Nearly half of the respondents (46.1%) to an exclusive Building Design+Construction survey of AEC professionals reported that revenues had increased this year compared to 2012, with another 24.2% saying cash flow had stayed the same.

The majority (56.8%) of respondents—architects, engineers, contractors, building owners, and others in the commercial, industrial, multifamily, and institutional field—said their firms will bump up revenues next year, with 31.4% saying business will stay the same and only 11.8% predicting it will decline. A majority (55.5%) rated the health of their firms as good (35.6%) or very good (19.9%).

As has been the case in recent years, the overwhelming majority (71.2%) rated “general economic conditions (i.e., recession)” as the most important concern their firms will face in 2014.

Competition from other firms went up as a factor for the third year in a row, to 47.6% (44.9% in 2012, 40.1% in 2011). Nearly four in five respondents (79.3%) described the current business climate for their firms as “very” to “intensely” competitive; that’s up somewhat from 73.4% in 2012 and 74.8% in 2011. But “having insufficient capital funding for projects” declined slightly, to 24.1% of respondents, down from 29.7% in 2012 and 34.5% in 2011.

AEC respondents to this third annual survey of BD+C subscribers were still worried about the economy. On the other hand, “avoiding layoffs” (17.6%), “avoiding benefit reductions” (16.4%), and “keeping staff motivated” (14.6%) were of less concern.

DATA CENTERS CONTINUE THEIR SURGE INTO 2014

Asked to rate their firms’ prospects in specific construction sectors on a five-point scale from “excellent” to “very weak,” respondents gave data centers high marks. (Note: Respondents who checked “Not applicable/No opinion/Don’t know” are not counted here.) Among the findings:

• Data centers and mission-critical facilities continued to show strength, with the majority (56.0%) of respondents in the good/excellent category, compared to 52.1% last year and 45.2% the year before.

• Healthcare continued its leadership as the most highly desirable sector, with more than three in five respondents (62.5%) giving it a good to excellent rating, up from 58.8% last year.

• The apartment boom registered with AEC professionals, who gave multifamily housing a 56.1% good/excellent rating.

• Industrial/warehouse facilities keep moving up in the AEC psyche, registering a 33.0% interest level on the good/excellent scale, a significant climb from last year’s 25.5%.

• Retail commercial construction also showed vitality. Nearly a third of respondents (31.4%) came out on the good/excellent side for the coming year, well up from last year’s 19.9% rating.

• Nearly two-thirds of those surveyed (66.0%) said senior and assisted-living facilities look like good/excellent prospects for their firms, significantly up from last year’s healthy 50.5%. Hello, baby boomers!

• College and university facilities got the nod from 44.8% of respondents on the good to excellent scale, up from 37.8% last year.

As for government/military projects, the survey was taken before the full impact of the sequestration was known. The sector was rated good to excellent by 33.7% of respondents, much along the lines of last year’s 36.1% of respondents, down slightly from the previous year’s 41.1%.

While the construction of new office buildings drew tepid response (26.9%) in the good/excellent scale, that was still up significantly from last year’s 15.6% rating. However, a solid majority (52.1%) of respondents said office fitouts and interior renovations look good to excellent for 2014. That was likely a statistically significant leap from last year’s 35.7% who said office interiors would be a strong sector.

Respondents said their firms will likely use multiple strategies to stay ahead of the game in 2014. Only a small percentage (3.2%) said they think their companies will open a new office in the U.S. or Canada, while 4.5% said their firms might open an international office.

In fact, reconstruction, historic preservation, and renovations accounted for at least 25% of work for more than a third (38.5%) of respondents, up slightly from the 34.6% of respondents’ firms in 2012 and roughly the same as in 2011 (36.3%).

K-12 schools perked up a bit, with 30.9% saying the sector looks good to excellent for 2014, compared with 22.9% last year and 23.2% the year before.

TAKING ON THE DEMANDS OF BIM/VDC TECHNOLOGY

What about BIM? Is its promise holding true? Somewhat surprisingly, more than one in five respondents (22.7%) said their firms do not use building information modeling, about what was recorded over the previous two years.

Remarkably, precisely the same percentage of respondents (26.8%) said their firms used BIM in the majority of projects based on dollar value as in the last two annual surveys. Nearly two in five (39.8%) said their firms’ use of BIM will rise in the coming year; similarly, two-fifths (42.2%) of respondents said their companies will be investing more in technology in 2014.

As for social media, LinkedIn remained the top choice of respondents, at 53.1%, but that was a steep decline from last year’s 85.1% for LinkedIn. Facebook also took a hit, dropping to 32.5% in popularity, versus 49.5% last year, while Twitter dropped from 21.1% last year to 13.4%. Once again, a big chunk of respondents (31.3%) said they did not use social media channels.

Of the 400 who gave their professional description, 45.0% were architects; 8.0%, engineers; 28.8%, contractors; 9.8%, building owners, developers, or facility managers; and 8.6%, consultants or “other.” The margin of error was 4.8% at the 95% confidence level.

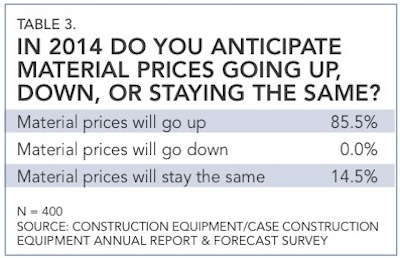

Respondents overwhelmingly said they expect prices of materials to rise in the coming year, with no respondents saying they expect such prices to fall.

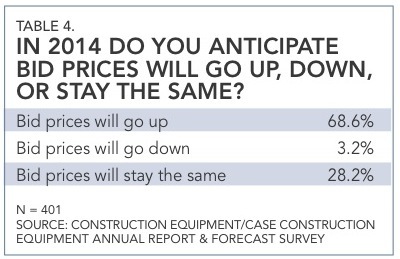

More than two-thirds of respondents (68.6%) said they expect bid prices to go up next year. Survey results have a margin of error of 4.8%.

For more on AEC firms' financial performance, see BD+C's 2013 Giants 300 Report.

Related Stories

Giants 400 | Feb 6, 2023

2022 Religious Sector Giants: Top architecture, engineering, and construction firms in the U.S. religious facility construction sector

HOK, Parkhill, KPFF, Shawmut Design and Construction, and Wiss, Janney, Elstner head BD+C's rankings of the nation's largest religious facility sector architecture, engineering, and construction firms, as reported in the 2022 Giants 400 Report.

Giants 400 | Feb 6, 2023

2022 Justice Facility Sector Giants: Top architecture, engineering, and construction firms in the U.S. justice facility/public safety sector

Stantec, DLR Group, Turner Construction, STO Building Group, AECOM, and Dewberry top BD+C's rankings of the nation's largest architecture, engineering, and construction firms for justice facility/public safety buildings work, including correctional facilities, fire stations, jails, police stations, and prisons, as reported in the 2022 Giants 400 Report.

Giants 400 | Feb 6, 2023

2022 Parking Structure Giants: Top architecture, engineering, and construction firms in the U.S. parking structure sector

Choate Parking Consultants, Walker Consultants, Kimley-Horn, PCL, and Balfour Beatty top BD+C's rankings of the nation's largest parking structure sector architecture, engineering, and construction firms, as reported in the 2022 Giants 400 Report.

Market Data | Feb 6, 2023

Nonresidential construction spending dips 0.5% in December 2022

National nonresidential construction spending decreased by 0.5% in December, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $943.5 billion for the month.

Giants 400 | Feb 3, 2023

Top Workplace/Interior Fitout Architecture, Engineering, and Construction Firms for 2022

Gensler, Interior Architects, AECOM, STO Building Group, and CBRE top the ranking of the nation's largest workplace/interior fitout architecture, engineering, and construction firms, as reported in Building Design+Construction's 2022 Giants 400 Report.

Multifamily Housing | Feb 3, 2023

HUD unveils report to help multifamily housing developers overcome barriers to offsite construction

The U.S. Department of Housing and Urban Development, in partnership with the National Institute of Building Sciences and MOD X, has released the Offsite Construction for Housing: Research Roadmap, a strategic report that presents the key knowledge gaps and research needs to overcome the barriers and challenges to offsite construction.

Steel Buildings | Feb 3, 2023

Top 10 structural steel building projects for 2023

A Mies van der Rohe-designed art and architecture school at Indiana University and Morphosis Architects' Orange County Museum of Art in Costa Mesa, Calif., are among 10 projects to win IDEAS² Awards from the American Institute of Steel Construction.

Multifamily Housing | Feb 2, 2023

St. Louis’s first transit-oriented multifamily development opens in historic Skinker DeBaliviere neighborhood

St. Louis’s first major transit-oriented, multi-family development recently opened with 287 apartments available for rent. The $71 million Expo at Forest Park project includes a network of pathways to accommodate many modes of transportation including ride share, the region’s Metro Transit system, a trolley line, pedestrian traffic, automobiles, and bike traffic on the 7-mile St. Vincent Greenway Trail.

Giants 400 | Feb 2, 2023

2022 Convention Center Sector Giants: Top architecture, engineering, and construction firms in the U.S. convention and conference facilities sector

Clark Group, EUA, KPFF, Populous, TVS, and Walter P Moore top BD+C's rankings of the nation's largest convention and conference facilities architecture, engineering, and construction firms, as reported in the 2022 Giants 400 Report.

Multifamily Housing | Feb 1, 2023

Step(1) housing: A new approach to sheltering unhoused people in Redwood City, Calif.

A novel solution to homelessness will open soon in Redwood City, Calif. The compact residential campus employs modular units to create individual sleeping units, most with private bathrooms. The 240 units of housing will be accompanied by shared services and community spaces. Instead of the congregate dorm-style shelters found in many U.S. cities, this approach gives each resident a private, lockable, conditioned sleeping space.