The impact of large, transformational deals by integrated engineers and constructors (E&C) last year will spur continued M&A activity this year, as the largest firms use acquisitions to drive growth and enter new markets, according to the latest edition of FMI’s Mergers & Acquisitions Trends.

“Large, transformational deals highlighted robust M&A activity in the E&C industry in 2014,” said Chris Daum, Senior Managing Director and Head of Investment Banking at FMI. “While there may not be as many marquee transactions thus far in 2015, M&A activity remains very high, particularly among the largest U.S. and international firms that continue to pursue acquisitions as a conduit for growth and margin expansion.”

Large, integrated E&C firms remain acquisitive in 2015 as they look to expand beyond their current maturing markets. Competition among buyers for quality firms of size in attractive growth markets is leading to favorable valuations for sellers. One material challenge that exists for buyers has been the limited number of willing sellers that are of sufficient size to be attractive—e.g., heavy civil contracting firms above $200 million and utility T&D or multi-trade industrial firms above $100 million in value.

Persistent themes in 2015

Persistent themes are shaping broader trends within the industry:

• 2014 was notable for several “mega-deals” in the E&C industry, with three deals accounting for more than $11 billion in transaction value alone. Several multibillion-dollar transactions, including AECOM’s acquisition of URS, SNC-Lavalin’s acquisition of Kentz and the merger of AMEC and Foster Wheeler, reflected the continuing convergence of engineering and construction, the pursuit of global scale by large firms and competition for “mega-projects,” which continue to proliferate.

• Firms tied to public spending remain in a “holding pattern” until spending returns to normalized levels. Most of the new construction currently taking place is in the private sector due to a lack of public spending on infrastructure, and buyers have shifted their appetites toward companies servicing the more active private sectors. Potential sellers who are heavily tied to the public sector may attract limited buyer interest until the outlook for public infrastructure spending improves.

• Interest from strategic buyers exceeds the number of quality, motivated sellers in several industry sectors, driven in part by strong interest from international buyers. The US is the most attractive growth market for international firms faced with flat or declining business in their home markets. International buyers are most interested in national or large regional general contractors, heavy civil contractors, or large specialty firms focused on power, energy and industrial infrastructure.

Varied activity by sector

The carryover of robust M&A activity from 2014 in the E&C industry is most notable among firms involved in the design, construction or maintenance of power, energy, utility and industrial infrastructure. However, building products, energy services and cleantech and specialty contractors with large service and maintenance operations continue to see increased buyer interest.

In Oil & Gas, many private equity firms pulled back from pending upstream and midstream deals in the second half of 2014. The sustained decline in the price of oil is expected to fuel an increase in distressed sales, a decline in valuation multiples and a re-emergence of strategic buyers in 2015. Those financial buyers who remain active in the market are focused on acquiring quality assets at steep discounts. The industrial sector, meanwhile, is growing faster than the overall construction market. For that reason, we expect M&A activity for industrial trade contractors to increase over the next few years. The surge in industrial projects is due to the recent availability of low natural gas prices. This has driven both new and renovation projects, spurring some contractors to look to M&A as a potential solution.

Robust international activity

Many international buyers, meanwhile, who have historically focused on traditional construction firms, are beginning to shift their attention to integrated E&C firms. Many buyers believe the integrated model provides a significant entry point into the U.S. market for firms looking to make their initial acquisition. In addition, international buyers continue to see the U.S. as an opportunity for Public-Private Partnerships (P3) projects, and an integrated platform can provide earlier access to the development of revenue-generating projects.

“While 2015 may not match the level of activity seen in 2014, M&A remains a focal point of strategy for many large domestic E&C firms,” said Daum. “Coupling that with the increased interest from international buyers should allow for a continued robust M&A market in 2015.”

FMI’s Mergers & Acquisitions Trends report can be accessed here.

Related Stories

| Feb 7, 2014

DOE, Autodesk team to overhaul the EnergyPlus simulation program

The update will allow a larger ecosystem of developers to contribute updates to the code in order to improve performance and decrease the time required to run energy model simulations.

| Feb 7, 2014

Bernards announces executive leadership realignment

Changes reflect long-term growth plans as builder enters its fifth decade.

| Feb 7, 2014

Zaha Hadid's 'white crystal' petroleum research center taking shape in the desert [slideshow]

Like a crystalline form still in the state of expansion, the King Abdullah Petroleum Studies and Research Center will rise from the desert in dramatic fashion, with a network of bright-white, six-sided cells combining to form an angular, shell-like façade.

| Feb 6, 2014

End of the open workplace?

If you’ve been following news about workplace design in the popular media, you might believe that the open workplace has run its course. While there’s no shortage of bad open-plan workplaces, there are two big flaws with the now common claim that openness is bad.

| Feb 6, 2014

New Hampshire metal building awes visitors

Visitors to the Keene Family YMCA in New Hampshire are often surprised by what they encounter. Liz Coppola calls it the “wow factor.” “Literally, there’s jaw dropping,” says Coppola, director of financial and program development for the Keene Family YMCA.

| Feb 5, 2014

M&A activity down in 2013 among architecture, engineering firms: Report

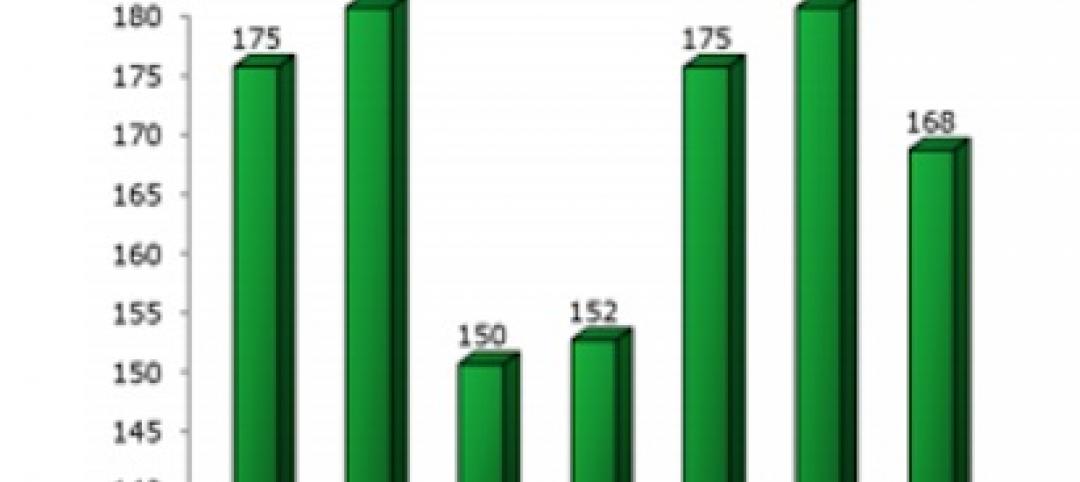

In 2013, consultant Morrissey Goodale observed 168 sales of U.S.-based architecture and engineering (“A/E”) firms – down nearly 7% from the record 180 sales of U.S.-based A/E firms in 2012.

| Feb 5, 2014

BIA Opens Entries for 25th Annual Brick in Architecture Awards

Entries open on February 10 for the Brick Industry Association's (BIA) Brick in Architecture Awards. Celebrating its silver anniversary, BIA's annual honors spotlight outstanding, innovative and sustainable architecture that incorporates clay brick products as the predominant exterior building or paving material.

| Feb 5, 2014

Multifamily Housing, Green Building, Market Trends, Innovation to be Prime Topics at MBI’s World of Modular

More than 600 developers, contractors, architects, builders, dealers and equipment/service suppliers are expected at the event, slated for March 21-24 in San Antonio, Texas, and hosted by the Modular Building Institute.

| Feb 5, 2014

7 towers that define the 'skinny skyscraper' boom [slideshow]

Recent advancements in structural design, combined with the loosening of density and zoning requirements, has opened the door for the so-called "superslim skyscraper."

| Feb 4, 2014

World's fifth 'living building' certified at Smith College [slideshow]

The Bechtel Environmental Classroom utilizes solar power, composting toilets, and an energy recovery system, among other sustainable strategies, to meet the rigorous performance requirements of the Living Building Challenge.