Construction employment continued to show strength across much of the United States through November 2017, when there were 191,000 more workers in the construction industry than during the same month a year earlier, and the construction unemployment rate fell by 0.7% to 5%, the lowest it’s been on record for the month of November, according to estimates released yesterday by Associated Builders and Contractors, a national trade group representing more than 21,000 members.

However, the industry still struggles with labor shortages that could be inhibiting investment and new construction.

During the first nine months of 2017, month-by-month employment growth was “minimal,” due primarily to “historically low unemployment” that limited the new construction talent pool, according to JLL’s Construction Outlook for the third quarter of 2017, which the market research and consulting firm released late last month.

During the third quarter of 2017, construction-related spending inched up by only 1.9% from the same period in 2016. “While topline spending is still increasing, consecutive quarters are demonstrating smaller and smaller gains over past years—underlining the trajectory towards a mature and stable industry,” JLL writes. Percentage growth of year-over-year spending decreased for nine out of the preceding 11 months, but was still above zero, “pointing to a tapering growth curve.”

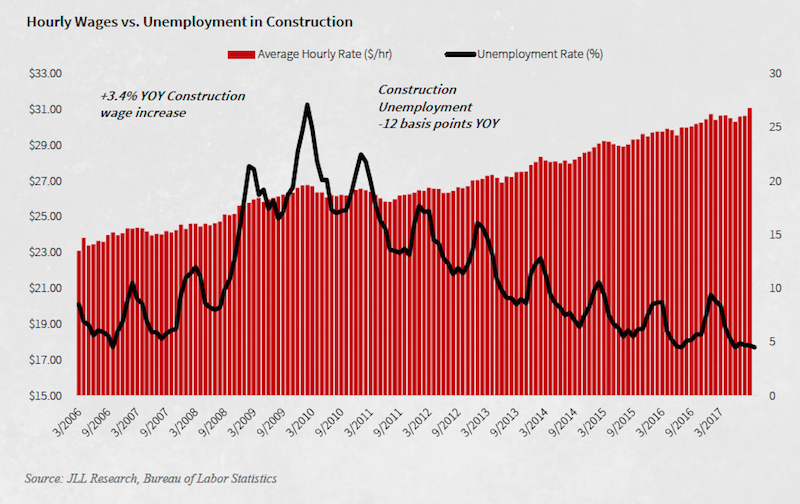

With qualified construction workers being harder to find, labor costs were volatile through the first nine months of last year. Image: JLL Research

Citing Census Bureau estimates, Associated Builders and Contractors posted that nonresidential construction spending declined in November by 1.3%, to $719.2 billion, compared to the same month a year earlier. Private nonres spending was down by 3.1%, while public-sector nonres spending grew by 1.7%. The gainers included commercial, educational, lodging, transportation, healthcare, and public safety. Manufacturing construction took the biggest hit, down 15.6%.

Commercial real estate has proven over the past several years that it can perform well regardless of how the economy in general is growing. “Right now we see little in fundamentals to cause concern about real estate as an asset class,” JLL writes.

Public construction, infrastructure and public works projects picked up steam during the third quarter of 2017, while single-family home construction grew at nearly double-digit annualized growth, which is expected to continue in 2018. Multifamily starts, on the other hand, dipped.

While the groundbreaking of large scale private commercial projects began to scale back due to stretched-out timelines, commercial renovation and fit-out work strengthened, and should prevail through the next several quarters and beyond into 2019, JLL predicts.

The cost of building slowed in the third quarter, up by just 3% from third quarter 2016. But it still grew faster than construction spending primarily because of increasing labor costs. (Wages grew by nearly 3.4%, on an annualized basis, in the third quarter of 2017.) Indeed, JLL expects labor shortages to persist through 2018, at least, and for construction costs to be up another 3% this year. JLL expects wage growth to accelerate, potentially hitting 5% or higher during peak building seasons.

The severe weather events that hit certain areas of the country had a surprisingly minor impact on the availability of most building materials. Nevertheless, materials costs rose by 3% in the third quarter compared to the same period a year ago, and those costs “are beginning to outpace current demand,” says JLL. Impending tariffs on Canadian lumber imports could jack up lumber prices for U.S. purchasers by 20% this year.

Manpower shortages, and the prospect that labor and products will cost more, could finally push the construction industry to embrace technology to a greater degree than it has done so to this point. JLL sees BIM, artificial intelligence and big data, and prefab and offsite construction as the three technologies that show the most promise this year.

Related Stories

Adaptive Reuse | Nov 1, 2023

Biden Administration reveals plan to spur more office-to-residential conversions

The Biden Administration recently announced plans to encourage more office buildings to be converted to residential use. The plan includes using federal money to lend to developers for conversion projects and selling government property that is suitable for conversions.

Sustainability | Nov 1, 2023

Tool identifies financial incentives for decarbonizing heavy industry, transportation projects

Rocky Mountain Institute (RMI) has released a tool to identify financial incentives to help developers, industrial companies, and investors find financial incentives for heavy industry and transport projects.

Contractors | Nov 1, 2023

Nonresidential construction spending increases for the 16th straight month, in September 2023

National nonresidential construction spending increased 0.3% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.1 trillion.

Sponsored | MFPRO+ Course | Oct 30, 2023

For the Multifamily Sector, Product Innovations Boost Design and Construction Success

This course covers emerging trends in exterior design and products/systems selection in the low- and mid-rise market-rate and luxury multifamily rental market. Topics include facade design, cladding material trends, fenestration trends/innovations, indoor/outdoor connection, and rooftop spaces.

Giants 400 | Oct 30, 2023

Top 170 K-12 School Architecture Firms for 2023

PBK Architects, Huckabee, DLR Group, VLK Architects, and Stantec top BD+C's ranking of the nation's largest K-12 school building architecture and architecture/engineering (AE) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Oct 30, 2023

Top 100 K-12 School Construction Firms for 2023

CORE Construction, Gilbane, Balfour Beatty, Skanska USA, and Adolfson & Peterson top BD+C's ranking of the nation's largest K-12 school building contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Oct 30, 2023

Top 80 K-12 School Engineering Firms for 2023

AECOM, CMTA, Jacobs, WSP, and IMEG head BD+C's ranking of the nation's largest K-12 school building engineering and engineering/architecture (EA) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

MFPRO+ Special Reports | Oct 27, 2023

Download the 2023 Multifamily Annual Report

Welcome to Building Design+Construction and Multifamily Pro+’s first Multifamily Annual Report. This 76-page special report is our first-ever “state of the state” update on the $110 billion multifamily housing construction sector.

Giants 400 | Oct 23, 2023

Top 115 Multifamily Construction Firms for 2023

Clark Group, Suffolk Construction, Summit Contracting Group, Whiting-Turner Contracting, and McShane Companies top the ranking of the nation's largest multifamily housing sector contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking factors revenue for all multifamily buildings work, including apartments, condominiums, student housing facilities, and senior living facilities.

Senior Living Design | Oct 19, 2023

Senior living construction poised for steady recovery

Senior housing demand, as measured by the change in occupied units, continued to outpace new supply in the third quarter, according to NIC MAP Vision. It was the ninth consecutive quarter of growth with a net absorption gain. On the supply side, construction starts continued to be limited compared with pre-pandemic levels.