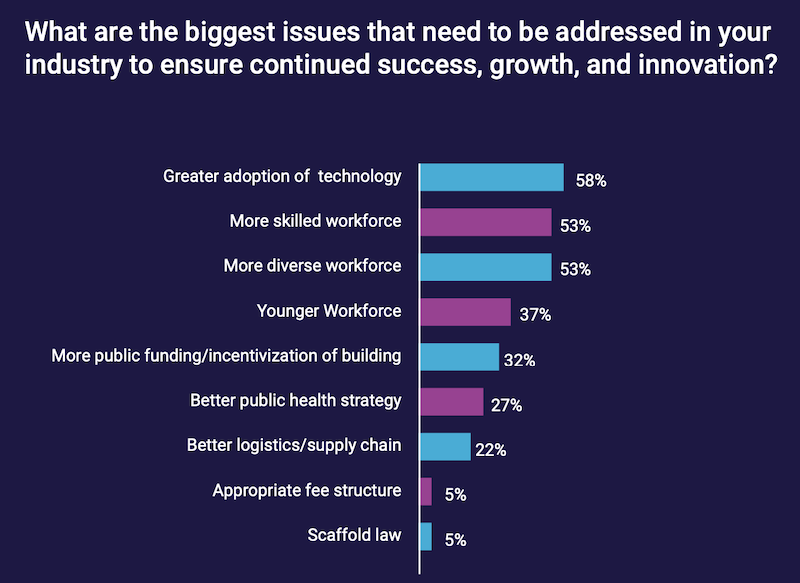

Modernization that leans heavier on technology to attract a younger, diverse, and skilled workforce is likely to determine the future success and growth of New York’s construction industry.

That is one of the key takeaways from a “State of the Construction Industry” survey of 20 New York metro-area AEC firms that the accounting consultancy Anchin, Block & Anchin conducted last November, and whose results it released earlier this month.

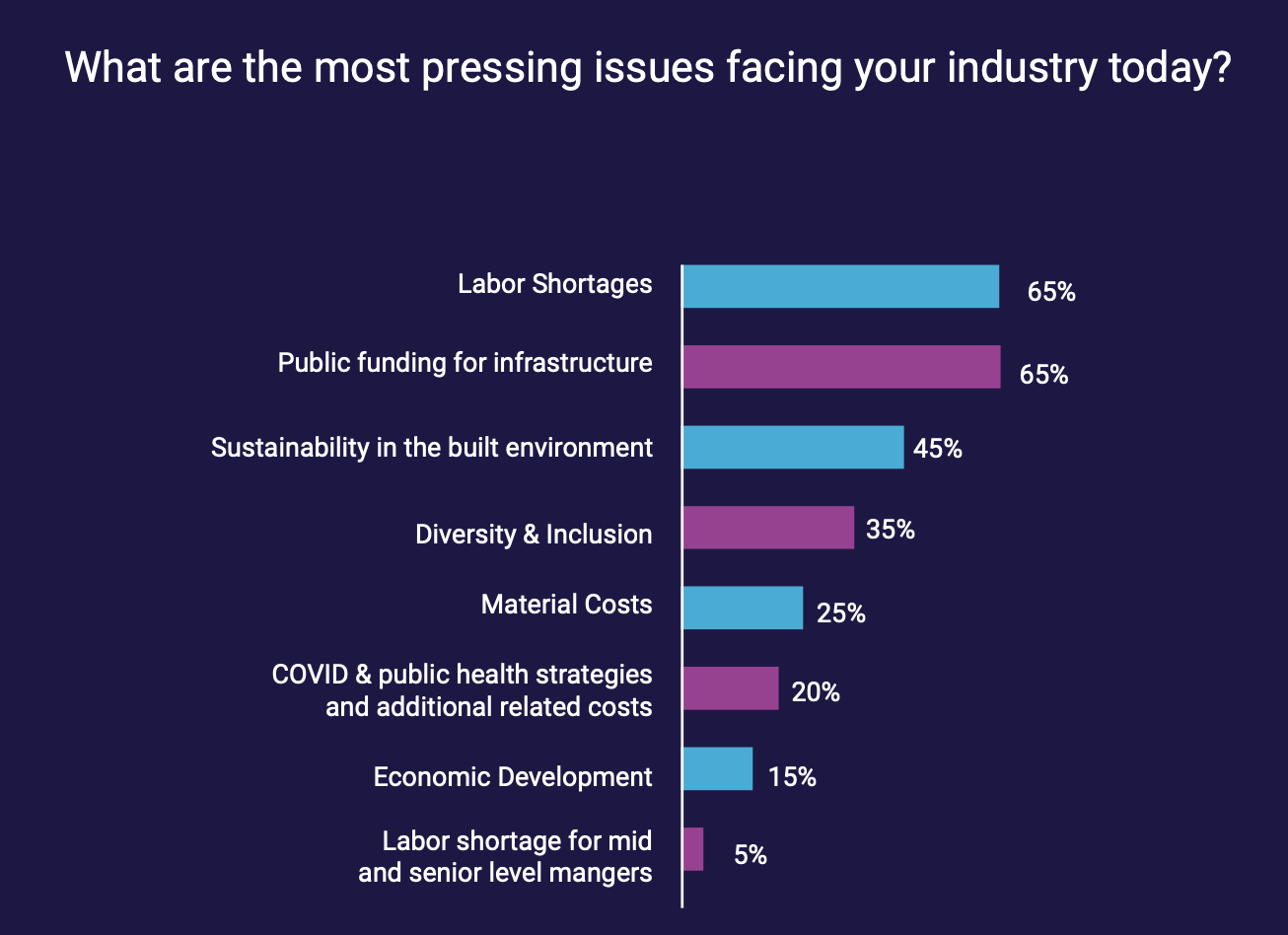

The report found a New York market that is at once resilient and facing “unprecedented challenges.” Its “most pressing” issues, as stated by nearly two-thirds of the firms polled, are labor shortages and public funding for infrastructure projects. Retaining talent is critical to these companies, and has led AEC firms toward greater flexibility about allowing remote or hybrid work, and increasing worker salaries. Thirty percent of the firms polled are focusing on management training and career development.

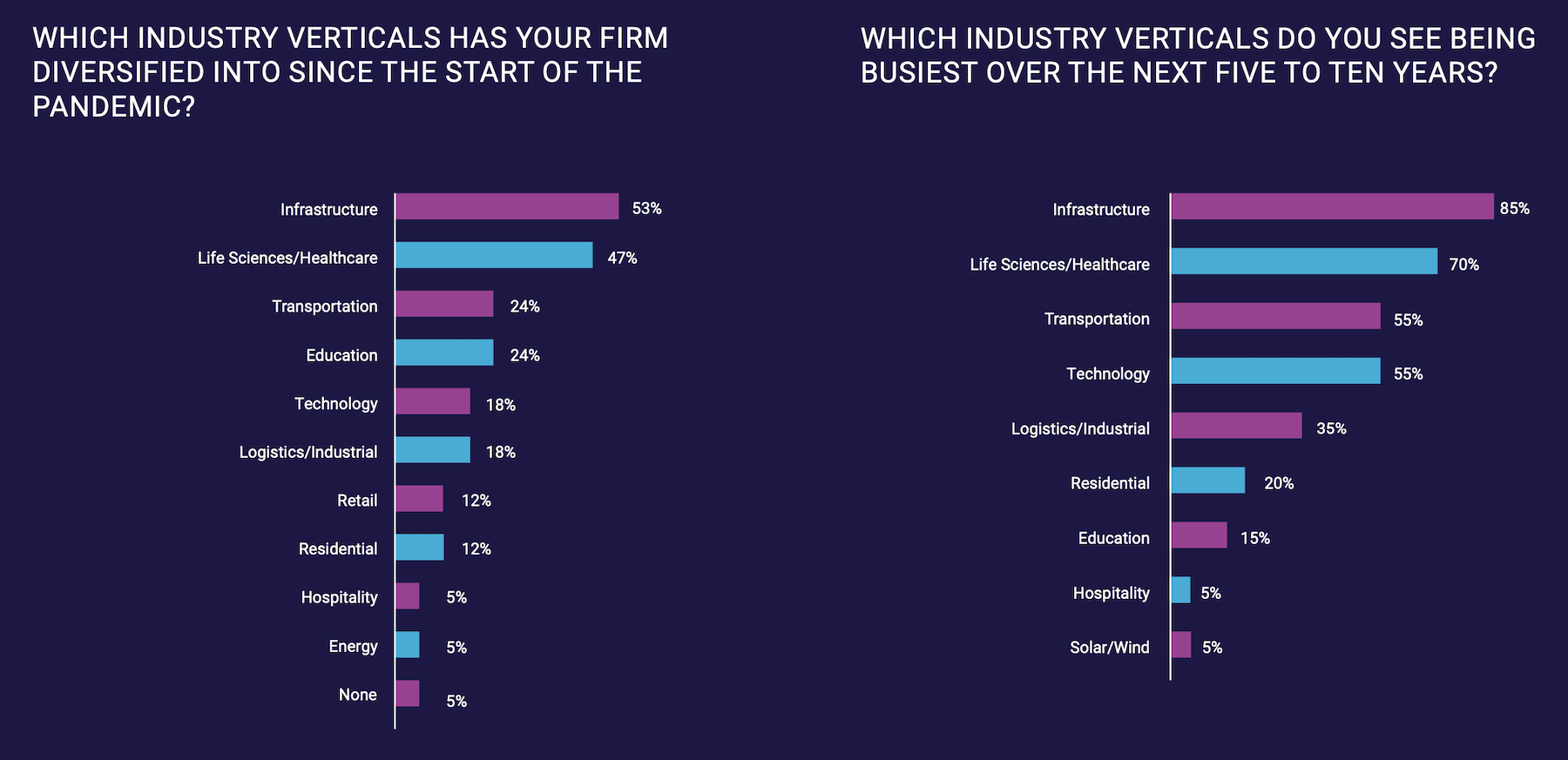

LIFE SCIENCES AND INDUSTRIAL SEEN AS GROWTH SECTORS

Since the coronavirus pandemic was declared in March 2020, more than half of the firms surveyed have diversified into the infrastructure sector, no doubt in anticipation of the $1.2 trillion federal infrastructure bill that President Biden signed into law last November. Eighty-five percent of the AEC firms polled expect infrastructure to be their market’s “busiest” sector over the next five to 10 years, followed by the life sciences/healthcare sector (into which nearly half of the firms polled diversified over the past 18 months}.

The survey’s authors also point to the industrial sector’s “growing momentum” as an in-demand asset driven by e-commerce.

However, AEC firms lamented the pressures being exerted on their companies’ cashflows from, most prominently, slower client payments, labor and materials cost inflation, insurance costs, and project delays.

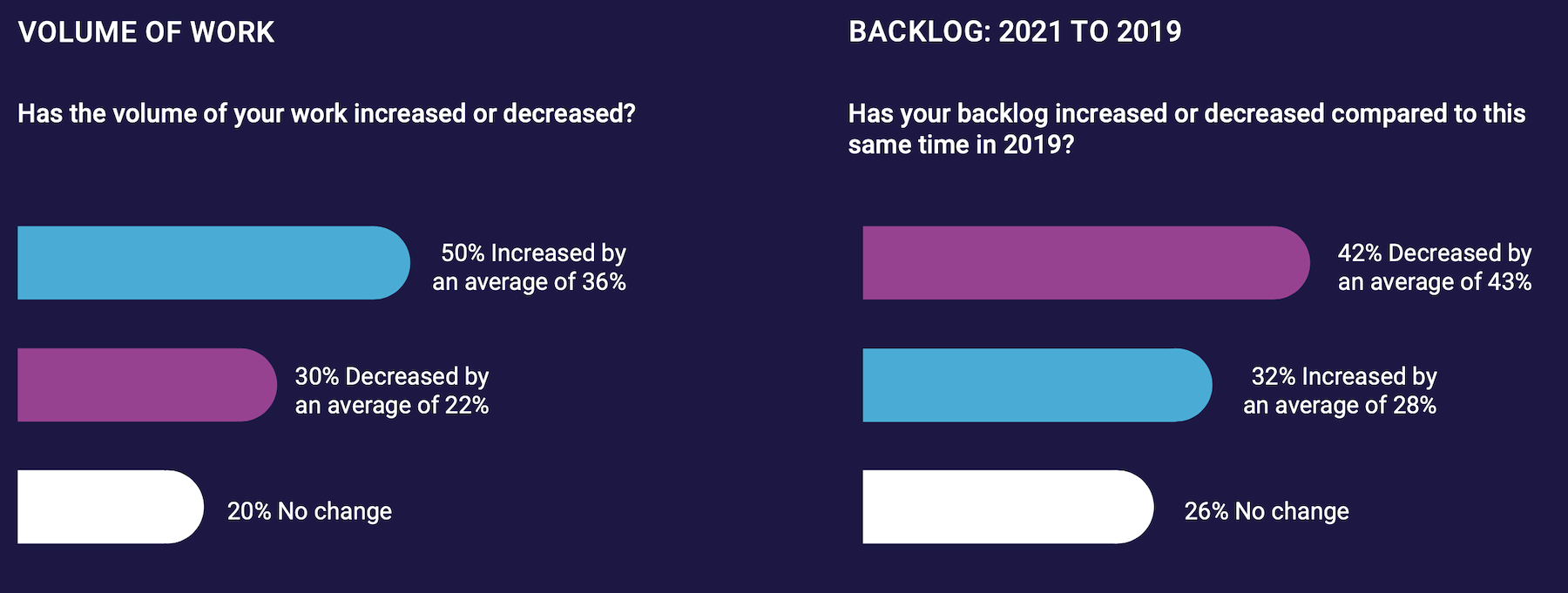

Half of the survey’s respondents said that their volume of work has increased during the pandemic, by an average of 36 percent. But 30 percent reported decreases in their companies’ work volumes, by an average of 22 percent. And 42 percent of those polled said their backlogs were down from 2019, by an average of 43 percent.

RESILIENCE AND SUSTAINABILITY ARE CENTRAL

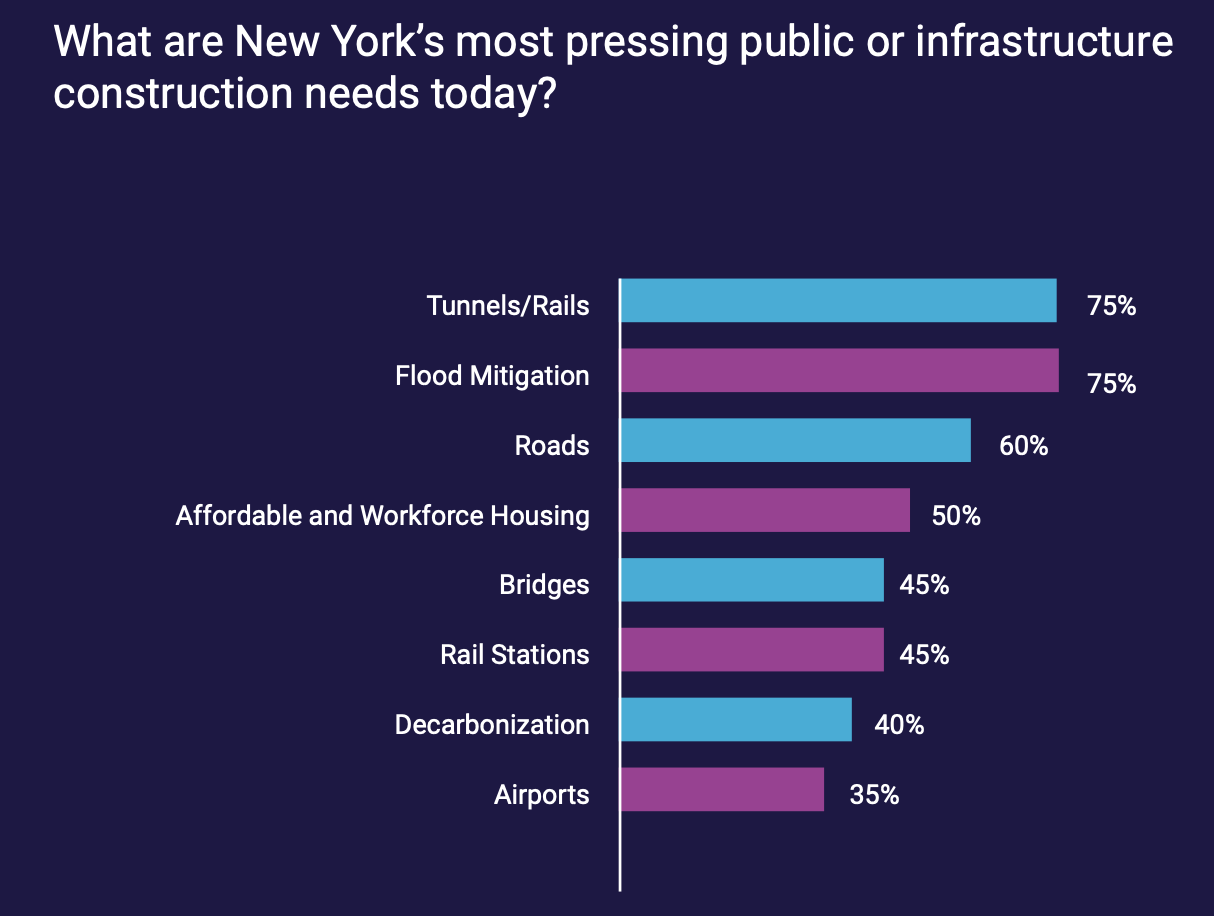

The usual suspects—tunnels, roads, bridges, rail stations—were cited by the survey’s respondents as being among the structures desperate for repair or replacement. A surprising 40 percent of the firms polled also identified “decarbonization” as a need, most probably because of New York’s Local Law 97, which passed in 2019, and creates carbon emissions limits for most commercial buildings over 25,000 sf, as well as alternative paths for the law’s two compliance periods: 2024-2029, and 2030-2034. Building owners must submit emission intensity reports, stamped by a registered design professional, every year starting in 2025 or face substantial fines.

“The overwhelming trend relates to resilience, particularly in the face of a growing urban population; and sustainability/climate change needs, which are being felt acutely,” the report states.

Related Stories

Market Data | Jul 18, 2019

Construction contractors remain confident as summer begins

Contractors were slightly less upbeat regarding profit margins and staffing levels compared to April.

Market Data | Jul 17, 2019

Design services demand stalled in June

Project inquiry gains hit a 10-year low.

Market Data | Jul 16, 2019

ABC’s Construction Backlog Indicator increases modestly in May

The Construction Backlog Indicator expanded to 8.9 months in May 2019.

K-12 Schools | Jul 15, 2019

Summer assignments: 2019 K-12 school construction costs

Using RSMeans data from Gordian, here are the most recent costs per square foot for K-12 school buildings in 10 cities across the U.S.

Market Data | Jul 12, 2019

Construction input prices plummet in June

This is the first time in nearly three years that input prices have fallen on a year-over-year basis.

Market Data | Jul 1, 2019

Nonresidential construction spending slips modestly in May

Among the 16 nonresidential construction spending categories tracked by the Census Bureau, five experienced increases in monthly spending.

Market Data | Jul 1, 2019

Almost 60% of the U.S. construction project pipeline value is concentrated in 10 major states

With a total of 1,302 projects worth $524.6 billion, California has both the largest number and value of projects in the U.S. construction project pipeline.

Market Data | Jun 21, 2019

Architecture billings remain flat

AIA’s Architecture Billings Index (ABI) score for May showed a small increase in design services at 50.2.

Market Data | Jun 19, 2019

Number of U.S. architects continues to rise

New data from NCARB reveals that the number of architects continues to increase.

Market Data | Jun 12, 2019

Construction input prices see slight increase in May

Among the 11 subcategories, six saw prices fall last month, with the largest decreases in natural gas.