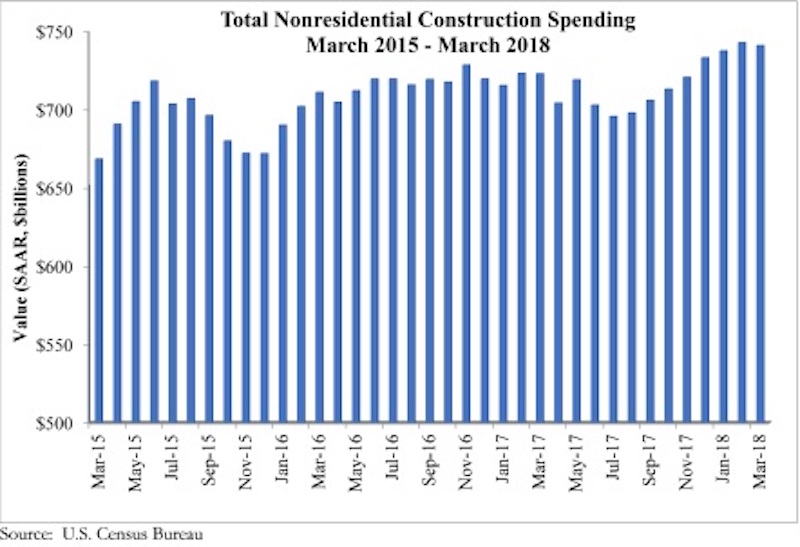

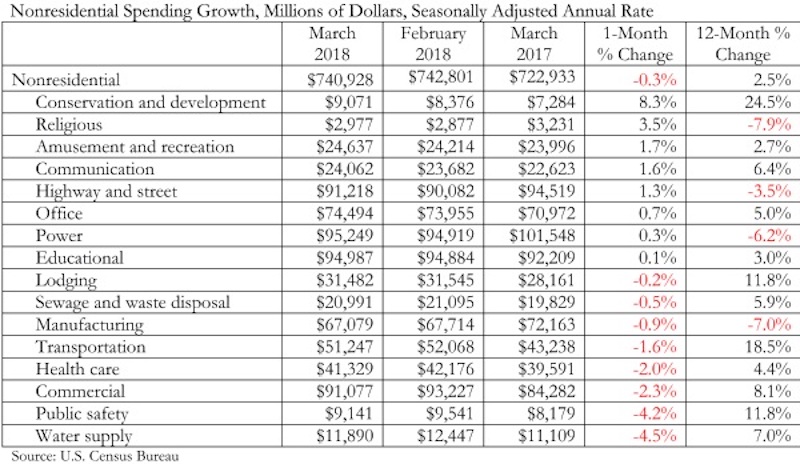

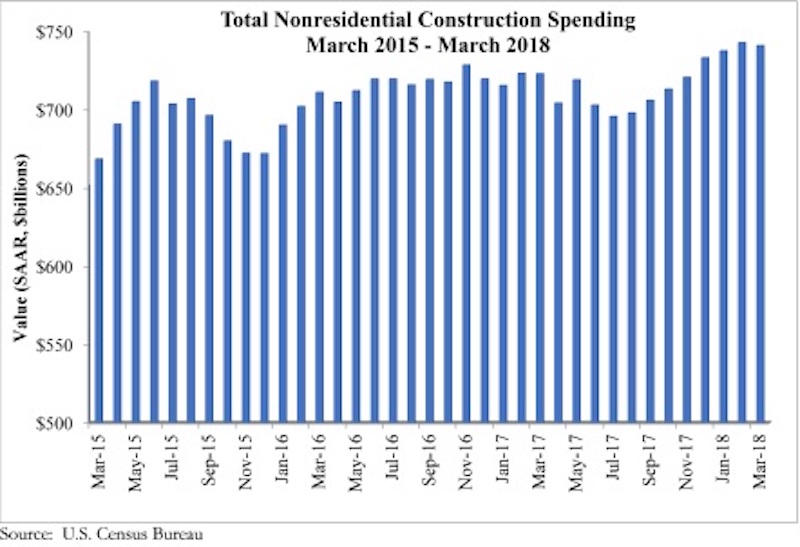

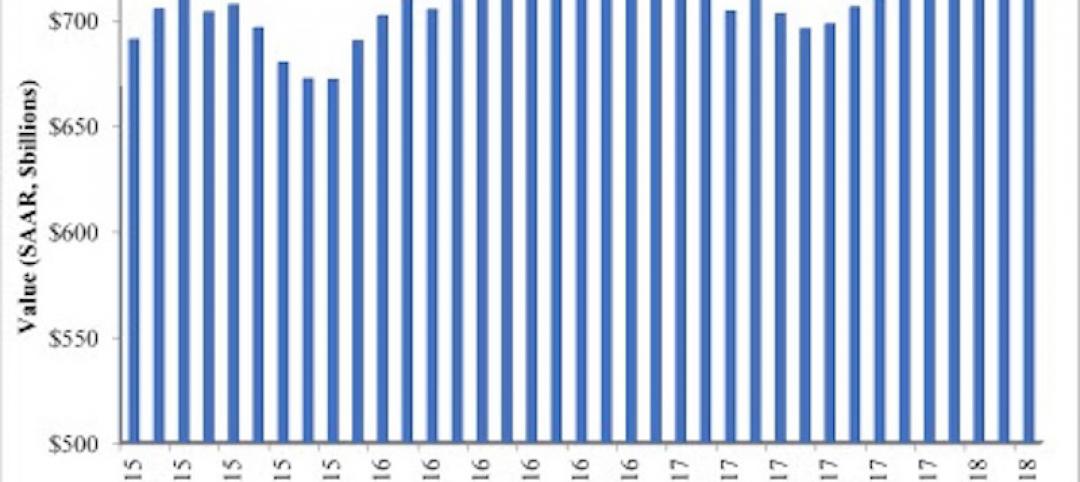

Nonresidential construction spending declined 0.3% in March, according to an Associated Builders and Contractors (ABC) analysis of U.S. Census Bureau data recently released. Nonresidential spending, which totaled $740.9 billion on a seasonally adjusted, annualized basis, has expanded 2.5% on a year-over-year basis. February’s spending estimate was revised roughly $10 billion higher, from $732.8 billion to $742.8 billion, rendering the March decline less meaningful.

Private sector nonresidential construction spending fell 0.4% on a monthly basis, but rose 2.2% from a year ago. Public sector nonresidential spending remained unchanged in March, but it is up 2.9% year-over-year.

“The nonresidential construction spending data emerging from the Census Bureau continue to be a bit at odds with other data characterizing growth in the level of activity,” said ABC’s Chief Economist Anirban Basu. “For instance, first quarter GDP data indicated brisk expansion in nonresidential investment. Data from ABC’s Construction Backlog Indicator, the Architecture Billings Index and other leading industry indicators have also been suggesting ongoing growth. Despite that, private nonresidential construction spending is up by roughly the inflation rate, indicating that the volume of services delivered over the past year has not expanded in real terms.

“That said, most economists who follow the industry presumed that March data would be somewhat soft,” said Basu. “The Northeast and Midwest were impacted by unusually persistent storm activity in March. The same phenomenon impacted March’s employment estimates, which indicated that construction actually lost 15,000 jobs that month. Other weather-sensitive industries, including retail trade, also experienced slow to negative job growth in March.

“The upshot is that CEOs and other construction leaders should remain upbeat regarding near-term prospects despite today’s construction spending report,” said Basu. “Leading indicators, including a host of confidence measures, collectively suggest that business investment will be on the rise during the months ahead. Improved state and local government finances should also support additional nonresidential construction activity.

“At the same time, construction industry leaders must remain wary of a sea of emerging risks to the ongoing economic and construction industry expansions,” said Basu. “Interest rates are on the rise. Materials prices, including those associated with softwood lumber, steel and aluminum, are expanding briskly. Wage pressures continue to build. There are also issues related to America’s expanding national debt, increasingly volatile financial markets, geopolitical uncertainty that has helped to propel fuel prices higher, and lack of transparency regarding America’s infrastructure investment intentions. The challenge for construction CEOs and others, therefore, is to prepare for growing activity in the near-term, but for something potentially rather different two to three years from now.”

Related Stories

Market Data | Jun 26, 2018

Yardi Matrix examines potential regional multifamily supply overload

Outsize development activity in some major metros could increase vacancy rates and stagnate rent growth.

Market Data | Jun 22, 2018

Multifamily market remains healthy – Can it be sustained?

New report says strong economic fundamentals outweigh headwinds.

Market Data | Jun 21, 2018

Architecture firm billings strengthen in May

Architecture Billings Index enters eighth straight month of solid growth.

Market Data | Jun 20, 2018

7% year-over-year growth in the global construction pipeline

There are 5,952 projects/1,115,288 rooms under construction, up 8% by projects YOY.

Market Data | Jun 19, 2018

ABC’s Construction Backlog Indicator remains elevated in first quarter of 2018

The CBI shows highlights by region, industry, and company size.

Market Data | Jun 19, 2018

America’s housing market still falls short of providing affordable shelter to many

The latest report from the Joint Center for Housing Studies laments the paucity of subsidies to relieve cost burdens of ownership and renting.

Market Data | Jun 18, 2018

AI is the path to maximum profitability for retail and FMCG firms

Leading retailers including Amazon, Alibaba, Lowe’s and Tesco are developing their own AI solutions for automation, analytics and robotics use cases.

Market Data | Jun 12, 2018

Yardi Matrix report details industrial sector's strength

E-commerce and biopharmaceutical companies seeking space stoke record performances across key indicators.

Market Data | Jun 8, 2018

Dodge Momentum Index inches up in May

May’s gain was the result of a 4.7% increase by the commercial component of the Momentum Index.

Market Data | Jun 4, 2018

Nonresidential construction remains unchanged in April

Private sector spending increased 0.8% on a monthly basis and is up 5.3% from a year ago.