Last year’s boon in single-family housing construction will have an impact on the availability and cost of building materials for nonresidential construction in 2021, which is expected to be a year of “decreasing work volume,” according to JLL’s latest Construction Forecast being released today.

Nonresidential starts were down 24% last year, and are expected to decline again in 2021. Yet, JLL sees an industry that has become more resilient and better positioned to function during the pandemic recovery.

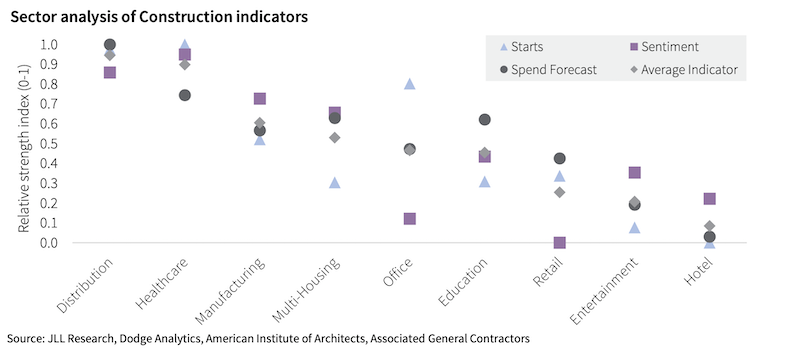

Healthcare and industrial should be the growth winners in construction spending this year. Chart: JLL

Healthcare and industrial should be the growth winners in construction spending this year. Chart: JLL

This recovery won’t be like the last one during the Great Recession in the late 2000s. For one thing, the range between sector forecasts is wider.

JLL analyzed three indicators of future growth: construction starts, construction industry sentiment, and forecast construction spending across nine nonresidential sectors. The clear winners, in its estimation, will be distribution and healthcare. The clear stragglers: hotels and entertainment. The office sector shows the least consensus.

LUMBER PRICING WILL CONTINUE TO BE VOLATILE

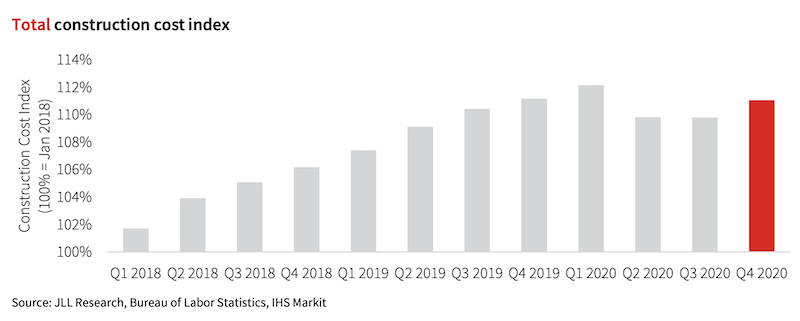

The boon in new-home construction is having an impact on overall construction costs. Chart: JLL

The boon in new-home construction is having an impact on overall construction costs. Chart: JLL

In addition, this has not been a total construction shutdown. Single-family housing starts increased by 11% last year, and have continued to grow since last May. (According to the latest Census Bureau estimates, single-family starts in January, at an annualized rate of 1,269,000 units, were up 29.9% over the same month in 2020.)

Residential construction employment was also up last year, by 1.2%, while nonres construction employment dipped 3.9%. That growth is affecting labor and materials markets. “The growth in residential is the primary cause of our forecast for elevated cost inflation in the coming year,” states JLL.

This year, it predicts that construction cost increases will be in the higher range between 3.5% and 5.5%. Labor costs will be up in the 2-5% range. Material costs will rise 4-6% and volatility “will remain elevated.” Nonres construction spending will stabilize from the early stages of the pandemic, but still decline between 5% and 8%, although JLL foresees an upswing in the third and fourth quarter, and more typical industry growth in 2022.

One silver lining from the pandemic is that it “spurred three years of construction tech adoption to be condensed into the last nine months of 2020,” observes JLL. It cites a recent Associated General Contractors survey that found contractors planning to increase their spending for all 14 ConTech categories listed.

Labor demand should also continue, although the key to any construction recovery, states JLL, will be how quickly the population is vaccinated against COVID-19. The industry’s labor shortage was a big enough buffer to absorb some of the pandemic’s shock, and through the entire post-pandemic period “there have been more active job openings in construction than at the peak of the last expansion in 2006-2007.”

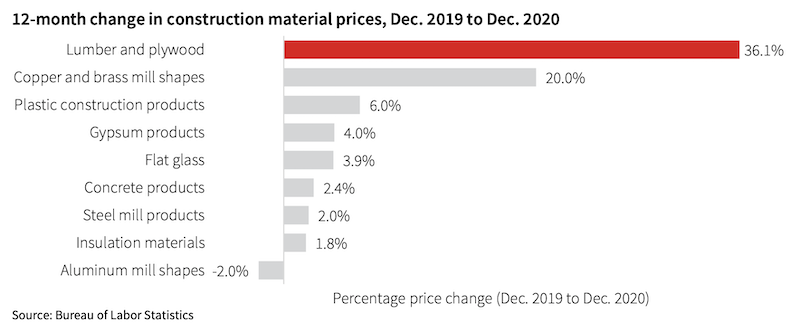

As for materials pricing, volatility will affect lumber, plywood, copper and brass mill shapes. The least volatile, price-wise, should be concrete, flat glass, insulation, and plastic construction products.

Lumber and plywood pricing is expected to remain unpredictable. Chart: JLL

Lumber and plywood pricing is expected to remain unpredictable. Chart: JLL

NEW ADMINISTRATION COULD SHAKE UP CONSTRUCTION

JLL weighed in on the potential impact of the Biden Administration on the construction industry. The next stimulus package, if passed by Congress, should keep the economy’s growth from reversing. A large infrastructure bill “is a good possibility later this year,” which JLL thinks could be an “accelerant” to construction inflation.

Interestingly, JLL doesn’t think either a reduction in immigration restrictions or an increase in the minimum wage to $15 per hour would have a substantive impact on projects, wages, or costs, except in states like Texas where construction wages are lower than the federal rate.

Related Stories

Sustainability | Jan 9, 2023

Innovative solutions emerge to address New York’s new greenhouse gas law

New York City’s Local Law 97, an ambitious climate plan that includes fines for owners of large buildings that don’t significantly reduce carbon emissions, has spawned innovations to address the law’s provisions.

Fire and Life Safety | Jan 9, 2023

Why lithium-ion batteries pose fire safety concerns for buildings

Lithium-ion batteries have become the dominant technology in phones, laptops, scooters, electric bikes, electric vehicles, and large-scale battery energy storage facilities. Here’s what you need to know about the fire safety concerns they pose for building owners and occupants.

Market Data | Jan 6, 2023

Nonresidential construction spending rises in November 2022

Spending on nonresidential construction work in the U.S. was up 0.9% in November versus the previous month, and 11.8% versus the previous year, according to the U.S. Census Bureau.

Industry Research | Dec 28, 2022

Following a strong year, design and construction firms view 2023 cautiously

The economy and inflation are the biggest concerns for U.S. architecture, construction, and engineering firms in 2023, according to a recent survey of AEC professionals by the editors of Building Design+Construction.

Performing Arts Centers | Dec 23, 2022

Diller Scofidio + Renfro's renovation of Dallas theater to be ‘faithful reinterpretation’ of Frank Lloyd Wright design

Diller Scofidio + Renfro recently presented plans to restore the Kalita Humphreys Theater at the Dallas Theater Center (DTC) in Dallas. Originally designed by Frank Lloyd Wright, this theater is the only freestanding theater in Wright’s body of work.

University Buildings | Dec 22, 2022

Loyola Marymount University completes a new home for its acclaimed School of Film and Television

California’s Loyola Marymount University (LMU) has completed two new buildings for arts and media education at its Westchester campus. Designed by Skidmore, Owings & Merrill (SOM), the Howard B. Fitzpatrick Pavilion is the new home of the undergraduate School of Film and Television, which is consistently ranked among the nation’s top 10 film schools. Also designed by SOM, the open-air Drollinger Family Stage is an outdoor lecture and performance space.

Adaptive Reuse | Dec 21, 2022

University of Pittsburgh reinvents century-old Model-T building as a life sciences research facility

After opening earlier this year, The Assembly recently achieved LEED Gold certification, aligning with the school’s and community’s larger sustainability efforts.

Multifamily Housing | Dec 20, 2022

Brooks + Scarpa-designed apartment provides affordable housing to young people aging out of support facilities

In Venice, Calif., the recently completed Rose Apartments provides affordable housing to young people who age out of youth facilities and often end up living on the street. Designed by Brooks + Scarpa, the four-story, 35-unit mixed-use apartment building will house transitional aged youths.

Coatings | Dec 20, 2022

The Pier Condominiums — What's old is new again!

When word was out that the condominium association was planning to carry out a refresh of the Pier Condominiums on Fort Norfolk, Hanbury jumped at the chance to remake what had become a tired, faded project.

Cladding and Facade Systems | Dec 20, 2022

Acoustic design considerations at the building envelope

Acentech's Ben Markham identifies the primary concerns with acoustic performance at the building envelope and offers proven solutions for mitigating acoustic issues.