Overcapacity in global iron ore production was a major factor in keeping construction costs low through the first four months of 2015. And for the first time in years, subcontractor labor costs showed signs of softening.

Those are two key findings in the latest assessment of current and future pricing from IHS, the Englewood, Colo.-based market analysis firm.

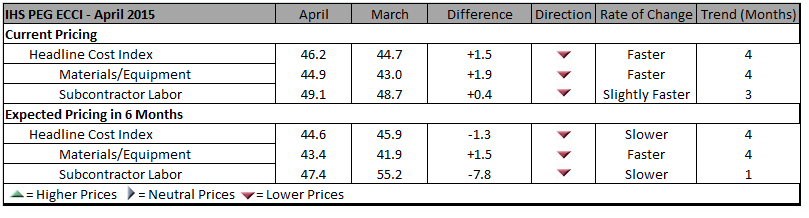

IHS derives its monthly Cost Index from information it receives from member procurement executives working for several of the world’s largest construction and engineering companies, including AECOM and Bechtel. It breaks down those data into current pricing trends and projections for six months forward.

In April, its Cost Index was 46.2, a bit higher than 44.7 in March, but still below what IHS would consider a “neutral” reading. Its sub index for Materials/Equipment costs in April was 44.9 compared to 43.0 in March. And the April sub index for Subcontractor Labor costs stood at 49.1, compared to 48.7 in March.

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

IHS notes that eight of 12 construction components it tracks registered falling prices in April, led by carbon steel pipe and fabricated structural steel. Both are victims of “bloated capacity, weak profit growth, and lackluster demand,” explains John Anton, IHS’s Director of Steel Services. Iron ore companies that, in response to demand from China’s steel industry, have initiated massive projects whose capacity, so far, “is far ahead of demand,” and is holding prices down.

Anton adds that while the iron ore market may have some ostensible similarities to the recent decline of crude oil prices, what’s different is that iron ore producers have shown no inclinations toward cutting production to match demand. (IHS points out that three quarters of China’s mines are losing money.)

IHS also notes that several global construction and engineering firms, particularly those in the oil and gas sectors, have been taking a “wait and see” approach to investing in larger capital projects. “The capex environment has yet to thaw,” asserts Mark Eisinger, IHS’s senior economist.

While some markets, like the U.S. South, are still experiencing shortages in skilled subcontractor labor, manpower costs have been receding. For the third consecutive month, the U.S. did not register higher month-to-month labor costs in April. And for the first time in this survey’s history, projections about labor costs over the next six months are below the neutral mark. The six-month cost index for subcontractor labor fell to 47.4 in April, compared to 55.2 in March.

The forward-looking index for materials and equipment, at 43.4 April, rose from March’s record low of 41.9, even as 10 of 12 components showed falling price expectations.

Related Stories

Office Buildings | Mar 21, 2024

BOMA updates floor measurement standard for office buildings

The Building Owners and Managers Association (BOMA) International has released its latest floor measurement standard for office buildings, BOMA 2024 for Office Buildings – ANSI/BOMA Z65.1-2024.

Healthcare Facilities | Mar 18, 2024

A modular construction solution to the mental healthcare crisis

Maria Ionescu, Senior Medical Planner, Stantec, shares a tested solution for the overburdened emergency department: Modular hub-and-spoke design.

Codes and Standards | Mar 18, 2024

New urban stormwater policies treat rainwater as a resource

U.S. cities are revamping how they handle stormwater to reduce flooding and capture rainfall and recharge aquifers. New policies reflect a change in mindset from treating stormwater as a nuisance to be quickly diverted away to capturing it as a resource.

Plumbing | Mar 18, 2024

EPA to revise criteria for WaterSense faucets and faucet accessories

The U.S. Environmental Protection Agency (EPA) plans to revise its criteria for faucets and faucet accessories to earn the WaterSense label. The specification launched in 2007; since then, most faucets now sold in the U.S. meet or exceed the current WaterSense maximum flow rate of 1.5 gallons per minute (gpm).

MFPRO+ New Projects | Mar 18, 2024

Luxury apartments in New York restore and renovate a century-old residential building

COOKFOX Architects has completed a luxury apartment building at 378 West End Avenue in New York City. The project restored and renovated the original residence built in 1915, while extending a new structure east on West 78th Street.

Construction Costs | Mar 15, 2024

Retail center construction costs for 2024

Data from Gordian shows the most recent costs per square foot for restaurants, social clubs, one-story department stores, retail stores and movie theaters in select cities.

Healthcare Facilities | Mar 15, 2024

First comprehensive cancer hospital in Dubai to host specialized multidisciplinary care

Stantec was selected to lead the design team for the Hamdan Bin Rashid Cancer Hospital, Dubai’s first integrated, comprehensive cancer hospital. Named in honor of the late Sheikh Hamdan Bin Rashid Al Maktoum, the hospital is scheduled to open to patients in 2026.

Codes and Standards | Mar 15, 2024

Technical brief addresses the impact of construction-generated moisture on commercial roofing systems

A new technical brief from SPRI, the trade association representing the manufacturers of single-ply roofing systems and related component materials, addresses construction-generated moisture and its impact on commercial roofing systems.

Sports and Recreational Facilities | Mar 14, 2024

First-of-its-kind sports and rehabilitation clinic combines training gym and healing spa

Parker Performance Institute in Frisco, Texas, is billed as a first-of-its-kind sports and rehabilitation clinic where students, specialized clinicians, and chiropractic professionals apply neuroscience to physical rehabilitation.

Market Data | Mar 14, 2024

Download BD+C's March 2024 Market Intelligence Report

U.S. construction spending on buildings-related work rose 1.4% in January, but project teams continue to face headwinds related to inflation, interest rates, and supply chain issues, according to Building Design+Construction's March 2024 Market Intelligence Report (free PDF download).