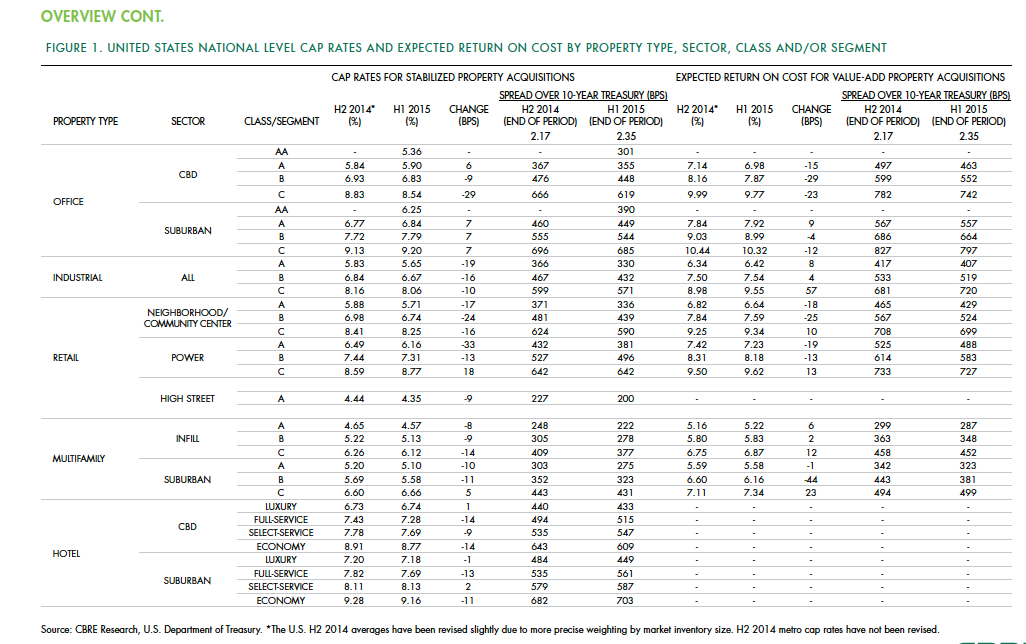

Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

| Jun 5, 2013

USGBC: Free LEED certification for projects in new markets

In an effort to accelerate sustainable development around the world, the U.S. Green Building Council is offering free LEED certification to the first projects to certify in the 112 countries where LEED has yet to take root.

| Jun 4, 2013

SOM research project examines viability of timber-framed skyscraper

In a report released today, Skidmore, Owings & Merrill discussed the results of the Timber Tower Research Project: an examination of whether a viable 400-ft, 42-story building could be created with timber framing. The structural type could reduce the carbon footprint of tall buildings by up to 75%.

| Jun 3, 2013

Construction spending inches upward in April

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during April 2013 was estimated at a seasonally adjusted annual rate of $860.8 billion, 0.4 percent above the revised March estimate of $857.7 billion.

| Jun 3, 2013

Trifecta of awards recognize Vision/Rubenstein campus, Bayer Healthcare HQ

When Vision Equities, LLC and Rubenstein Partners purchased the 200-acre former Alcatel-Lucent campus in Whippany a little more than two years ago, the partnership recognized the property’s potential to serve as a benchmark infill revitalization for the State of New Jersey.

| May 31, 2013

Nation's first retrofitted zero-energy building opens in California

The new training facility for IBEW/NECA is the first commercial building retrofit designed to meet the U.S. Department of Energy’s requirements for a net-zero energy building.

| May 29, 2013

Realtors report positive trends in commercial real estate market

Realtors who practice commercial real estate have reported an increase in annual gross income for the third year in a row, signaling the market is on the road to recovery.

| May 24, 2013

First look: Revised plan for Amazon's Seattle HQ and 'biodome'

NBBJ has released renderings of a revised plan for Amazon's new three-block headquarters in Seattle. The proposal would replace a previously approved six-story office building with a three-unit "biodome."

| May 20, 2013

Jones Lang LaSalle: All U.S. real estate sectors to post gains in 2013—even retail

With healthier job growth numbers and construction volumes at near-historic lows, real estate experts at Jones Lang LaSalle see a rosy year for U.S. commercial construction.

| May 3, 2013

'LEED for all GSA buildings,' says GSA Green Building Advisory Committee

The Green Building Advisory Committee established by the General Services Administration, officially recommended to GSA that the LEED green building certification system be used for all GSA buildings as the best measure of building efficiency.

| May 2, 2013

A snapshot of the world's amazing construction feats (in one flashy infographic)

From the Great Pyramids of Giza to the U.S. Interstate Highway System, this infographic outlines interesting facts about some of the world's most notable construction projects.