Last year’s boon in single-family housing construction will have an impact on the availability and cost of building materials for nonresidential construction in 2021, which is expected to be a year of “decreasing work volume,” according to JLL’s latest Construction Forecast being released today.

Nonresidential starts were down 24% last year, and are expected to decline again in 2021. Yet, JLL sees an industry that has become more resilient and better positioned to function during the pandemic recovery.

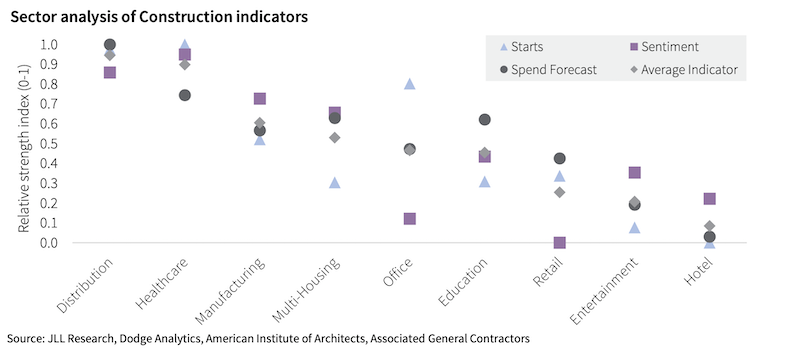

Healthcare and industrial should be the growth winners in construction spending this year. Chart: JLL

Healthcare and industrial should be the growth winners in construction spending this year. Chart: JLL

This recovery won’t be like the last one during the Great Recession in the late 2000s. For one thing, the range between sector forecasts is wider.

JLL analyzed three indicators of future growth: construction starts, construction industry sentiment, and forecast construction spending across nine nonresidential sectors. The clear winners, in its estimation, will be distribution and healthcare. The clear stragglers: hotels and entertainment. The office sector shows the least consensus.

LUMBER PRICING WILL CONTINUE TO BE VOLATILE

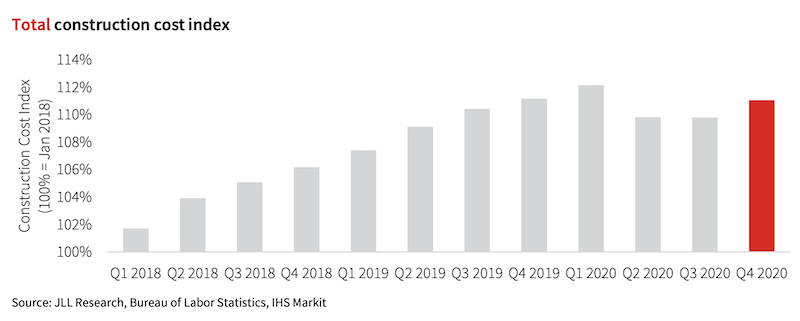

The boon in new-home construction is having an impact on overall construction costs. Chart: JLL

The boon in new-home construction is having an impact on overall construction costs. Chart: JLL

In addition, this has not been a total construction shutdown. Single-family housing starts increased by 11% last year, and have continued to grow since last May. (According to the latest Census Bureau estimates, single-family starts in January, at an annualized rate of 1,269,000 units, were up 29.9% over the same month in 2020.)

Residential construction employment was also up last year, by 1.2%, while nonres construction employment dipped 3.9%. That growth is affecting labor and materials markets. “The growth in residential is the primary cause of our forecast for elevated cost inflation in the coming year,” states JLL.

This year, it predicts that construction cost increases will be in the higher range between 3.5% and 5.5%. Labor costs will be up in the 2-5% range. Material costs will rise 4-6% and volatility “will remain elevated.” Nonres construction spending will stabilize from the early stages of the pandemic, but still decline between 5% and 8%, although JLL foresees an upswing in the third and fourth quarter, and more typical industry growth in 2022.

One silver lining from the pandemic is that it “spurred three years of construction tech adoption to be condensed into the last nine months of 2020,” observes JLL. It cites a recent Associated General Contractors survey that found contractors planning to increase their spending for all 14 ConTech categories listed.

Labor demand should also continue, although the key to any construction recovery, states JLL, will be how quickly the population is vaccinated against COVID-19. The industry’s labor shortage was a big enough buffer to absorb some of the pandemic’s shock, and through the entire post-pandemic period “there have been more active job openings in construction than at the peak of the last expansion in 2006-2007.”

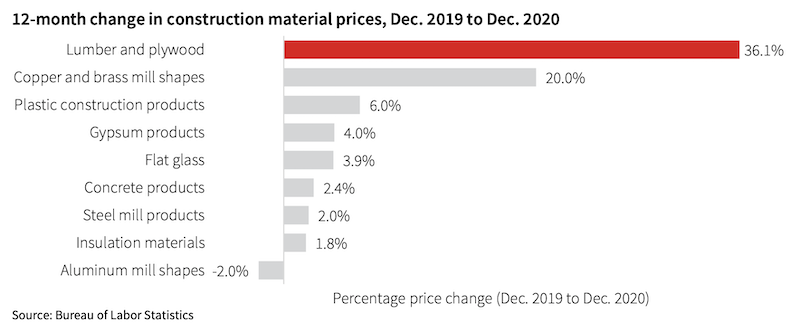

As for materials pricing, volatility will affect lumber, plywood, copper and brass mill shapes. The least volatile, price-wise, should be concrete, flat glass, insulation, and plastic construction products.

Lumber and plywood pricing is expected to remain unpredictable. Chart: JLL

Lumber and plywood pricing is expected to remain unpredictable. Chart: JLL

NEW ADMINISTRATION COULD SHAKE UP CONSTRUCTION

JLL weighed in on the potential impact of the Biden Administration on the construction industry. The next stimulus package, if passed by Congress, should keep the economy’s growth from reversing. A large infrastructure bill “is a good possibility later this year,” which JLL thinks could be an “accelerant” to construction inflation.

Interestingly, JLL doesn’t think either a reduction in immigration restrictions or an increase in the minimum wage to $15 per hour would have a substantive impact on projects, wages, or costs, except in states like Texas where construction wages are lower than the federal rate.

Related Stories

Designers | Oct 1, 2024

Global entertainment design firm WATG acquires SOSH Architects

Entertainment design firm WATG has acquired SOSH Architects, an interior design and planning firm based in Atlantic City, N.J.

Tom-Harris, courtesy Studio Gang")

Higher Education | Sep 30, 2024

Studio Gang turns tobacco warehouse into the new home of the University of Kentucky’s College of Design

Studio Gang has completed the Gray Design Building, the new home of the University of Kentucky’s College of Design. In partnership with K. Norman Berry Associates Architects, Studio Gang has turned a former tobacco warehouse into a contemporary facility for interdisciplinary learning and collaboration.

Warehouses | Sep 27, 2024

California bill would limit where distribution centers can be built

A bill that passed the California legislature would limit where distribution centers can be located and impose other rules aimed at reducing air pollution and traffic. Assembly Bill 98 would tighten building standards for new warehouses and ban heavy diesel truck traffic next to sensitive sites including homes, schools, parks and nursing homes.

Laboratories | Sep 27, 2024

Traditional lab design doesn't address neurodiverse needs, study finds

A study conducted by ARC, HOK, and the University of the West of Scotland, has revealed that half (48.1%) of all survey respondents who work in laboratory settings identify as neurodivergent.

Laboratories | Sep 26, 2024

BSL conversions: A cost-efficient method to support high-containment research

Some institutions are creating flexible lab spaces that can operate at a BSL-2 and modulate up to a BSL-3 when the need arises. Here are key aspects to consider when accommodating a rapid modulation between BSL-2 and BSL-3 space.

MFPRO+ News | Sep 24, 2024

Major Massachusetts housing law aims to build or save 65,000 multifamily and single-family homes

Massachusetts Gov. Maura Healey recently signed far-reaching legislation to boost housing production and address the high cost of housing in the Bay State. The Affordable Homes Act aims to build or save 65,000 homes through $5.1 billion in spending and 49 policy initiatives.

Designers | Sep 20, 2024

The growing moral responsibility of designing for shade

Elliot Glassman, AIA, NCARB, LEED AP BD+C, CPHD, Building Performance Leader, CannonDesign, makes the argument for architects to consider better shade solutions through these four strategies.

")

Mixed-Use | Sep 19, 2024

A Toronto development will transform a 32-acre shopping center site into a mixed-use urban neighborhood

Toronto developers Mattamy Homes and QuadReal Property Group have launched The Clove, the first phase in the Cloverdale, a $6 billion multi-tower development. The project will transform Cloverdale Mall, a 32-acre shopping center in Toronto, into a mixed-use urban neighborhood.

Codes and Standards | Sep 19, 2024

Navigating the intricacies of code compliance and authorities having jurisdiction

The construction of a building entails navigating through a maze of regulations, permits, and codes. Architects are more than mere designers; we are stewards of safety and navigators of code compliance.

Higher Education | Sep 18, 2024

Modernizing dental schools: The intersection of design and education

Page's John Smith and Jennifer Amster share the how firm's approach to dental education facilities builds on the success of evidence-based design techniques pioneered in the healthcare built environment.