Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

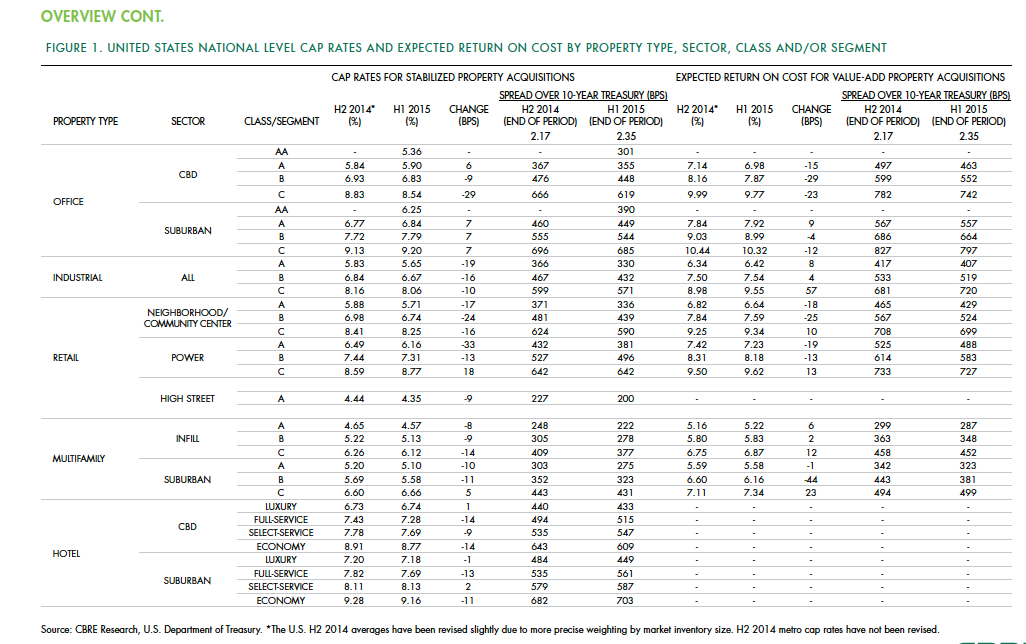

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

| Oct 13, 2010

HQ renovations aim for modern look

Gerner Kronick + Valcarcel Architects’ renovations to the Commonwealth Bank of Australia’s New York City headquarters will feature a reworked reception lobby with back-painted glass, silk-screened logos, and a video wall.

| Oct 13, 2010

County building aims for the sun, shade

The 187,032-sf East County Hall of Justice in Dublin, Calif., will be oriented to take advantage of daylighting, with exterior sunshades preventing unwanted heat gain and glare. The building is targeting LEED Silver. Strong horizontal massing helps both buildings better match their low-rise and residential neighbors.

| Oct 12, 2010

Guardian Building, Detroit, Mich.

27th Annual Reconstruction Awards—Special Recognition. The relocation and consolidation of hundreds of employees from seven departments of Wayne County, Mich., into the historic Guardian Building in downtown Detroit is a refreshing tale of smart government planning and clever financial management that will benefit taxpayers in the economically distressed region for years to come.

| Oct 12, 2010

The Watch Factory, Waltham, Mass.

27th Annual Reconstruction Awards — Gold Award. When the Boston Watch Company opened its factory in 1854 on the banks of the Charles River in Waltham, Mass., the area was far enough away from the dust, dirt, and grime of Boston to safely assemble delicate watch parts.

| Oct 12, 2010

Building 13 Naval Station, Great Lakes, Ill.

27th Annual Reconstruction Awards—Gold Award. Designed by Chicago architect Jarvis Hunt and constructed in 1903, Building 13 is one of 39 structures within the Great Lakes Historic District at Naval Station Great Lakes, Ill.

| Oct 12, 2010

From ‘Plain Box’ to Community Asset

The Mid-Ohio Foodbank helps provide 55,000 meals a day to the hungry. Who would guess that it was once a nondescript mattress factory?

| Oct 11, 2010

HGA wins 25-Year Award from AIA Minnesota

HGA Architects and Engineers won a 25-Year Award from AIA Minnesota for the Willow Lake Laboratory.

| Oct 8, 2010

Union Bank’S San Diego HQ awarded LEED Gold

Union Bank’s San Diego headquarters building located at 530 B Street has been awarded LEED Gold certification from the Green Building Certification Institute under the standards established by the U.S. Green Building Council. Gold status was awarded to six buildings across the United States in the most recent certification and Union Bank’s San Diego headquarters building is one of only two in California.

| Oct 6, 2010

Windows Keep Green Goals in View

The DOE's National Renewable Energy Laboratory has almost 600 window openings, and yet it's targeting LEED Platinum, net-zero energy use, and 50% improvement over ASHRAE 90.1. How the window ‘problem’ is part of the solution.

| Sep 21, 2010

New BOMA-Kingsley Report Shows Compression in Utilities and Total Operating Expenses

A new report from the Building Owners and Managers Association (BOMA) International and Kingsley Associates shows that property professionals are trimming building operating expenses to stay competitive in today’s challenging marketplace. The report, which analyzes data from BOMA International’s 2010 Experience Exchange Report® (EER), revealed a $0.09 (1.1 percent) decrease in total operating expenses for U.S. private-sector buildings during 2009.