Overcapacity in global iron ore production was a major factor in keeping construction costs low through the first four months of 2015. And for the first time in years, subcontractor labor costs showed signs of softening.

Those are two key findings in the latest assessment of current and future pricing from IHS, the Englewood, Colo.-based market analysis firm.

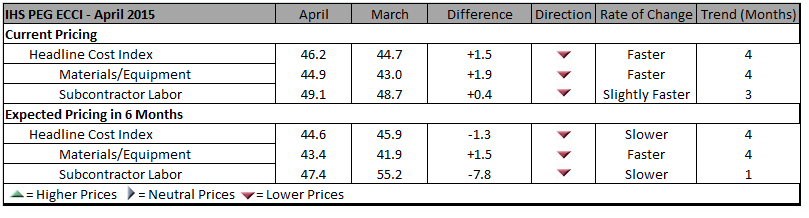

IHS derives its monthly Cost Index from information it receives from member procurement executives working for several of the world’s largest construction and engineering companies, including AECOM and Bechtel. It breaks down those data into current pricing trends and projections for six months forward.

In April, its Cost Index was 46.2, a bit higher than 44.7 in March, but still below what IHS would consider a “neutral” reading. Its sub index for Materials/Equipment costs in April was 44.9 compared to 43.0 in March. And the April sub index for Subcontractor Labor costs stood at 49.1, compared to 48.7 in March.

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

IHS notes that eight of 12 construction components it tracks registered falling prices in April, led by carbon steel pipe and fabricated structural steel. Both are victims of “bloated capacity, weak profit growth, and lackluster demand,” explains John Anton, IHS’s Director of Steel Services. Iron ore companies that, in response to demand from China’s steel industry, have initiated massive projects whose capacity, so far, “is far ahead of demand,” and is holding prices down.

Anton adds that while the iron ore market may have some ostensible similarities to the recent decline of crude oil prices, what’s different is that iron ore producers have shown no inclinations toward cutting production to match demand. (IHS points out that three quarters of China’s mines are losing money.)

IHS also notes that several global construction and engineering firms, particularly those in the oil and gas sectors, have been taking a “wait and see” approach to investing in larger capital projects. “The capex environment has yet to thaw,” asserts Mark Eisinger, IHS’s senior economist.

While some markets, like the U.S. South, are still experiencing shortages in skilled subcontractor labor, manpower costs have been receding. For the third consecutive month, the U.S. did not register higher month-to-month labor costs in April. And for the first time in this survey’s history, projections about labor costs over the next six months are below the neutral mark. The six-month cost index for subcontractor labor fell to 47.4 in April, compared to 55.2 in March.

The forward-looking index for materials and equipment, at 43.4 April, rose from March’s record low of 41.9, even as 10 of 12 components showed falling price expectations.

Related Stories

3D Printing | Sep 13, 2024

Swiss researchers develop robotic additive manufacturing method that uses earth-based materials—and not cement

Researchers at ETH Zurich, a university in Switzerland, have developed a new robotic additive manufacturing method to help make the construction industry more sustainable. Unlike concrete 3D printing, the process does not require cement.

Adaptive Reuse | Sep 12, 2024

White paper on office-to-residential conversions released by IAPMO

IAPMO has published a new white paper titled “Adaptive Reuse: Converting Offices to Multi-Residential Family,” a comprehensive analysis of addressing housing shortages through the conversion of office spaces into residential units.

Mixed-Use | Sep 10, 2024

Centennial Yards, a $5 billion mixed-use development in downtown Atlanta, tops out its first residential tower

Centennial Yards Company has topped out The Mitchell, the first residential tower of Centennial Yards, a $5 billion mixed-use development in downtown Atlanta. Construction of the apartment building is expected to be complete by the middle of next year, with first move-ins slated for summer 2025.

Contractors | Sep 10, 2024

The average U.S. contractor has 8.2 months worth of construction work in the pipeline, as of August 2024

Associated Builders and Contractors reported today that its Construction Backlog Indicator fell to 8.2 months in August, according to an ABC member survey conducted Aug. 20 to Sept. 5. The reading is down 1.0 months from August 2023.

Office Buildings | Sep 6, 2024

Fact sheet outlines benefits, challenges of thermal energy storage for commercial buildings

A U.S. Dept. of Energy document discusses the benefits and challenges of thermal energy storage for commercial buildings. The document explains how the various types of thermal energy storage technologies work, where their installation is most beneficial, and some practical considerations around installations.

Office Buildings | Sep 5, 2024

Office space downsizing trend appears to be past peak

The office downsizing trend may be past its peak, according to a CBRE survey of 225 companies with offices in the U.S., Canada, and Latin America. Just 37% of companies plan to shrink their office space this year compared to 57% last year, the survey found.

Codes and Standards | Sep 3, 2024

Atlanta aims to crack down on blighted properties with new tax

A new Atlanta law is intended to crack down on absentee landlords including commercial property owners and clean up neglected properties. The “Blight Tax” allows city officials to put levies on blighted property owners up to 25 times higher than current millage rates.

Resiliency | Sep 3, 2024

Phius introduces retrofit standard for more resilient buildings

Phius recently released, REVIVE 2024, a retrofit standard for more resilient buildings. The standard focuses on resilience against grid outages by ensuring structures remain habitable for at least a week during extreme weather events.

Construction Costs | Sep 2, 2024

Construction material decreases level out, but some increases are expected to continue for the balance Q3 2024

The Q3 2024 Quarterly Construction Insights Report from Gordian examines the numerous variables that influence material pricing, including geography, global events and commodity volatility. Gordian and subject matter experts examine fluctuations in costs, their likely causes, and offer predictions about where pricing is likely to go from here. Here is a sampling of the report’s contents.

Adaptive Reuse | Aug 29, 2024

More than 1.2 billion sf of office space have strong potential for residential conversion

More than 1.2 billion sf of U.S. office space—14.8% of the nation’s total—have strong potential for conversion to residential use, according to real estate software and services firm Yardi. Yardi’s new Conversion Feasibility Index scores office buildings on their suitability for multifamily conversion.