Though news reports and predictions painted a gloomy picture, the U.S. economy actually ended 2013 with a record setting year on Wall Street. The Dow Jones Industrial Average finished up 26.5%, its best return since 1995, and the S&P up nearly 30%, shattering previous records.

(See past articles from CBRE Healthcare)

Momentum continues to build in the housing market with positive trends in pricing, new housing starts, and inventory volume across the country. The U.S. economy added 74,000 jobs in December, as the unemployment rate fell to 6.7%, according to the Bureau of Labor Statistics.

With an improving economy and an unprecedented stimulus from the Federal Reserve continuing through 2014, the macro-economic outlook is good.

Healthcare Reform

Meanwhile, the healthcare industry has been rapidly evolving under the Affordable Care Act (ACA). Healthcare reform has compelled health systems, hospitals and physician groups to rein in sky-high costs while improving the quality of care, often coping with more regulatory requirements and less money.

Changes to reimbursement methods and reductions in healthcare provider compensation combined with an increased demand for healthcare services over the next five years, from an estimated 79 million aging baby boomers and 30 million newly insured patients, is forcing health systems to rethink their approach to balance sheet assets and liabilities, including health care real estate.

As health systems and physician groups change their delivery network, both healthcare service operators and owners of healthcare real estate are repositioning their portfolio requirements based on their growth needs. This has led to the highest medical office sales volume in the healthcare capital markets since 2007.

Healthcare reform incentives are driving consolidation of services in the industry, which has produced a robust mergers and acquisitions environment. As hospitals and healthcare organizations face mounting competitive, regulatory and financial challenges, leadership is seeking ways to capitalize on the increase of privately insured patients and Medicaid expansion while effectively serving the interests of their communities.

Healthcare operators need to diversify and expand their patient base while also becoming more efficient and leaner. This is most effectively achieved through greater economies of scale by merging with other health systems, hospitals, and physician groups, leading to a consolidation in the industry.

Consolidation is taking on two forms that are impacting real estate. First, is a unification of real estate assets as a result of health system mergers and physician employment, which has caused a consolidation of physician practices into fewer facilities that are strategically dispersed throughout the community. The other is consolidation among the hospitals and health systems seeking to concentrate operations in a single Metropolitan Statistical Area (MSA), region or state.

Off-Campus Healthcare

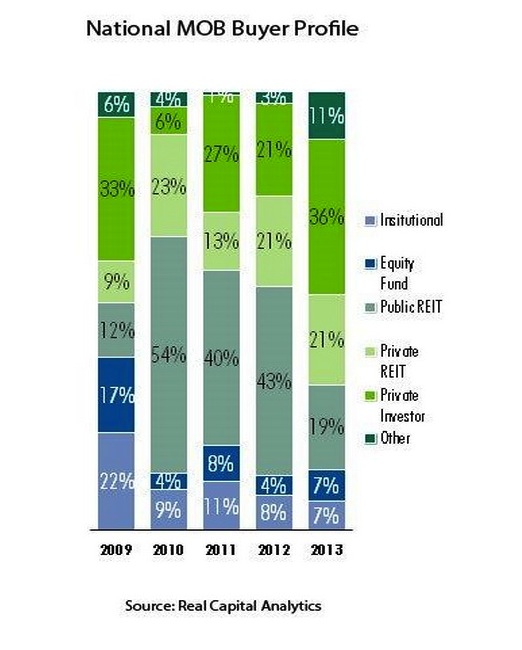

Healthcare investors are monitoring the consolidation trends and strategically aligning themselves through real estate transactions with market dominant hospitals and health systems, specifically those with investment grade credit ratings. Historically, investment in medical office properties revealed an institutional and REIT investor preference for core on-campus properties only.

However, over the past 12-18 months, we have witnessed little difference between core on-campus and core off-campus medical office buildings with meaningful hospital tenancy. This is a direct result of the health system shift to high quality healthcare delivered in outpatient facilities further away from traditional acute-care hospital campuses.

The care delivery network is moving from the busy, compact hospital campuses to off-campus outpatient settings with convenient access where patients live, work and shop. In response to healthcare providers commitment to off-campus destinations located near traditional retail properties and close to residential neighborhoods, investors have modified their investment criteria with a focus on off-campus properties.

The buyer pool for healthcare real estate has steadily increased over the last couple of years as investors continue to realize the inherent stability and higher returns for medical properties when compared to the more competitive multi-family, office, retail, and industrial real estate markets.

Public healthcare REITs have historically dominated the medical office investment market share, but in 2013 the private healthcare REITs and private capital investors took over the top slots. Listed and non-listed U.S. equity REITs (including both Public and Private) raised a total of $76.96 billion of equity and debt in 2013, an amount that surpassed 2012’s prior record of $73.33 billion, according to the National Association of Real Estate Investment Trusts (NAREIT). Nearly $9.3 billion, or roughly 12% was attributed to the Healthcare sector.

Conclusion

We anticipate another active year in healthcare capital markets for 2014. All investors will have stable access to capital and interest rates will likely remain at historic lows.

The favorable macro-economic outlook and consolidation among healthcare providers and continuous modification of the healthcare delivery model will continue to fuel the investment engine for what could be another record year in medical office sales.

About the authors

Lee Asher (Lee.Asher@cbre.com) and Chris Bodnar (Chris.Bodnar@cbre.com) are both Senior Vice Presidents with CBRE Healthcare Capital Markets Group. For more on CBRE Healthcare, visit www.cbre.com/healthcare.

Related Stories

Senior Living Design | Apr 24, 2024

Nation's largest Passive House senior living facility completed in Portland, Ore.

Construction of Parkview, a high-rise expansion of a Continuing Care Retirement Community (CCRC) in Portland, Ore., completed recently. The senior living facility is touted as the largest Passive House structure on the West Coast, and the largest Passive House senior living building in the country.

Hotel Facilities | Apr 24, 2024

The U.S. hotel construction market sees record highs in the first quarter of 2024

As seen in the Q1 2024 U.S. Hotel Construction Pipeline Trend Report from Lodging Econometrics (LE), at the end of the first quarter, there are 6,065 projects with 702,990 rooms in the pipeline. This new all-time high represents a 9% year-over-year (YOY) increase in projects and a 7% YOY increase in rooms compared to last year.

Architects | Apr 24, 2024

Shepley Bulfinch appoints new Board of Director: Evelyn Lee, FAIA

Shepley Bulfinch, a national architecture firm announced the appointment of new Board of Director member Evelyn Lee, FAIA as an outside director. With this new appointment, Lucia Quinn has stepped down from the firm’s Board, after serving many years as an outside board advisor and then as an outside director.

ProConnect Events | Apr 23, 2024

5 more ProConnect events scheduled for 2024, including all-new 'AEC Giants'

SGC Horizon present 7 ProConnect events in 2024.

75 Top Building Products | Apr 22, 2024

Enter today! BD+C's 75 Top Building Products for 2024

BD+C editors are now accepting submissions for the annual 75 Top Building Products awards. The winners will be featured in the November/December 2024 issue of Building Design+Construction.

Laboratories | Apr 22, 2024

Why lab designers should aim to ‘speak the language’ of scientists

Learning more about the scientific work being done in the lab gives designers of those spaces an edge, according to Adrian Walters, AIA, LEED AP BD+C, Principal and Director of SMMA's Science & Technology team.

Resiliency | Apr 22, 2024

Controversy erupts in Florida over how homes are being rebuilt after Hurricane Ian

The Federal Emergency Management Agency recently sent a letter to officials in Lee County, Florida alleging that hundreds of homes were rebuilt in violation of the agency’s rules following Hurricane Ian. The letter provoked a sharp backlash as homeowners struggle to rebuild following the devastating 2022 storm that destroyed a large swath of the county.

Mass Timber | Apr 22, 2024

British Columbia changing building code to allow mass timber structures of up to 18 stories

The Canadian Province of British Columbia is updating its building code to expand the use of mass timber in building construction. The code will allow for encapsulated mass-timber construction (EMTC) buildings as tall as 18 stories for residential and office buildings, an increase from the previous 12-story limit.

Standards | Apr 22, 2024

Design guide offers details on rain loads and ponding on roofs

The American Institute of Steel Construction and the Steel Joist Institute recently released a comprehensive roof design guide addressing rain loads and ponding. Design Guide 40, Rain Loads and Ponding provides guidance for designing roof systems to avoid or resist water accumulation and any resulting instability.

Building Materials | Apr 22, 2024

Tacoma, Wash., investigating policy to reuse and recycle building materials

Tacoma, Wash., recently initiated a study to find ways to increase building material reuse through deconstruction and salvage. The city council unanimously voted to direct the city manager to investigate deconstruction options and estimate costs.