The healthcare industry has undergone a technology renaissance. What once encompassed patient scheduling and payment software has evolved into a myriad of applications and IoT devices (internet of things) that are often critical to the delivery of healthcare services. These changes to the healthcare industry have increased the need for IT infrastructure and data center capacity. However, despite the proliferation of technology in the healthcare sector, many healthcare companies aren’t providing the correct or adequate data center and IT infrastructure solutions to support their organizations’ growing technology needs. This article outlines the current data center landscape in the healthcare sector, industry trends, and challenges and opportunities new technologies present to the healthcare space.

Current Healthcare IT Landscape

From an IT perspective, the healthcare landscape is extremely complex and fluid. Consolidation and merger and acquisition (M&A) activity has caused organizations to inherit portfolios of often disparate or duplicative data center and IT assets. The typical combination of owned and leased data center assets are a mixed bag, often in the wrong location and inconsistent from a design and operation perspective. Consolidation and M&A events are the perfect catalyst for a reevaluation of data center and IT strategy. IT refresh periods should be used to rightsize data center portfolios and dispose underutilized and obsolescent data center capacity. However, it’s challenging to develop a strategy to conform to changing business, technology and regulatory environments.

As outsourcing in the healthcare industry becomes more prevalent, migration to third-party solutions seems to be a natural progression, allowing healthcare organizations to focus on their patients and alleviating the responsibilities and risks associated with owning a data center. As data center strategies become multi-faceted, IT and real estate decision-makers face the reality that their data center facilities may not be capable of accommodating cloud, virtualization and active-active architectures—all components of the evolving IT stack and often critical to a successful strategy. The trend toward third-party solutions has also enabled companies to hedge financial risks. Having the ability to scale data center footprints and IT technologies helps mitigate unnecessary spending and manages the risk of incorrect IT forecasting and capacity planning errors.

The complexity of matching data center strategies with evolving IT is exacerbated when options like cloud, managed services and virtualization are thrown into the equation. These options complicate the IT stack and contribute to a departure from traditional space and power discussions. By combining services beyond traditional power and space, the line between real estate and IT becomes blurred. This only adds to the difficulty of formulating a cohesive strategy since there is often a mismatch of IT needs and perceptions between real estate, IT and the procurement arms of an organization.

Industry Trends

Adapting to changing business and IT environments, healthcare companies are seeking flexible and scalable data center solutions to support emerging technologies. Often these requirements can’t be met in a single-owned data center facility and thus migrations to third-party solutions are taking place (i.e., colocation, cloud or other third-party environment). Besides the scalability benefits, healthcare companies are migrating to third-party solutions to support new and emerging technologies. Facility density, resiliency, location, connectivity, compliance certifications, hybrid IT services and other attributes play into the effective deployment and growth of these new technologies.

As healthcare organizations continue to look at reducing costs, data centers can prove to be a lucrative area for both short and long-term savings opportunities. With increasing healthcare real estate values, there’s often a financial benefit to repurposing traditional “on premise” data center space. This can also help mitigate occupancy constraints in existing healthcare facilities while providing more revenue-generating space. Migrating to third-party solutions also allows end users to take advantage of variable cost savings associated with different geographies, power, taxes, incentives, real estate, network and staffing. These variables are static in an owned data center scenario. Despite all of the benefits of migrating to a third-party solution, some organizations remain hesitant as they struggle with misconceptions around control of the data center, compliance and location.

With the shift toward third-party solutions, many legacy data center assets are becoming obsolete to organizations’ evolving IT strategies. Apart from obsolescence, other data center challenges healthcare organization face include:

● Underutilization

● Extensive capital expenditures

● Inefficient densities

● Security concerns

● Escalating operating costs

Although these assets may not be suitable for a healthcare entity to own and operate, many healthcare organizations are successfully offloading the liabilities of these data center assets and monetizing them in the form of Sale-Leaseback or Sale-Partial Leaseback transactions. This strategy can be ideal when looking to minimize Capex exposure, raise capital and remain in the same data center building without the perils of maintaining aging infrastructure. Even though investors’ appetites for data center assets are high, end users should be cautioned that not all legacy data centers are diamonds in the rough. Tenant credit rating, facility quality, lease terms and location all weigh heavily on the valuation. “If I have an opportunity to minimize my capital expenditures, that’s something I am going to look at,” said Daniel Morreale, CIO of Riverside Healthcare, in a recent Clear Data article. He also noted the growth of data storage requirements is on a steep curve, which will continue to rise with the growth of picture archiving and communication system (PACS) across cardiology and other non-radiological medical specialties.

Security & Compliance

Security concerns have been a catalyst for migrating to third-party solutions as Chief Information Officers (CIOs) and IT professionals begin to grasp the severity of security breaches. Data center and cloud providers have responded with offerings that address these concerns from a physical standpoint and virtual approach, rolling cybersecurity services into their offering.

Healthcare organizations are closely evaluating the criticality of applications and matching them with the appropriate tiering requirement support, a radical shift from the tradition Tier III and above data center solution. This shift in thinking has allowed healthcare organizations to realize the substantial savings that providers can offer through non-redundant (“N”) data center offerings, ideal for organizations that process large amounts of data for test and development, research, high-performance computing and non-mission-critical applications. As enterprises look to segment applications by criticality, the need for colocation, cloud and hybrid IT technologies becomes even more crucial.

Compliance issues like HIPAA (Health Insurance Portability and Accountability Act) continue to be a major burden and expensive effort for in-house data centers. In addition, the Affordable Care Act (ACA) has increased the number of patient records, driving growth in the data center. Multiply growth in the number of patients by the number of procedures, such as CAT scans or MRIs, and the effect on data becomes apparent. With doctors, nurses and technicians using mobile devices to check patients, data centers must be maintained to a zero fail rate and designed with enough flexibility to grow on demand.

IT Strategy

As companies develop and refine their IT strategies, discussions around traditional power and space are becoming less of a focus. Successful strategies begin by quantifying IT needs from a workload perspective and identifying the other applications necessary to complete the data center plan. By taking a more granular approach to understanding workloads and growth of the organization, IT and real estate leaders can more effectively align resources to ensure capital is being deployed and technology assets are being used to their fullest potential. A flexible and scalable data center strategy should also help mitigate unnecessary expenditures, reduce underutilized data center space and offer substantial cost savings.

While the approach for formulating a data center strategy is important, so is its life cycle. Effective strategies should be ahead by a minimum of 24 months and should address changes inside and outside of the healthcare organization. These extended lead times will help IT and real estate decision-makers review their data center portfolio and assess existing technologies. This will allow time to evaluate new technologies to implement across the organization.

For organizations with leased data center assets, it’s crucial to assess renewals and expiring leases more than two years in advance. On average, data center lease rates are 25% lower than they were three to five years ago, offering substantial savings. The benefit of renewals and renegotiating leases goes beyond rental rates as service level agreements (SLAs) may become more favorable to end users. These SLAs can be incredibly important to healthcare organizations as a majority of their data center applications are mission critical and don’t allow for downtime. Allowing a 24-month lead time gives IT teams the opportunity to develop and execute a migration strategy should the terms be favorable in other locations.

Since today’s data center strategies are made up of so many components, it’s important to open lines of communication across IT, real estate and procurement departments. Many organizations are plagued by self-sourced technology, business lines within procuring servers or applying for cloud subscriptions since the organization’s technology can’t move quickly enough. This is a textbook example as to why it’s difficult to calculate an organization’s true IT spend and footprint.

Conclusion

As technology continues to evolve and shape the healthcare industry, it’s critical that data center decision-makers understand the options available when creating their optimal data center strategy. While traditional power and space are still a cornerstone of data center strategies, the IT stack has grown in complexity; cloud, managed services and virtualization are now key components and allow organizations to mitigate traditional challenges of growth, forecasting and owning traditional IT and data center infrastructure.

IT and real estate leaders should also view the prevalence of consolidation and M&A activity as an opportunity for their organizations to refine and develop their data center strategy, taking time to quantify and optimize assets in their IT and real estate portfolios. With a better understanding of these portfolios, end users are increasingly migrating to third-party solutions as owning and operating data centers isn’t their core competency.

This move toward third-party solutions has allowed healthcare providers to realize the benefits of a flexible, secure and scalable environment for their IT hardware and applications. Although technology is fluid and constantly evolving, developing effective IT and data center strategies in the healthcare industry is becoming increasingly important. As the delivery of healthcare services and the success of healthcare organizations can often hinge on these factors, IT and real estate leaders need to be certain they’re making the right data center decisions for the future.

Related Stories

Digital Twin | May 24, 2021

Digital twin’s value propositions for the built environment, explained

Ernst & Young’s white paper makes its cases for the technology’s myriad benefits.

Healthcare Facilities | May 20, 2021

California Veteran Home, Skilled Nursing Facility and Memory Care project set for Yountville, Calif.

A team of Rudolph and Sletten and CannonDesign will design and build the facility.

Market Data | May 18, 2021

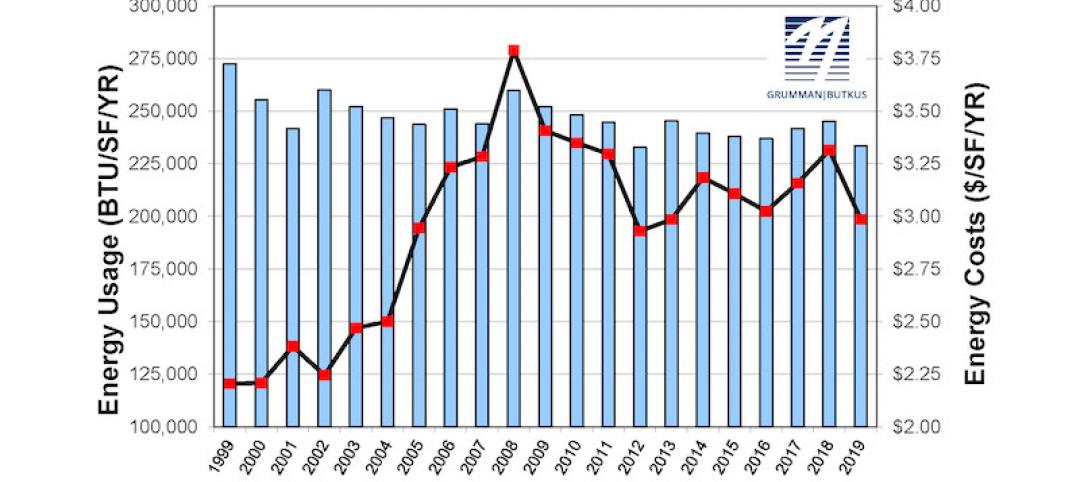

Grumman|Butkus Associates publishes 2020 edition of Hospital Benchmarking Survey

The report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Healthcare Facilities | May 12, 2021

New pet ER under construction in Vancouver, Wash.

The project will serve the Portland metro area 24 hours a day.

Healthcare Facilities | May 7, 2021

Private practice: Designing healthcare spaces that promote patient privacy

If a facility violates HIPAA rules, the penalty can be costly to both their reputation and wallet, with fines up to $250,000 depending on the severity.

Healthcare Facilities | May 5, 2021

HOK to design new Waterloo Eye Institute

The project is being designed for The University of Waterloo’s School of Optometry & Vision Science.

Healthcare Facilities | May 4, 2021

New proton therapy center will serve five-state region in Midwest

NCI-designated facility an addition to the University of Kansas Health System.

Healthcare Facilities | Apr 30, 2021

Registration and waiting: Weak points and an enduring strength

Changing how patients register and wait for appointments will enhance the healthcare industry’s ability to respond to crises.

Healthcare Facilities | Apr 29, 2021

HDR selected to design new Cancer Hospital in Shaoxing

Nature is at the heart of the project’s design.

Healthcare Facilities | Apr 16, 2021

UCI Medical Center Irvine to break ground in mid-2021

Hensel Phelps + CO Architects design-build team were awarded the project.