The medical office and industrial sectors will drive what is expected to be moderate growth in the commercial real estate market this year, predict the real estate advisory teams of Transwestern and Devencore located in 43 U.S. and Canadian metros.

The biggest potential impediments to that growth could be rising build-out costs and regulations on how medical tenants can use space.

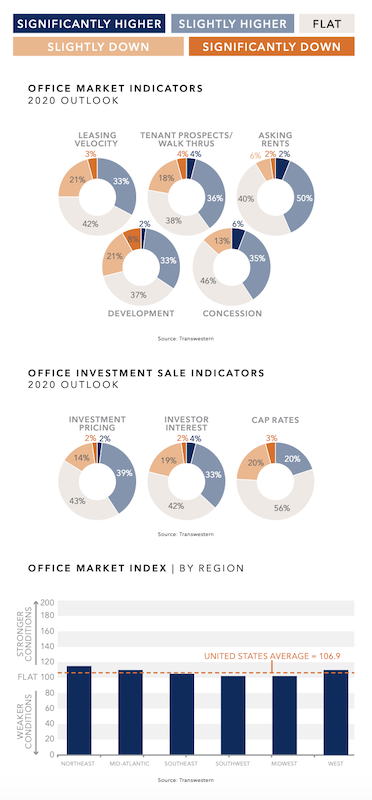

The survey (which can be downloaded from here) finds that conditions for the U.S. office market, while expected to improve, might still be down slightly from the previous year’s outlook. The Northeast, Mid-Atlantic, and West regions are expected to exhibit the strongest office demand. Two fifths of the survey’s respondents expect overall leasing velocity and tenant prospects to be flat this year, as tenants require more time to finalize their decisions.

Brokers and analysts are concerned about ebbing consumer confidence, given the upcoming elections and uncertain economy. Optimists, though, anticipate pockets of demand from tech and medical tenants. Brokers also expect tenant densification (measured by leased space per employee) to continue but at a decelerating pace from last year.

“Tenants are getting creative with space efficiency, with many opting to densify space in order to upgrade quality,” the survey observes.

Flat to slightly better conditions could prevail in most markets this year. Charts: Transwestern and Devencore

This trend might explain why respondents expect development pipelines to be only flat or slightly higher this year, with some markets showing signs of oversupply and rising construction costs. However, tenant leasing will remain intensely competitive, with concession packages staying at least even with 2019 or a bit higher, according to 81% of survey respondents.

About the same percentage think investment interest and pricing will be flat or rise slightly in 2020, and nearly three-fifths (56%) foresee flat capitalization.

The survey also looks at the markets for medical offices, industrial, and Canada’s office market. Its findings include the following:

•The medical office sector will “handsomely” outperform in 2020, with leasing activity, tenant walk throughs, asking rents and development all expected to be higher this year.

•Half of the respondents expect conditions for industrial to be healthy, albeit with slight deceleration in leasing velocity. And while brokers see some overbuilding occurring in markets like Houston and Dallas-Fort Worth, “generally, low supply, coupled with high demand from ecommerce, is forecasted to drive the market.”

•With the exception of Alberta, Canada’s major provinces—Ontario, British Columbia, and Quebec—should see leasing velocity and tenant prospects pick up this year. However, tenants are now taking anywhere from seven to 12 months to sign midsized deals.

Related Stories

Hotel Facilities | Jan 13, 2016

Hotel construction should remain strong through 2017

More than 100,000 rooms could be delivered this year alone.

Market Data | Jan 6, 2016

Census Bureau revises 10 years’ worth of construction spending figures

The largest revisions came in the last two years and were largely upward.

Market Data | Jan 5, 2016

Majority of AEC firms saw growth in 2015, remain optimistic for 2016: BD+C survey

By all indications, 2015 was another solid year for U.S. architecture, engineering, and construction firms.

Market Data | Jan 5, 2016

Nonresidential construction spending falters in November

Only 4 of 16 subsectors showed gains

Market Data | Dec 15, 2015

AIA: Architecture Billings Index hits another bump

Business conditions show continued strength in South and West regions.

Market Data | Dec 7, 2015

2016 forecast: Continued growth expected for the construction industry

ABC forecasts growth in nonresidential construction spending of 7.4% in 2016 along with growth in employment and backlog.