A rising tide of new office projects may be skewing the national average rental rate upward and obscuring increased leasing challenges for second-generation properties in many markets, Transwestern’s latest U.S. office market report suggests.

Monthly asking rent averaged $26.97 per square foot in the third quarter, representing a 3.4% increase from a year earlier and a five-year gain of 19.7%. Much of that national increase reflects above-market rents at new or renovated projects, where landlords have incurred elevated material and labor costs to complete amenity-rich offerings.

The national vacancy rate has plateaued near 9.8%, equal to the rate one year ago. A dozen of the 49 markets Transwestern tracks showed negative net absorption or an increase in the volume of vacant space for the 12 months ended September. Nationwide, annualized absorption through the third quarter was 57.3 million square feet, or roughly one-third less than the 85.2 million square feet absorbed in 2018.

Office construction is at a cyclical high. Building starts in the 12 months through the third quarter were up 12.1% over the year-ago period, with more than 166 million square feet of projects underway. The sector delivered 18.5 million square feet of new space in the recent quarter, less than the second quarter’s 21.7 million square feet but up 1.3% from a year earlier, while the national economy and average monthly job growth have slowed.

“Developers have responded vigorously to tenant preferences for new construction,” said Jimmy Hinton, Senior Managing Director of Investment & Analytics at Transwestern. “In many markets, new construction is outpacing already moderating tenant demand, creating extra pressure on older-vintage properties. Landlords are increasingly challenged in reconciling capital improvement needs with cycle timing and prospects for suitable investment returns.”

While high-end rents at new properties can increase a market’s average lease rate, new construction drives rent downward when landlords feel pressure to compete for tenants by lowering rates. In Houston, for example, average third quarter asking rent had declined 0.7% from a year earlier.

Stuart Showers, Vice President of Research in Houston, predicts other markets will experience a similar shift in the coming months, and could represent a late-cycle playbook for landlords in other markets, should macro conditions deteriorate.

“The volume of new office construction pushing through Houston has resulted in downward pressure on rental rates, a situation that will manifest throughout second-generation product in a number of the nation’s markets that have high construction activity,” Showers said.

Download the full third quarter 2019 U.S. office market report at: www.twurls.com/us-office-3q19

Related Stories

Market Data | Apr 20, 2021

Demand for design services continues to rapidly escalate

AIA’s ABI score for March rose to 55.6 compared to 53.3 in February.

Market Data | Apr 16, 2021

Construction employment in March trails March 2020 mark in 35 states

Nonresidential projects lag despite hot homebuilding market.

Market Data | Apr 13, 2021

ABC’s Construction Backlog slips in March; Contractor optimism continues to improve

The Construction Backlog Indicator fell to 7.8 months in March.

Market Data | Apr 9, 2021

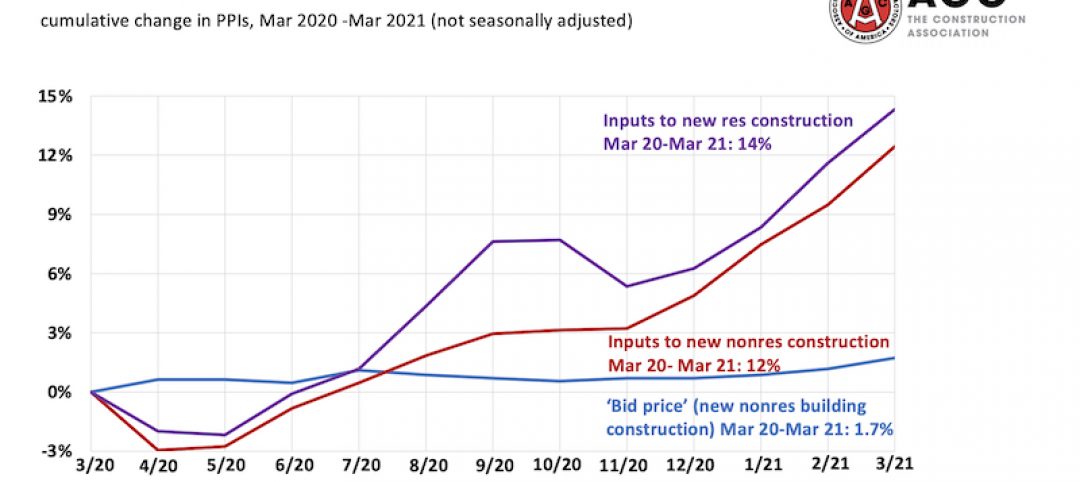

Record jump in materials prices and supply chain distributions threaten construction firms' ability to complete vital nonresidential projects

A government index that measures the selling price for goods used construction jumped 3.5% from February to March.

Contractors | Apr 9, 2021

Construction bidding activity ticks up in February

The Blue Book Network's Velocity Index measures month-to-month changes in bidding activity among construction firms across five building sectors and in all 50 states.

Industry Research | Apr 9, 2021

BD+C exclusive research: What building owners want from AEC firms

BD+C’s first-ever owners’ survey finds them focused on improving buildings’ performance for higher investment returns.

Market Data | Apr 7, 2021

Construction employment drops in 236 metro areas between February 2020 and February 2021

Houston-The Woodlands-Sugar Land and Odessa, Texas have worst 12-month employment losses.

Market Data | Apr 2, 2021

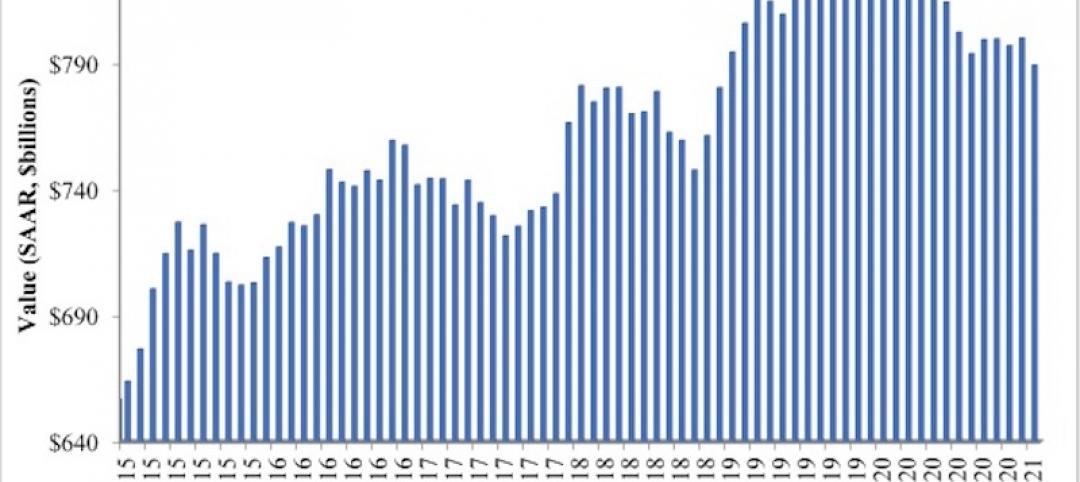

Nonresidential construction spending down 1.3% in February, says ABC

On a monthly basis, spending was down in 13 of 16 nonresidential subcategories.

Market Data | Apr 1, 2021

Construction spending slips in February

Shrinking demand, soaring costs, and supply delays threaten project completion dates and finances.

Market Data | Mar 26, 2021

Construction employment in February trails pre-pandemic level in 44 states

Soaring costs, supply-chain problems jeopardize future jobs.