest number of completions in 2021 (21,318 units), followed by Phoenix, Houston, Washington DC, Austin, L.A., Atlanta, and Miami. Yardi Matrix believes that while Dallas, Phoenix, and Houston should have little trouble absorbing new deliveries, “Washington DC might struggle,” because demand is lagging in part due to remote work requirements or preferences, and out-migration.

Material price hikes are the “wild card” in prognostications about apartment development, says Yardi Matrix. The extreme volatility of lumber prices over the past several months, coupled with increases in the cost of other building materials, could slow new starts and force developers “to choose between raising rents and reducing profit margins.”

RENTS RISING AT UNSUSTAINABLE RATES

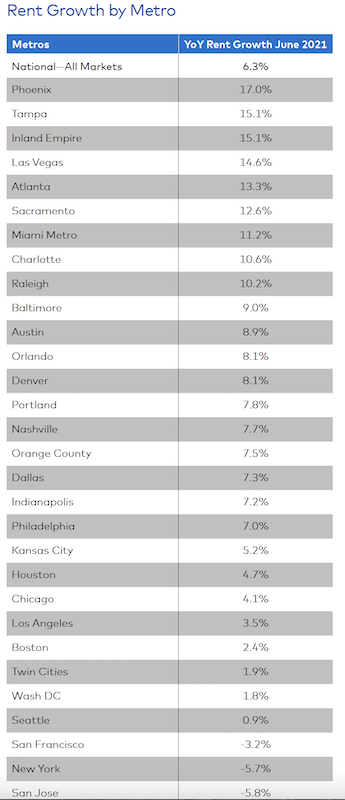

Through the first six months of 2021, national asking rents rose 5.8%. Yardi Matrix estimates that year-over-year asking rent growth, as of June, stood at 6.3%, “well above the [country’s] pre-pandemic performance.” Rent inflation is even more pronounced in tech hubs and tertiary metros, and asking rent growth in the Southwest and Southeast has been at levels “not seen in decades.”

While this escalation for multifamily units probably isn’t sustainable, Yardi Matrix expects conditions for above-average rent growth to persist in many metros “for months.” The report points out that rents are driven by “buoyant” demand. In the 12 months through May, 378,000 multifamily units were absorbed nationwide. The top markets for absorption as a percentage of total inventories were Miami (8,500 units, or 2.7% of stock), Charlotte (4,500, 2.4%) and Orlando (4,900, 2.1%).

Through June of this year, rent growth in Phoenix was nearly three times the national average. And despite its year-to-year rent decline, New York bounced back in the first half of 2021. Image: Yardi Matrix

By units, Chicago topped the list with almost 7,800 multifamily units absorbed, or 2.2 % of the Windy City’s stock. And for all the talk about New Yorkers evacuating in droves during the pandemic, rents actually rose by 6% during the first half of this year, and more companies are now requiring employees to return to office work. Rent recoveries through the first half of 2021 were also in “full swing” in Chicago (up 6.5%), Miami (6.4%), Boston (5%), Los Angeles (4%) and D.C. (3.3%).

Yardi Matrix’s report offers an economic outlook that foresees a flat labor participation market, and questions about rising inflation. Economic volatility “is likely to continue” globally until markets get a handle on controlling their virus outbreaks. “However, that does not mean there won’t be strong economic growth in certain sectors and geographies in the short term,” the report states.

Related Stories

Multifamily Housing | Sep 15, 2022

Heat Pumps in Multifamily Projects

RMI's Lacey Tan gives the basics of heat pumps and how they can reduce energy costs and carbon emissions in apartment projects.

Multifamily Housing | Sep 14, 2022

27 new kitchen and bath products multifamily developers and AEC teams are using for the first time

Multifamily developers and AEC project teams are adopting new kitchen + bath products and systems for the first time, according to the MULTIFAMILY Design+Construction Kitchen+Bath Survey 2022.

Multifamily Housing | Sep 13, 2022

Take the Multifamily Kitchen + Bath survey – Maybe win one of 10 $50 gift cards

Preliminary results of 2022 Multifamily Design+Construction exclusive Kitchen + Bath survey.

Senior Living Design | Sep 8, 2022

What’s new with AQ: The top trends in active adult living

Today's 55-or-better buyers are ready to design their lives and their homes as they see fit. With so much growth on tap, builders and developers must stay apprised of trends related to home, environment, and culture of 55+ communities.

Mass Timber | Aug 30, 2022

Mass timber construction in 2022: From fringe to mainstream

Two Timberlab executives discuss the market for mass timber construction and their company's marketing and manufacturing strategies. Sam Dicke, Business Development Manager, and Erica Spiritos, Director of Preconstruction, Timberlab, speak with BD+C's John Caulfield.

Giants 400 | Aug 29, 2022

Top 50 Senior Living Facility Contractors + CM Firms for 2022

Whiting-Turner, Ryan Companies US, W.E. O'Neil Construction, and KBE Building Corp. top the ranking of the nation's largest senior living facility contractors and construction management (CM) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Giants 400 | Aug 29, 2022

Top 80 Senior Living Facility Architecture + AE Firms for 2022

Perkins Eastman, Hord Coplan Macht, Ryan A+E, and Stantec top the ranking of the nation's largest senior living facility architecture and architecture/engineering (AE) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Giants 400 | Aug 29, 2022

Top 30 Senior Living Facility Engineering + EA Firms for 2022

WSP, Olsson, Kimley-Horn, and KPFF Consulting Engineers top the ranking of the nation's largest senior living facility engineering and engineering/architecture (EA) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Giants 400 | Aug 29, 2022

Top 40 Student Housing Facility Contractors + CM Firms for 2022

J.H. Findorff & Son, PCL Construction Enterprises, Juneau Construction, and Sundt Construction top the ranking of the nation's largest student housing facility contractors and construction management (CM) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Giants 400 | Aug 29, 2022

Top 35 Student Housing Facility Engineering + EA Firms for 2022

Kimley-Horn, Wiss, Janney, Elstner Associates, KPFF Consulting Engineers, and Jacobs top the ranking of the nation's largest student housing facility engineering and engineering/architecture (EA) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.