A rising tide of new office projects may be skewing the national average rental rate upward and obscuring increased leasing challenges for second-generation properties in many markets, Transwestern’s latest U.S. office market report suggests.

Monthly asking rent averaged $26.97 per square foot in the third quarter, representing a 3.4% increase from a year earlier and a five-year gain of 19.7%. Much of that national increase reflects above-market rents at new or renovated projects, where landlords have incurred elevated material and labor costs to complete amenity-rich offerings.

The national vacancy rate has plateaued near 9.8%, equal to the rate one year ago. A dozen of the 49 markets Transwestern tracks showed negative net absorption or an increase in the volume of vacant space for the 12 months ended September. Nationwide, annualized absorption through the third quarter was 57.3 million square feet, or roughly one-third less than the 85.2 million square feet absorbed in 2018.

Office construction is at a cyclical high. Building starts in the 12 months through the third quarter were up 12.1% over the year-ago period, with more than 166 million square feet of projects underway. The sector delivered 18.5 million square feet of new space in the recent quarter, less than the second quarter’s 21.7 million square feet but up 1.3% from a year earlier, while the national economy and average monthly job growth have slowed.

“Developers have responded vigorously to tenant preferences for new construction,” said Jimmy Hinton, Senior Managing Director of Investment & Analytics at Transwestern. “In many markets, new construction is outpacing already moderating tenant demand, creating extra pressure on older-vintage properties. Landlords are increasingly challenged in reconciling capital improvement needs with cycle timing and prospects for suitable investment returns.”

While high-end rents at new properties can increase a market’s average lease rate, new construction drives rent downward when landlords feel pressure to compete for tenants by lowering rates. In Houston, for example, average third quarter asking rent had declined 0.7% from a year earlier.

Stuart Showers, Vice President of Research in Houston, predicts other markets will experience a similar shift in the coming months, and could represent a late-cycle playbook for landlords in other markets, should macro conditions deteriorate.

“The volume of new office construction pushing through Houston has resulted in downward pressure on rental rates, a situation that will manifest throughout second-generation product in a number of the nation’s markets that have high construction activity,” Showers said.

Download the full third quarter 2019 U.S. office market report at: www.twurls.com/us-office-3q19

Related Stories

Market Data | Apr 16, 2019

ABC’s Construction Backlog Indicator rebounds in February

ABC's Construction Backlog Indicator expanded to 8.8 months in February 2019.

Market Data | Apr 8, 2019

Engineering, construction spending to rise 3% in 2019: FMI outlook

Top-performing segments forecast in 2019 include transportation, public safety, and education.

Market Data | Apr 1, 2019

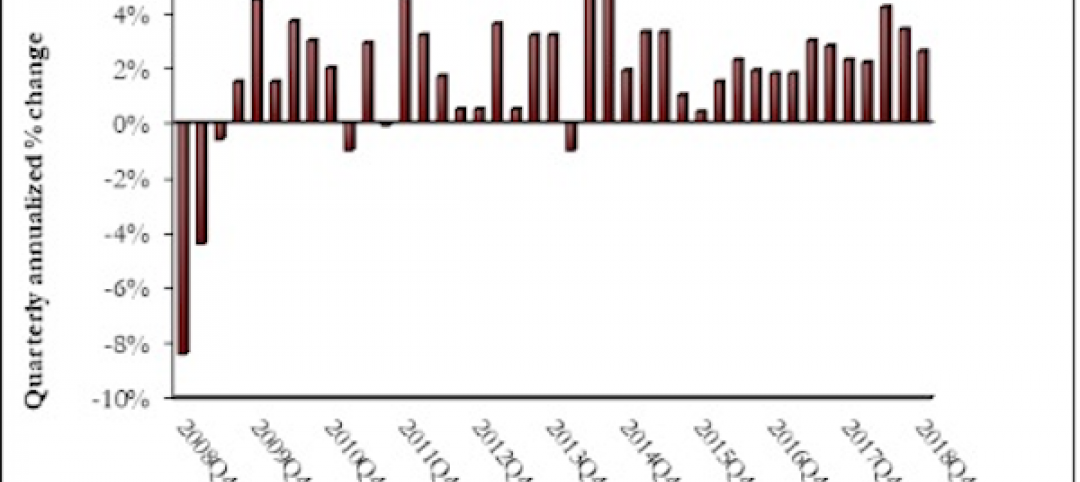

Nonresidential spending expands again in February

Private nonresidential spending fell 0.5% for the month and is only up 0.1% on a year-over-year basis.

Market Data | Mar 22, 2019

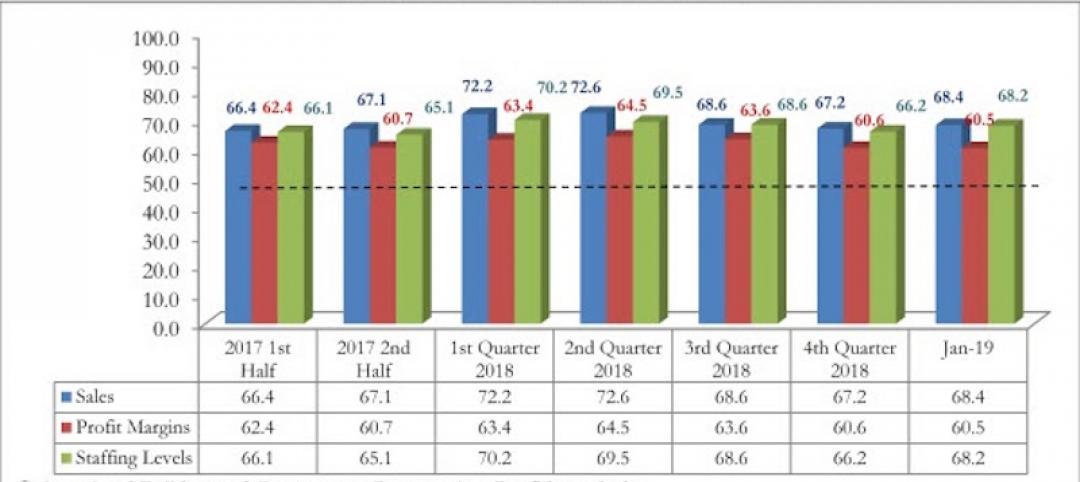

Construction contractors regain confidence in January 2019

Expectations for sales during the coming six-month period remained especially upbeat in January.

Market Data | Mar 21, 2019

Billings moderate in February following robust New Year

AIA’s Architecture Billings Index (ABI) score for February was 50.3, down from 55.3 in January.

Market Data | Mar 19, 2019

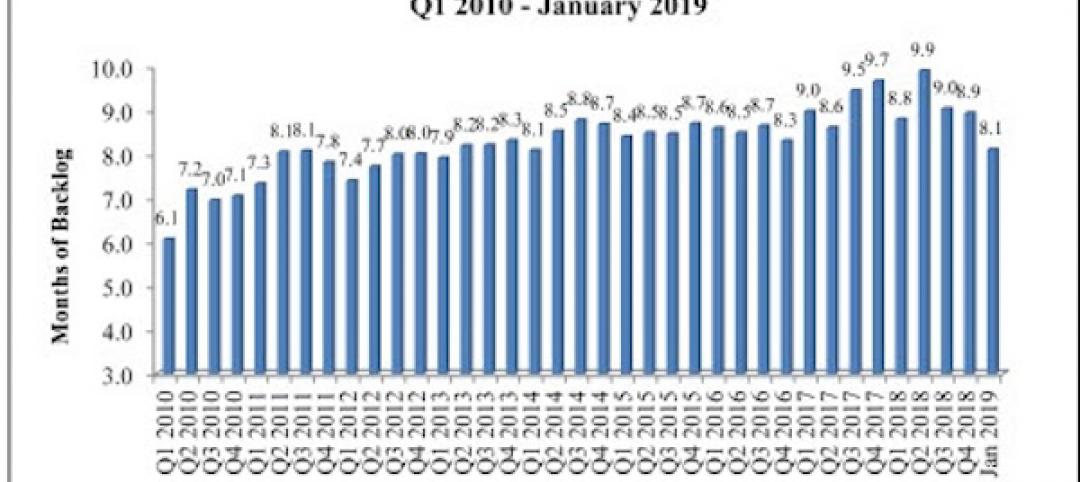

ABC’s Construction Backlog Indicator declines sharply in January 2019

The Construction Backlog Indicator contracted to 8.1 months during January 2019.

Market Data | Mar 15, 2019

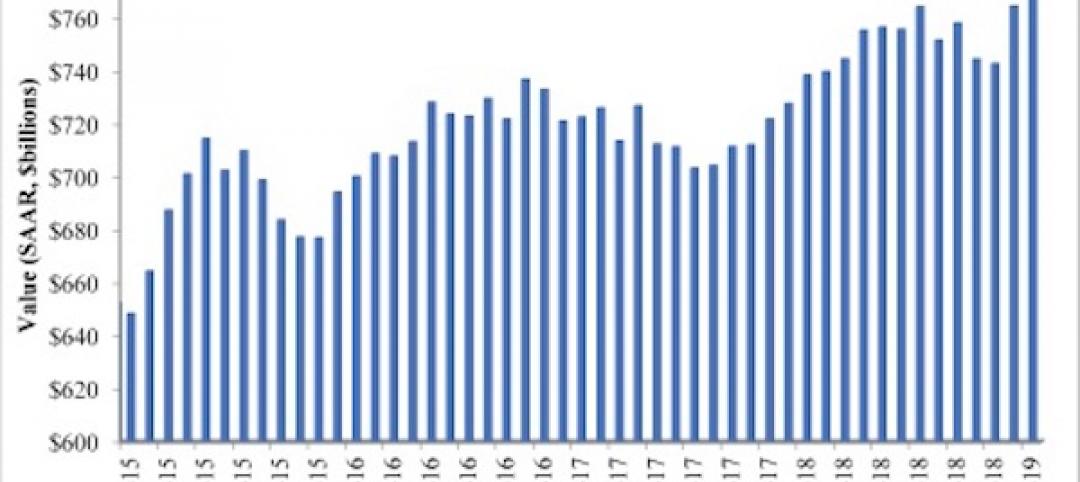

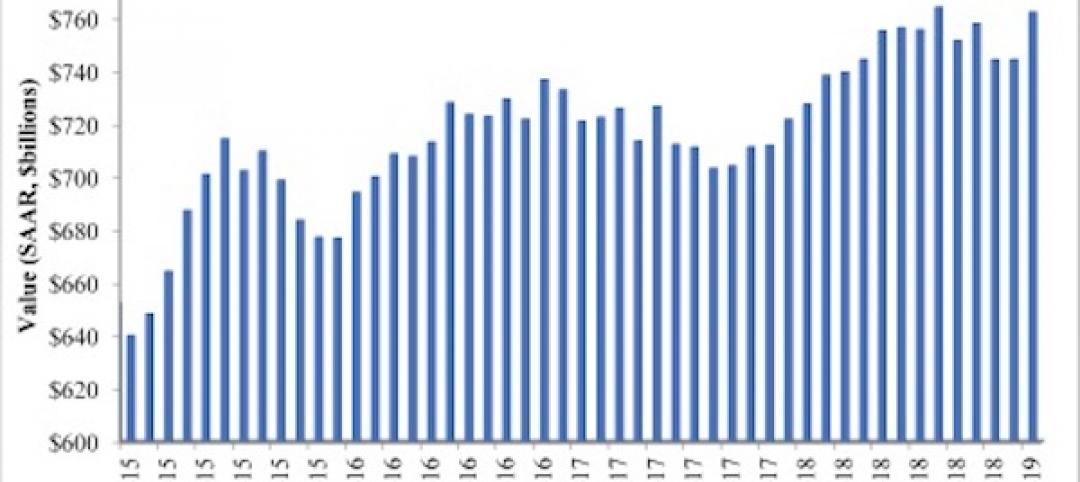

2019 starts off with expansion in nonresidential spending

At a seasonally adjusted annualized rate, nonresidential spending totaled $762.5 billion for the month.

Market Data | Mar 14, 2019

Construction input prices rise for first time since October

Of the 11 construction subcategories, seven experienced price declines for the month.

Market Data | Mar 6, 2019

Global hotel construction pipeline hits record high at 2018 year-end

There are a record-high 6,352 hotel projects and 1.17 million rooms currently under construction worldwide.

Market Data | Feb 28, 2019

U.S. economic growth softens in final quarter of 2018

Year-over-year GDP growth was 3.1%, while average growth for 2018 was 2.9%.