The medical office and industrial sectors will drive what is expected to be moderate growth in the commercial real estate market this year, predict the real estate advisory teams of Transwestern and Devencore located in 43 U.S. and Canadian metros.

The biggest potential impediments to that growth could be rising build-out costs and regulations on how medical tenants can use space.

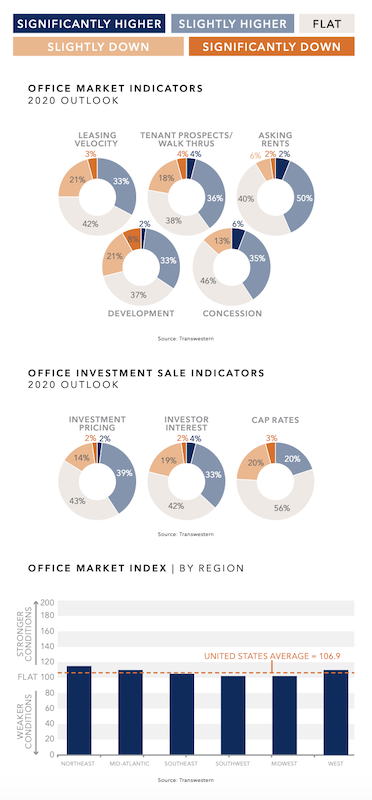

The survey (which can be downloaded from here) finds that conditions for the U.S. office market, while expected to improve, might still be down slightly from the previous year’s outlook. The Northeast, Mid-Atlantic, and West regions are expected to exhibit the strongest office demand. Two fifths of the survey’s respondents expect overall leasing velocity and tenant prospects to be flat this year, as tenants require more time to finalize their decisions.

Brokers and analysts are concerned about ebbing consumer confidence, given the upcoming elections and uncertain economy. Optimists, though, anticipate pockets of demand from tech and medical tenants. Brokers also expect tenant densification (measured by leased space per employee) to continue but at a decelerating pace from last year.

“Tenants are getting creative with space efficiency, with many opting to densify space in order to upgrade quality,” the survey observes.

Flat to slightly better conditions could prevail in most markets this year. Charts: Transwestern and Devencore

This trend might explain why respondents expect development pipelines to be only flat or slightly higher this year, with some markets showing signs of oversupply and rising construction costs. However, tenant leasing will remain intensely competitive, with concession packages staying at least even with 2019 or a bit higher, according to 81% of survey respondents.

About the same percentage think investment interest and pricing will be flat or rise slightly in 2020, and nearly three-fifths (56%) foresee flat capitalization.

The survey also looks at the markets for medical offices, industrial, and Canada’s office market. Its findings include the following:

•The medical office sector will “handsomely” outperform in 2020, with leasing activity, tenant walk throughs, asking rents and development all expected to be higher this year.

•Half of the respondents expect conditions for industrial to be healthy, albeit with slight deceleration in leasing velocity. And while brokers see some overbuilding occurring in markets like Houston and Dallas-Fort Worth, “generally, low supply, coupled with high demand from ecommerce, is forecasted to drive the market.”

•With the exception of Alberta, Canada’s major provinces—Ontario, British Columbia, and Quebec—should see leasing velocity and tenant prospects pick up this year. However, tenants are now taking anywhere from seven to 12 months to sign midsized deals.

Related Stories

Market Data | Oct 31, 2016

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.

Industry Research | Sep 27, 2016

Sterling Risk Sentiment Index indicates risk exposure perception remains stable in construction industry

Nearly half (45%) of those polled say election year uncertainty has a negative effect on risk perception in the construction market.