Nearly half of the respondents (46.1%) to an exclusive Building Design+Construction survey of AEC professionals reported that revenues had increased this year compared to 2012, with another 24.2% saying cash flow had stayed the same.

The majority (56.8%) of respondents—architects, engineers, contractors, building owners, and others in the commercial, industrial, multifamily, and institutional field—said their firms will bump up revenues next year, with 31.4% saying business will stay the same and only 11.8% predicting it will decline. A majority (55.5%) rated the health of their firms as good (35.6%) or very good (19.9%).

As has been the case in recent years, the overwhelming majority (71.2%) rated “general economic conditions (i.e., recession)” as the most important concern their firms will face in 2014.

Competition from other firms went up as a factor for the third year in a row, to 47.6% (44.9% in 2012, 40.1% in 2011). Nearly four in five respondents (79.3%) described the current business climate for their firms as “very” to “intensely” competitive; that’s up somewhat from 73.4% in 2012 and 74.8% in 2011. But “having insufficient capital funding for projects” declined slightly, to 24.1% of respondents, down from 29.7% in 2012 and 34.5% in 2011.

AEC respondents to this third annual survey of BD+C subscribers were still worried about the economy. On the other hand, “avoiding layoffs” (17.6%), “avoiding benefit reductions” (16.4%), and “keeping staff motivated” (14.6%) were of less concern.

DATA CENTERS CONTINUE THEIR SURGE INTO 2014

Asked to rate their firms’ prospects in specific construction sectors on a five-point scale from “excellent” to “very weak,” respondents gave data centers high marks. (Note: Respondents who checked “Not applicable/No opinion/Don’t know” are not counted here.) Among the findings:

• Data centers and mission-critical facilities continued to show strength, with the majority (56.0%) of respondents in the good/excellent category, compared to 52.1% last year and 45.2% the year before.

• Healthcare continued its leadership as the most highly desirable sector, with more than three in five respondents (62.5%) giving it a good to excellent rating, up from 58.8% last year.

• The apartment boom registered with AEC professionals, who gave multifamily housing a 56.1% good/excellent rating.

• Industrial/warehouse facilities keep moving up in the AEC psyche, registering a 33.0% interest level on the good/excellent scale, a significant climb from last year’s 25.5%.

• Retail commercial construction also showed vitality. Nearly a third of respondents (31.4%) came out on the good/excellent side for the coming year, well up from last year’s 19.9% rating.

• Nearly two-thirds of those surveyed (66.0%) said senior and assisted-living facilities look like good/excellent prospects for their firms, significantly up from last year’s healthy 50.5%. Hello, baby boomers!

• College and university facilities got the nod from 44.8% of respondents on the good to excellent scale, up from 37.8% last year.

As for government/military projects, the survey was taken before the full impact of the sequestration was known. The sector was rated good to excellent by 33.7% of respondents, much along the lines of last year’s 36.1% of respondents, down slightly from the previous year’s 41.1%.

While the construction of new office buildings drew tepid response (26.9%) in the good/excellent scale, that was still up significantly from last year’s 15.6% rating. However, a solid majority (52.1%) of respondents said office fitouts and interior renovations look good to excellent for 2014. That was likely a statistically significant leap from last year’s 35.7% who said office interiors would be a strong sector.

Respondents said their firms will likely use multiple strategies to stay ahead of the game in 2014. Only a small percentage (3.2%) said they think their companies will open a new office in the U.S. or Canada, while 4.5% said their firms might open an international office.

In fact, reconstruction, historic preservation, and renovations accounted for at least 25% of work for more than a third (38.5%) of respondents, up slightly from the 34.6% of respondents’ firms in 2012 and roughly the same as in 2011 (36.3%).

K-12 schools perked up a bit, with 30.9% saying the sector looks good to excellent for 2014, compared with 22.9% last year and 23.2% the year before.

TAKING ON THE DEMANDS OF BIM/VDC TECHNOLOGY

What about BIM? Is its promise holding true? Somewhat surprisingly, more than one in five respondents (22.7%) said their firms do not use building information modeling, about what was recorded over the previous two years.

Remarkably, precisely the same percentage of respondents (26.8%) said their firms used BIM in the majority of projects based on dollar value as in the last two annual surveys. Nearly two in five (39.8%) said their firms’ use of BIM will rise in the coming year; similarly, two-fifths (42.2%) of respondents said their companies will be investing more in technology in 2014.

As for social media, LinkedIn remained the top choice of respondents, at 53.1%, but that was a steep decline from last year’s 85.1% for LinkedIn. Facebook also took a hit, dropping to 32.5% in popularity, versus 49.5% last year, while Twitter dropped from 21.1% last year to 13.4%. Once again, a big chunk of respondents (31.3%) said they did not use social media channels.

Of the 400 who gave their professional description, 45.0% were architects; 8.0%, engineers; 28.8%, contractors; 9.8%, building owners, developers, or facility managers; and 8.6%, consultants or “other.” The margin of error was 4.8% at the 95% confidence level.

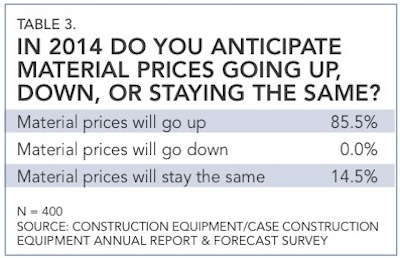

Respondents overwhelmingly said they expect prices of materials to rise in the coming year, with no respondents saying they expect such prices to fall.

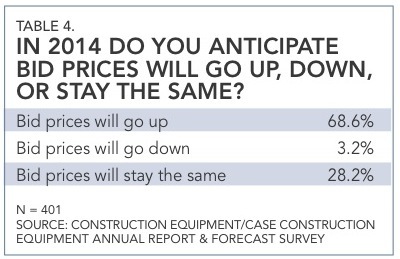

More than two-thirds of respondents (68.6%) said they expect bid prices to go up next year. Survey results have a margin of error of 4.8%.

For more on AEC firms' financial performance, see BD+C's 2013 Giants 300 Report.

Related Stories

| Aug 11, 2010

PBK, DLR Group among nation's largest K-12 school design firms, according to BD+C's Giants 300 report

A ranking of the Top 75 K-12 School Design Firms based on Building Design+Construction's 2009 Giants 300 survey. For more Giants 300 rankings, visit http://www.BDCnetwork.com/Giants

| Aug 11, 2010

Turner Building Cost Index dips nearly 4% in second quarter 2009

Turner Construction Company announced that the second quarter 2009 Turner Building Cost Index, which measures nonresidential building construction costs in the U.S., has decreased 3.35% from the first quarter 2009 and is 8.92% lower than its peak in the second quarter of 2008. The Turner Building Cost Index number for second quarter 2009 is 837.

| Aug 11, 2010

AGC unveils comprehensive plan to revive the construction industry

The Associated General Contractors of America unveiled a new plan today designed to revive the nation’s construction industry. The plan, “Build Now for the Future: A Blueprint for Economic Growth,” is designed to reverse predictions that construction activity will continue to shrink through 2010, crippling broader economic growth.

| Aug 11, 2010

New AIA report on embassies: integrate security and design excellence

The American Institute of Architects (AIA) released a new report to help the State Department design and build 21st Century embassies.

| Aug 11, 2010

Section Eight Design wins 2009 Open Architecture Challenge for classroom design

Victor, Idaho-based Section Eight Design beat out seven other finalists to win the 2009 Open Architecture Challenge: Classroom, spearheaded by the Open Architecture Network. Section Eight partnered with Teton Valley Community School (TVCS) in Victor to design the classroom of the future. Currently based out of a remodeled house, students at Teton Valley Community School are now one step closer to getting a real classroom.