Financing solutions provider Billd recently surveyed nearly 900 commercial construction professionals across the U.S. for its 2023 National Subcontractor Market Report. Its key finding: rising input prices for materials and labor cost subcontractors $97 billion in unplanned expenses last year.

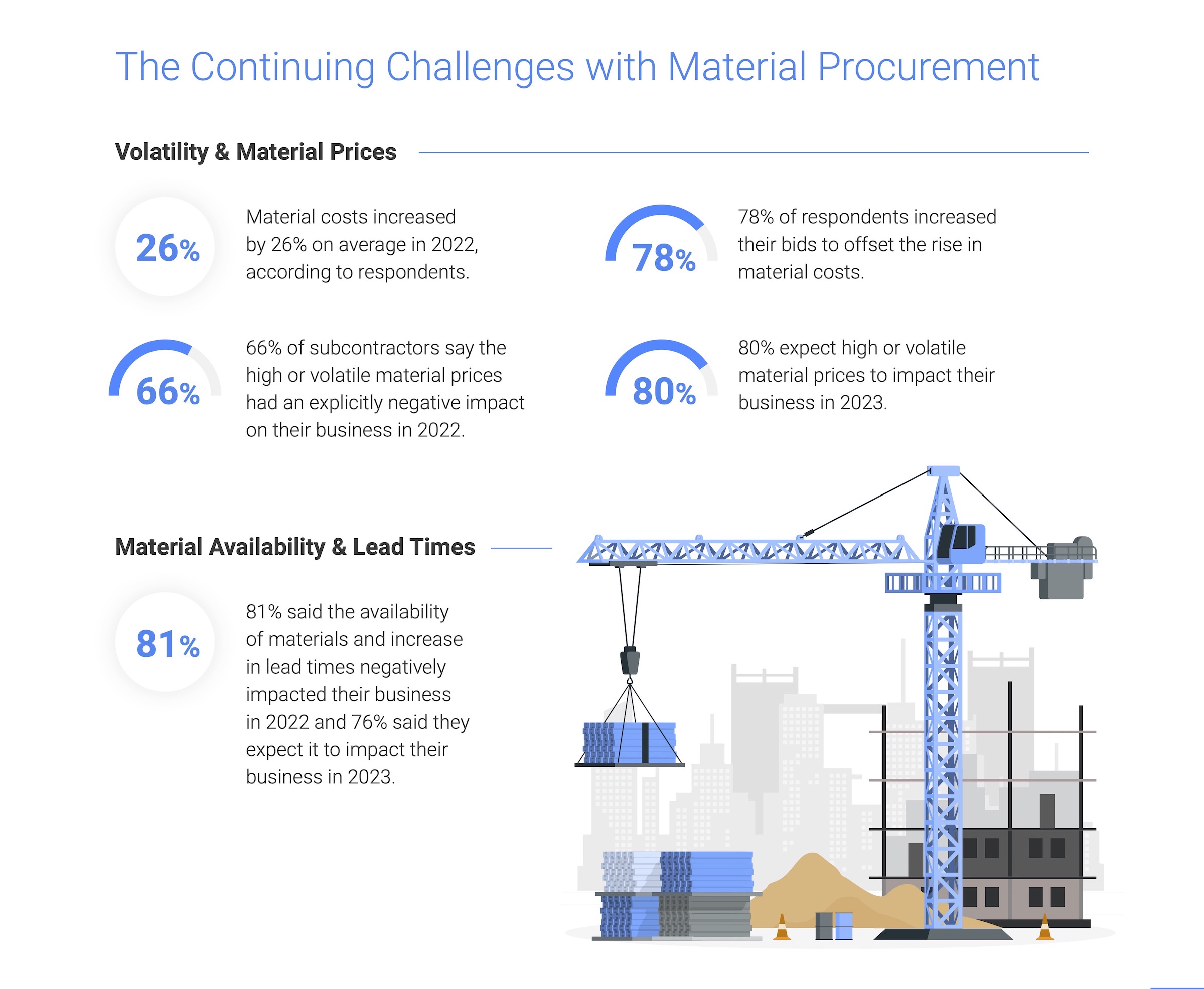

Rising material costs and price volatility are not new issues for subcontractors, with 81% of those surveyed reporting a negative effect on their businesses in 2022; 80% expect that trend to continue. It is no surprise given material costs jumped a staggering 26%, according to respondents. Similarly, competition for labor due to the longtime labor shortage was validated by a 15% average increase in labor cost. Together, those increases amounted to $97 billion in additional expenses for the subcontractor. While some subcontractors increased their bids to offset these rapidly rising costs, one third of respondents were unable to raise those bids commensurate with their expenses. This resulted in 57% of businesses reporting a decrease in profitability, despite 61% reporting revenue growth.

"Subcontractors are the foundation of the construction industry, providing all material and labor to complete a project," said Chris Doyle, CEO of Billd. "They purchase that material and pay for that labor upfront, not being paid for their work for 74 days, a result of the dysfunctional payment cycle. If you add unplanned expenses due to rising costs in material and labor, it puts an unrealistic burden on subcontractors to provide that foundation."

The report examines how macroeconomic conditions from this and prior years impacted subcontractors in 2022, as well as their outlook for 2023. It also creates hope by providing perspective on new financing options subcontractors can leverage as mainstays – like supplier terms – become less reliable. 72% of respondents report having supplier terms of 30 days or less. Compared to a 74-day average wait time for payment, it is no surprise that 51% deem the length of their terms insufficient.

Supplier terms also have an unforeseen cost; most suppliers (also surveyed) state that they offer discounts for upfront payment. Despite those disadvantages, 87% of respondents still rely on supplier terms as their predominant means of buying materials. When it comes to funding their increasing labor costs, traditional financing options are even less accessible, leaving 87% of respondents coming out of pocket for labor before getting paid themselves. Luckily, the report highlights financial relief for labor as well as materials.

Related Stories

75 Top Building Products | Nov 30, 2022

75 top building products for 2022

Each year, the Building Design+Construction editorial team evaluates the vast universe of new and updated products, materials, and systems for the U.S. building design and construction market. The best-of-the-best products make up our annual 75 Top Products report.

K-12 Schools | Nov 30, 2022

School districts are prioritizing federal funds for air filtration, HVAC upgrades

U.S. school districts are widely planning to use funds from last year’s American Rescue Plan (ARP) to upgrade or improve air filtration and heating/cooling systems, according to a report from the Center for Green Schools at the U.S. Green Building Council. The report, “School Facilities Funding in the Pandemic,” says air filtration and HVAC upgrades are the top facility improvement choice for the 5,004 school districts included in the analysis.

Retail Centers | Nov 29, 2022

'Social' tenants play a vital role in the health of the retail center market

After a long Covid-induced period when the public avoided large gatherings, owners of malls and retail lifestyle centers are increasingly focused on attracting tenants that provide opportunities for socialization. Pent-up demand for experiences involving gatherings of people is fueling renovations and redesigns of large retail developments.

Giants 400 | Nov 28, 2022

Top 130 Office Sector Contractors and CM Firms for 2022

Turner Construction, STO Building Group, Gilbane, and CBRE top the ranking of the nation's largest office sector contractors and construction management (CM) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Legislation | Nov 23, 2022

7 ways the Inflation Reduction Act will impact the building sector

HOK’s Anica Landreneau and Stephanie Miller and Smart Surfaces Coalition’s Greg Kats reveal multiple ways the IRA will benefit the built environment.

Multifamily Housing | Nov 22, 2022

10 compelling multifamily developments debut in 2022

A smart home tech-focused apartment complex in North Phoenix, Ariz., and a factory conversion to lofts in St. Louis highlight the notable multifamily developments to debut recently.

Industrial Facilities | Nov 16, 2022

Industrial building sector construction, while healthy, might also be flattening

For all the hoopla about the ecommerce boom and “last mile” order fulfillment driving demand for more warehouse and manufacturing space, construction of industrial buildings actually declined over the past five years, albeit marginally by 2.1% to $27.3 billion in 2022, according to estimates by IBIS World. Still, construction in this sector remains buzzy.

Wood | Nov 16, 2022

5 steps to using mass timber in multifamily housing

A design-assist approach can provide the most effective delivery method for multifamily housing projects using mass timber as the primary building element.

Giants 400 | Nov 14, 2022

Top 60 Airport Terminal Contractors + CM Firms for 2022

Hensel Phelps, Turner Construction, Walsh Group, and Holder Construction top the ranking of the nation's largest airport terminal contractors and construction management (CM) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Giants 400 | Nov 14, 2022

4 emerging trends from BD+C's 2022 Giants 400 Report

Regenerative design, cognitive health, and jobsite robotics highlight the top trends from the 519 design and construction firms that participated in BD+C's 2022 Giants 400 Report.