Industrial development continues to be a growth sector for many metros, especially in the western U.S. But aggressive building may be finally catching up with that sector’s demand, at least temporarily.

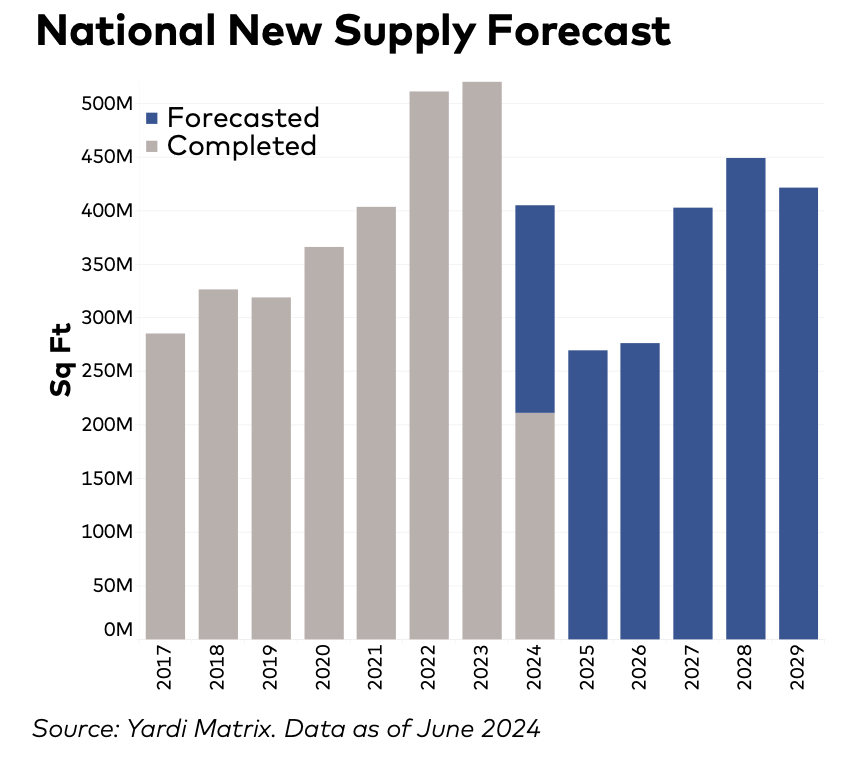

After two years of record-smashing deliveries, the industrial pipeline has slowed in a number of markets. In its latest National Industrial Report, CommercialEdge estimates that 97.8 million sf of industrial space were started in the first half of 2024, a 33% decline from the same period a year earlier. By comparison, 1.1 billion sf were started between 2021 and 2022, with 313 million sf started in the first half of 2022 alone. The latest slowdown in starts has been occurring for the past six quarters, says CommercialEdge, which attributes the erosion to “normalized” tenant demand, oversupply, rising construction costs, and “economic uncertainty.”

Nationwide, 375.7 million sf of industrial space were in various stages of construction through the first half of 2024, representing 1.9% of total stock. In the latest six-month period, 209 million sf of new space were delivered, compared to 160 million sf in the first half of 2022. “This growth underscores the market’s capacity to bring projects to completion despite the decline in construction starts,” CommercialEdge states.

This sector has gotten a big bump from manufacturing, which accounted for 16.1% of annualized industrial construction starts through June, compared to an estimated 7.5% in 2018 through 2021, and more than 13% in 2022 and 2023. As more manufacturing returns to the U.S., demand for industrial space is expected to benefit.

Indeed, CommercialEdge forecasts that the new development pipeline will grow in the next few years, but at a slower clip. It points out that developers have disclosed plans for 561.2 million sf of new space. “Once the market absorbs the recently completed stock, and the cost of capital begins to decrease, we expect many of these projects to see shovels in the ground,” predicts CommercialEdge.

Vacancy rates and rents for industrial space rising

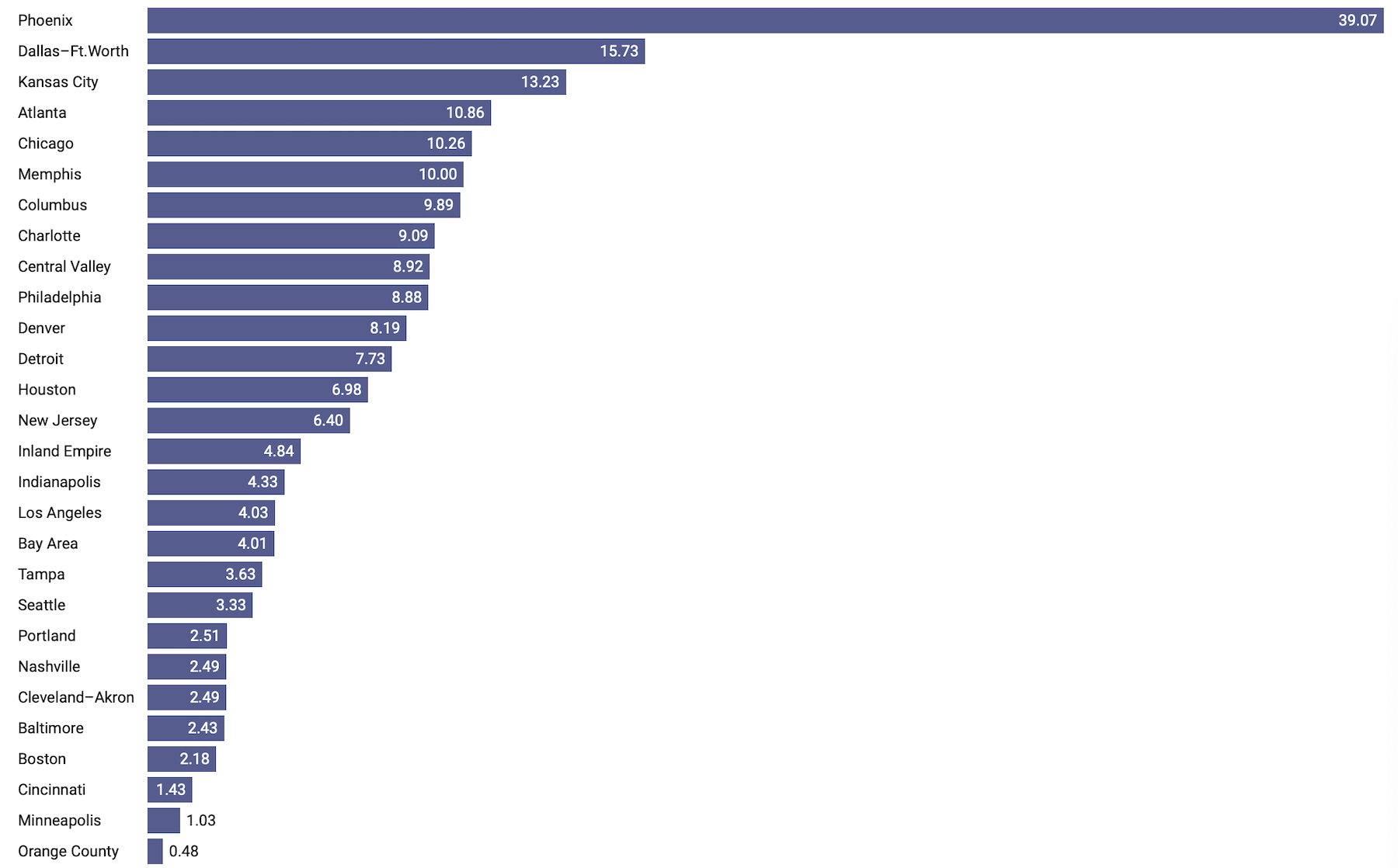

Phoenix leads the country by far in new industrial space, with 39.07 million sf under construction. The next-closest metro was Dallas-Fort Worth, at 15.23 million sf. DFW’s vacancy rate sat at a relatively manageable 6.5%, but it appears this market is “hitting the brakes” on new development after delivering 126.4 million sf of industrial space since the start of 2022.

Nationally, the vacancy rate for industrial space stood at 6.1%, up slightly. The national average rent in June was $8.04 per sf, although the average for contracts signed over the previous 12 months was $10.56. The San Francisco Bay Area recorded the highest average rent, at $13.34, and $16.24 per sf for newer contracts. Miami experienced the largest premium for new leases that, at $17.35, cost tenants $5.85 more than the national average.

California’s Inland Empire led the nation in rent growth, with in-place rents rising 12.5% year-over-year. Conversely, the Midwest saw the slowest rent growth: In Kansas City, for example, in-place rents increased only 2.5%; in St. Louis, 3.4%.

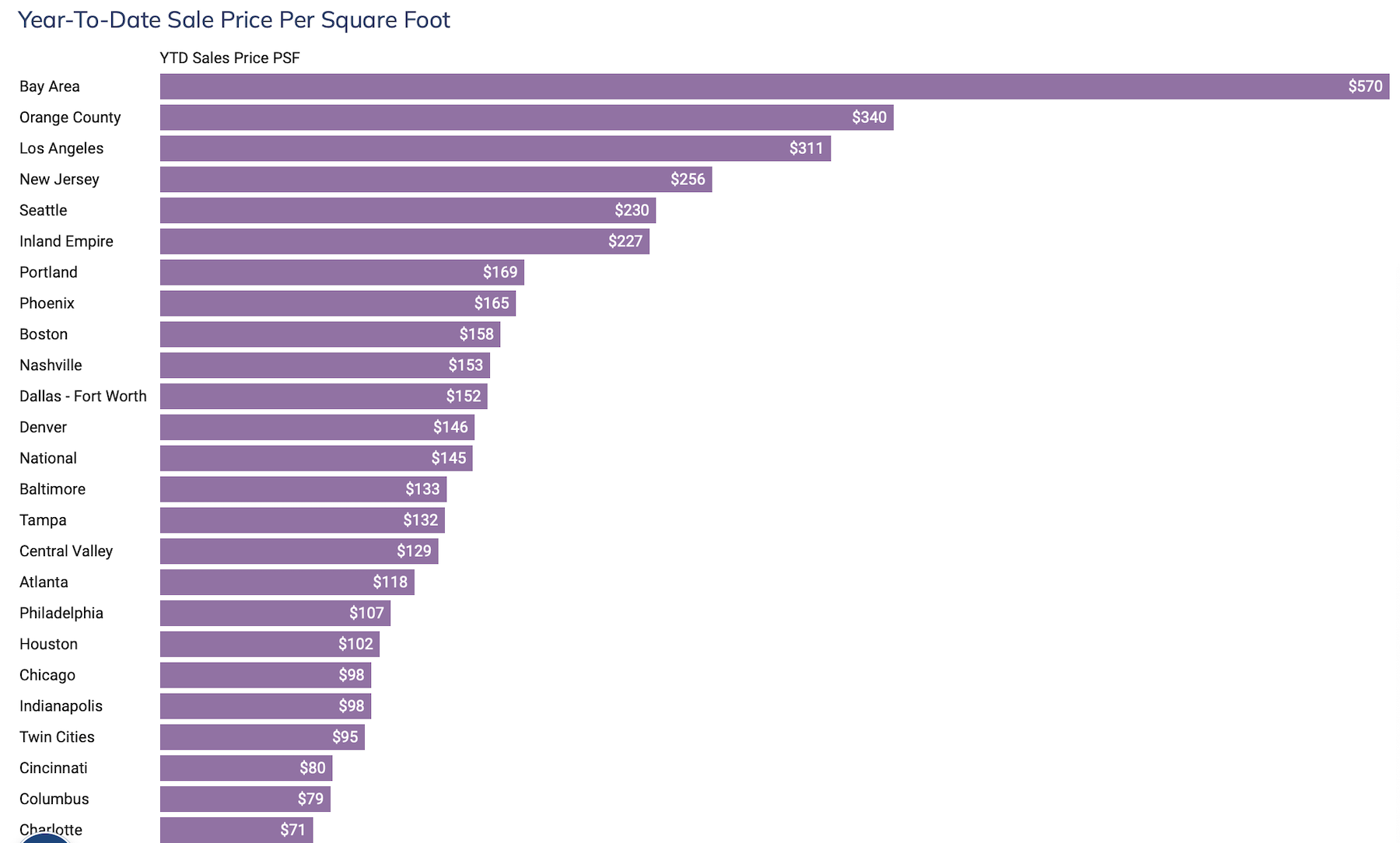

Bay Area leads industrial sales

The sale of industrial buildings totaled $25.1 billion through the first half of 2024, and demand remains strong, with the average sale price of $139 per sf rising 12.9% over the same period in 2023, according to CommercialEdge estimates.

Again, the Bay Area led all markets in year-to-date industrial sales, at $2.285 billion. San Francisco was followed by Dallas-Fort Worth ($2.006 billion), Los Angeles ($1.581 billion, and Chicago ($1.314 billion).

Southern California remains the most sought-after location for distribution center and warehouse sales and development. CommercialEdge notes that earlier this year Rexford Industrial Realty paid $1 billion for 3 million sf across 48 properties in L.A. and Orange counties.

The Bay Area led the nation in average sales price per sf, at $570. This market has seen a spike in demand for advanced manufacturing space. Over 4 million sf of industrial space are under construction in the Bay Area.

In the South, the surge in Texas’s population—it’s the fastest-growing state in the U.S.—drove demand for industrial space, with DFW serving as a hub from products arriving from Mexico, which recently surpassed Canada as America’s largest trading partner, according to the Census Bureau. That positioning is why CommercialEdge expects Dallas-Fort Worth’s industrial development and construction to eventually pick up steam again.

Other markets worth keeping an eye on include Charlotte and Nashville, with their low vacancy rates and tight supply.

On the other hand, Boston—one of the country’s most expensive markets—reported the highest industrial vacancy rate, at 8.8%. New Jersey, another pricy rent market, nevertheless remained a regional leader in industrial sales, with over $1 billion in transactions closing through June.

Related Stories

| Jul 28, 2014

Reconstruction Sector Construction Firms [2014 Giants 300 Report]

Structure Tone, Turner, and Gilbane top Building Design+Construction's 2014 ranking of the largest reconstruction contractor and construction management firms in the U.S.

| Jul 28, 2014

Reconstruction Sector Engineering Firms [2014 Giants 300 Report]

Jacobs, URS, and Wiss, Janney, Elstner top Building Design+Construction's 2014 ranking of the largest reconstruction engineering and engineering/architecture firms in the U.S.

| Jul 28, 2014

Reconstruction Sector Architecture Firms [2014 Giants 300 Report]

Stantec, HDR, and HOK top Building Design+Construction's 2014 ranking of the largest reconstruction architecture and architecture/engineering firms in the U.S.

| Jul 27, 2014

Maturing ‘plug and play’ sector could take market share from AEC Giants [2014 Giants 300 Report]

The growth of modular and containerized data center solutions may eventually hinder the growth of traditional data center construction services.

| Jul 27, 2014

Top Data Center Construction Firms [2014 Giants 300 Report]

Holder, Turner, and DPR head Building Design+Construction's 2014 ranking of the largest data center contractors and construction management firms in the U.S.

| Jul 27, 2014

Top Data Center Engineering Firms [2014 Giants 300 Report]

Fluor, Jacobs, and Syska Hennessy top Building Design+Construction's 2014 ranking of the largest data center engineering and engineering/architecture firms in the U.S.

| Jul 27, 2014

Top Data Center Architecture Firms [2014 Giants 300 Report]

Gensler, Corgan, and HDR head Building Design+Construction's 2014 ranking of the largest data center architecture and architecture/engineering firms in the U.S.

| Jul 23, 2014

Architecture Billings Index up nearly a point in June

AIA reported the June ABI score was 53.5, up from a mark of 52.6 in May.

| Jul 21, 2014

Economists ponder uneven recovery, weigh benefits of big infrastructure [2014 Giants 300 Report]

According to expert forecasters, multifamily projects, the Panama Canal expansion, and the petroleum industry’s “shale gale” could be saving graces for commercial AEC firms seeking growth opportunities in an economy that’s provided its share of recent disappointments.

| Jul 18, 2014

Contractors warm up to new technologies, invent new management schemes [2014 Giants 300 Report]

“UAV.” “LATISTA.” “CMST.” If BD+C Giants 300 contractors have anything to say about it, these new terms may someday be as well known as “BIM” or “LEED.” Here’s a sampling of what Giant GCs and CMs are doing by way of technological and managerial innovation.