A new report on office fit-out costs in North America sets out to establish a range of benchmarks for three different office styles, and to suggest what businesses favor which style.

JLL’s project and development services group, which produced the report, used data from more than 2,800 JLL-managed project budgets for over 100 clients from 17 industries in 59 markets throughout the U.S. and Canada.

The goal, says JLL, is to “elevate the conversation” around the real costs of building out various real estate designs. This year’s report includes office layout and space quality components to allow for evaluations of different office layouts, project complexities, and materials. It also provides high, medium, and low allowances for furniture, fixtures, and equipment (FFE); as well as for the installation of audio-visual and security equipment.

The result is an Office Fit Out Matrix, which shows how a handful of dynamics affect fit-out costs. Depending on the market and style, the costs range from $120.18 per sf to $216.07 per sf (see chart).

JLL breaks down these costs by region and metro market. The Northeast and Northwest consistently have higher fit-out costs. The medium costs in New York City are 28.5% above the U.S. average. In San Francisco, a fit-out would cost 22.6% more than the U.S. average. Conversely, the medium fit-out costs in West Palm Beach, Fla., are 15.9% below the national average; in Austin, Texas, 15.3% below.

This office fit-out matrix is based on data from over 2,800 project budgets in North America that JLL managed. Image: JLL

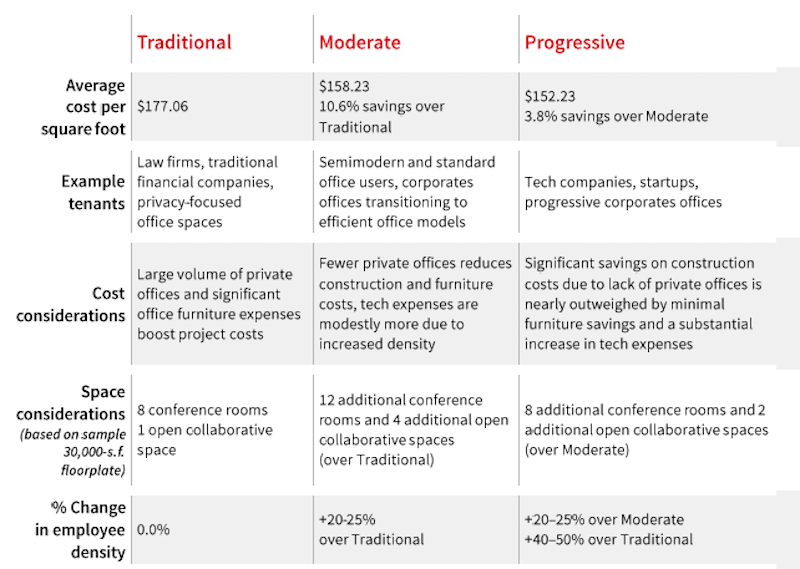

JLL's matrix compares the medium costs for fitting out three different office styles. Image: JLL

Three office styles examined

JLL divides its office fit-out costs along three styles:

• A Traditional office is still the most expensive to fit out. This style has the highest percentage of private office spaces, and typically between 20% and 50% fewer employees than the other two styles. Its FFE costs are the highest among the three styles, too. And tenant factors are “relatively small,” says JLL, because there is less common area. These offices are still favored by law firms, financial services companies, and businesses that focus on privacy with their offices.

JLL observes that some Traditional office styles are introducing lower-partition bench desks.

• A less-expensive fit-out, a Moderate office style features “agile” floorplans, with 10% dedicated to enclosed offices, and the rest of the space open with 6x6-foot workstations and minimal benching and guest space. Moderate offices—which are 20-25% less dense than Progressive office styles—include a healthy mix of conference rooms, and a few multipurpose and collaborative spaces. The hard fit-out costs for the Moderate style are average, but cost efficiencies can be captured by adding more bench-style desks.

• The Progressive office style is distinguished by an open floorplan, 100% of its desk space outfitted as bench-style furniture with zero enclosed spaces. This style’s focus is on activity-based working. Its employee density is 20-50% higher than a Traditional office, and it has double the amount of collaborative and conference spaces. (A standard plan would include 20 conference rooms and seven open collaborative/multi-use spaces.)

JLL points out that Progressive fit-outs generally have higher technology costs, but save money on FFE spending.

Landlords allowing for more upgrades

Last year, nearly 69 million sf of new office space were delivered to the market, but only 47.4% was preleased. JLL’s report observes that landlords are spending more to compete for tenants that are consistently gravitating toward high-quality spaces and assets. Consequently, landlords are offering better tenant improvement packages.

JLL cites several reasons for this trend, including the steady climb in construction costs, which increased on average by 15% last year. Landlords also offer better tenant improvement packages to offset the impact of higher rents.

The national average for tenant improvement allowances was $44 per sf, ranging from $105/sf in Washington D.C. to $28/sf in Nashville.

The report provides detailed snapshots of several markets, such as Austin, one of the country’s dynamic office markets, with robust growth supply. There are 3.1 million sf of new office space in Austin’s pipeline, 36% of which is preleased. The average tenant improvement allowance there last year was $45/sf.

There’s 7 million sf of new office space in the pipeline in San Francisco, where the office vacancy rate is 9.1%, and 68.8% of new space is preleased. The average tenant improvement allowance in San Francisco last year was $60/sf.

Related Stories

Giants 400 | Jan 29, 2024

Top 80 Workplace Interior Construction Firms for 2023

STO Building Group, HITT Contracting, Clune Construction, Hensel Phelps, and JRM Construction Management top BD+C's ranking of the nation's largest workplace interior and interior fitout general contractors and construction management (CM) firms for 2023, as reported in the 2023 Giants 400 Report.

Giants 400 | Jan 29, 2024

Top 50 Workplace Interior Engineering Firms for 2023

AECOM, Jacobs, Alfa Tech Consulting Engineers, Tetra Tech High Performance Buildings Group, and IMEG top BD+C's ranking of the nation's largest workplace interior and interior fitout engineering and engineering/architecture (EA) firms for 2023, as reported in the 2023 Giants 400 Report.

Giants 400 | Jan 29, 2024

Top 160 Workplace Interior Architecture Firms for 2023

Gensler, Interior Architects, HOK, SmithGroup, and Perkins&Will top BD+C's ranking of the nation's largest workplace interior and interior fitout architecture and architecture engineering (AE) firms for 2023, as reported in the 2023 Giants 400 Report.

Giants 400 | Jan 29, 2024

Top 100 Office Core and Shell Construction Firms for 2023

Turner Construction, AECOM, DPR Construction, Clark Group, and Clayco top BD+C's ranking of the nation's largest office core and shell general contractors and construction management (CM) firms for 2023, as reported in the 2023 Giants 400 Report.

Mixed-Use | Jan 29, 2024

12 U.S. markets where entertainment districts are under consideration or construction

The Pomp, a 223-acre district located 10 miles north of Fort Lauderdale, Fla., and The Armory, a 225,000-sf dining and entertainment venue on six acres in St Louis, are among the top entertainment districts in the works across the U.S.

Office Buildings | Jan 24, 2024

Office designs need to lean in on wellness, says a new HMC Architects report

The firm highlights seven recent design projects for public-sector clients as examples.

Industry Research | Jan 23, 2024

Leading economists forecast 4% growth in construction spending for nonresidential buildings in 2024

Spending on nonresidential buildings will see a modest 4% increase in 2024, after increasing by more than 20% last year according to The American Institute of Architects’ latest Consensus Construction Forecast. The pace will slow to just over 1% growth in 2025, a marked difference from the strong performance in 2023.

Adaptive Reuse | Jan 23, 2024

Adaptive reuse report shows 55K impact of office-to-residential conversions

The latest RentCafe annual Adaptive Reuse report shows that there are 55,300 office-to-residential units in the pipeline as of 2024—four times as much compared to 2021.

Giants 400 | Jan 23, 2024

Top 70 Medical Office Building Construction Firms for 2023

PCL Construction Enterprises, Swinerton, Skanska USA, Clark Group, and Hensel Phelps top BD+C's ranking of the nation's largest medical office building general contractors and construction management (CM) firms for 2023, as reported in the 2023 Giants 400 Report.

Giants 400 | Jan 23, 2024

Top 50 Medical Office Building Engineering Firms for 2023

Jacobs, Salas O'Brien, KPFF Consulting Engineers, IMEG, and Kimley-Horn head BD+C's ranking of the nation's largest medical office building engineering and engineering/architecture (EA) firms for 2023, as reported in the 2023 Giants 400 Report.