At the end of the first quarter of 2019, analysts at Lodging Econometrics (LE) reported that the total U.S. construction pipeline continued to expand with 5,647 projects/687,941 rooms, up a strong 7% by projects and 8% by rooms year-over-year (YOY). Pipeline totals are a mere 236 projects, or 4%, shy of the all-time high of 5,883 projects/785,547 rooms reached in the second quarter of 2008. The record should be pierced later in the year. Conversions and renovations are already at record levels.

Projects currently under construction stand at 1,709 projects/227,924 rooms with projects scheduled to start construction in the next 12 months at 2,429 projects/281,395 rooms. Projects in the early planning stage stand at 1,509 projects/178,622 rooms.

The upscale, upper-midscale, and midscale chain scales, all reached record-highs for both projects and rooms. Sixty-six percent of projects in the total pipeline are concentrated in two chain scales: upscale and upper midscale.

Annualized construction starts are at the highest level since 2008. In 2019, LE forecasts a 2.2% supply growth rate with 1,038 new hotels/118,385 rooms expected to open. For 2020, LE anticipates 1,174 new hotel openings and 128,598 rooms.

Hotel operations had a good quarter but mostly from expense improvements. Only 7 of the top 25 markets showed occupancy increases, quarter-over-quarter (QOQ). Only 11 markets had rev-par increases. Overall, U.S. demand growth was up 2.4% while supply was up 2%.

Leading Markets in the U.S. Hotel Construction Pipeline

In the first quarter of 2019, analysts at Lodging Econometrics (LE) report that the top five markets with the largest hotel construction pipelines are New York City with 170 projects/29,247 rooms. Next are Dallas and Los Angeles, both at record highs, with 163 projects/19,689 rooms and 158 projects/25,578 rooms, respectively. Houston follows with 151 projects/15,643 rooms, and Nashville with 116 projects/15,599 rooms.

Markets with the greatest number of projects already under construction are New York with 119 projects/20,068 rooms, Dallas with 48 projects/6,265 rooms, and Los Angeles with 42 projects/6,288 rooms. Houston has 36 projects/4,162 rooms while Nashville, Austin, and San Jose all have 34 projects presently under construction.

Reflective of the increasing pipeline, LE’s forecast for new hotel openings will continue to rise through 2020. In 2019, New York City tops the list with 63 new hotels expected to open with 9,605 rooms, followed by Dallas with 30 projects/3,604 rooms, Houston with 28 projects/3,342 rooms, Austin with 25 projects/2,512 rooms, and Nashville with 23 projects/3,030 rooms. In the 2020 forecast, New York continues to lead with the highest number of new hotels anticipated to open with 44 projects/6,225 rooms followed by Los Angeles with 35 projects/5,140 rooms and Dallas with 33 projects/4,163 rooms.

The number of markets where supply growth is now exceeding demand growth continues to increase. At the first quarter, 18 of the top 25 markets experienced the shift, up from 12 of the top 25 markets at the end of the fourth quarter of 2018.

Markets of concern where new supply is already outpacing demand and future new openings are forecasted to be high are Houston, New York, Dallas, and Los Angeles.

Related Stories

Market Data | Apr 11, 2023

Construction crane count reaches all-time high in Q1 2023

Toronto, Seattle, Los Angeles, and Denver top the list of U.S/Canadian cities with the greatest number of fixed cranes on construction sites, according to Rider Levett Bucknall's RLB Crane Index for North America for Q1 2023.

Contractors | Apr 11, 2023

The average U.S. contractor has 8.7 months worth of construction work in the pipeline, as of March 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator declined to 8.7 months in March, according to an ABC member survey conducted March 20 to April 3. The reading is 0.4 months higher than in March 2022.

Market Data | Apr 6, 2023

JLL’s 2023 Construction Outlook foresees growth tempered by cost increases

The easing of supply chain snags for some product categories, and the dispensing with global COVID measures, have returned the North American construction sector to a sense of normal. However, that return is proving to be complicated, with the construction industry remaining exceptionally busy at a time when labor and materials cost inflation continues to put pricing pressure on projects, leading to caution in anticipation of a possible downturn. That’s the prognosis of JLL’s just-released 2023 U.S. and Canada Construction Outlook.

Market Data | Apr 4, 2023

Nonresidential construction spending up 0.4% in February 2023

National nonresidential construction spending increased 0.4% in February, according to an Associated Builders and Contractors analysis of data published by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $982.2 billion for the month, up 16.8% from the previous year.

Multifamily Housing | Mar 24, 2023

Average size of new apartments dropped sharply in 2022

The average size of new apartments in 2022 dropped sharply in 2022, as tracked by RentCafe. Across the U.S., the average new apartment size was 887 sf, down 30 sf from 2021, which was the largest year-over-year decrease.

Multifamily Housing | Mar 14, 2023

Multifamily housing rent rates remain flat in February 2023

Multifamily housing asking rents remained the same for a second straight month in February 2023, at a national average rate of $1,702, according to the new National Multifamily Report from Yardi Matrix. As the economy continues to adjust in the post-pandemic period, year-over-year growth continued its ongoing decline.

Contractors | Mar 14, 2023

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of February 2023

Associated Builders and Contractors reported today that its Construction Backlog Indicator increased to 9.2 months in February, according to an ABC member survey conducted Feb. 20 to March 6. The reading is 1.2 months higher than in February 2022.

Industry Research | Mar 9, 2023

Construction labor gap worsens amid more funding for new infrastructure, commercial projects

The U.S. construction industry needs to attract an estimated 546,000 additional workers on top of the normal pace of hiring in 2023 to meet demand for labor, according to a model developed by Associated Builders and Contractors. The construction industry averaged more than 390,000 job openings per month in 2022.

Market Data | Mar 7, 2023

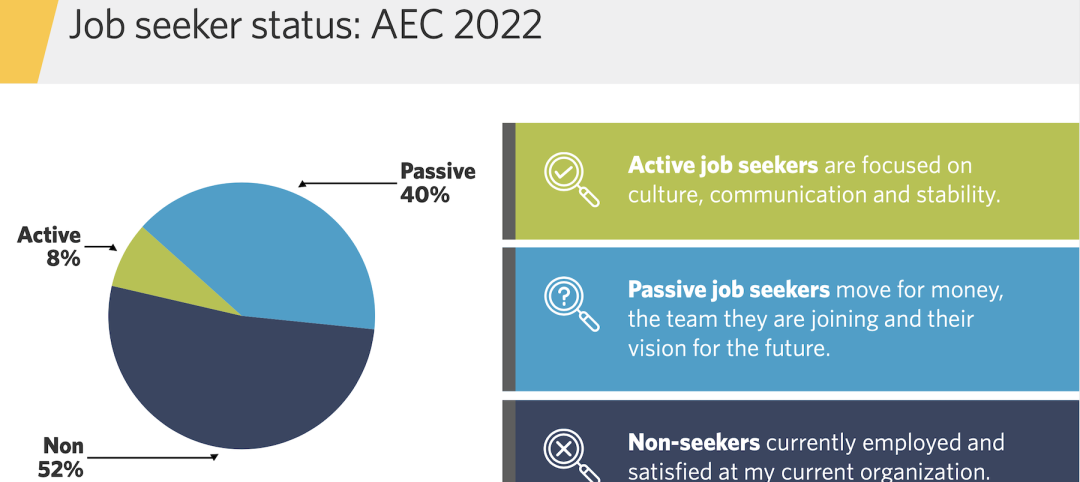

AEC employees are staying with firms that invest in their brand

Hinge Marketing’s latest survey explores workers’ reasons for leaving, and offers strategies to keep them in the fold.

Multifamily Housing | Feb 21, 2023

Multifamily housing investors favoring properties in the Sun Belt

Multifamily housing investors are gravitating toward Sun Belt markets with strong job and population growth, according to new research from Yardi Matrix. Despite a sharp second-half slowdown, last year’s nationwide $187 billion transaction volume was the second-highest annual total ever.