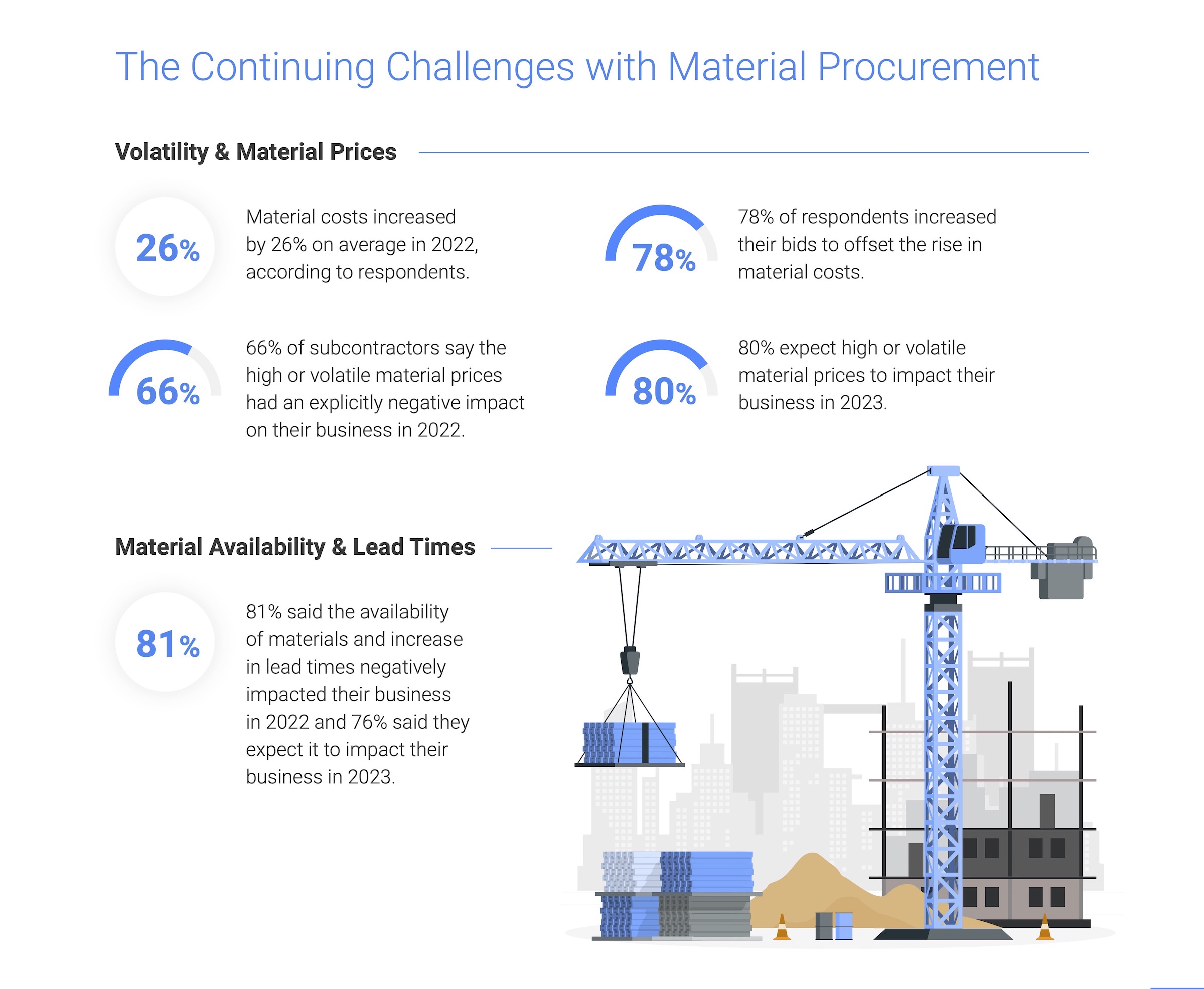

Financing solutions provider Billd recently surveyed nearly 900 commercial construction professionals across the U.S. for its 2023 National Subcontractor Market Report. Its key finding: rising input prices for materials and labor cost subcontractors $97 billion in unplanned expenses last year.

Rising material costs and price volatility are not new issues for subcontractors, with 81% of those surveyed reporting a negative effect on their businesses in 2022; 80% expect that trend to continue. It is no surprise given material costs jumped a staggering 26%, according to respondents. Similarly, competition for labor due to the longtime labor shortage was validated by a 15% average increase in labor cost. Together, those increases amounted to $97 billion in additional expenses for the subcontractor. While some subcontractors increased their bids to offset these rapidly rising costs, one third of respondents were unable to raise those bids commensurate with their expenses. This resulted in 57% of businesses reporting a decrease in profitability, despite 61% reporting revenue growth.

"Subcontractors are the foundation of the construction industry, providing all material and labor to complete a project," said Chris Doyle, CEO of Billd. "They purchase that material and pay for that labor upfront, not being paid for their work for 74 days, a result of the dysfunctional payment cycle. If you add unplanned expenses due to rising costs in material and labor, it puts an unrealistic burden on subcontractors to provide that foundation."

The report examines how macroeconomic conditions from this and prior years impacted subcontractors in 2022, as well as their outlook for 2023. It also creates hope by providing perspective on new financing options subcontractors can leverage as mainstays – like supplier terms – become less reliable. 72% of respondents report having supplier terms of 30 days or less. Compared to a 74-day average wait time for payment, it is no surprise that 51% deem the length of their terms insufficient.

Supplier terms also have an unforeseen cost; most suppliers (also surveyed) state that they offer discounts for upfront payment. Despite those disadvantages, 87% of respondents still rely on supplier terms as their predominant means of buying materials. When it comes to funding their increasing labor costs, traditional financing options are even less accessible, leaving 87% of respondents coming out of pocket for labor before getting paid themselves. Luckily, the report highlights financial relief for labor as well as materials.

Related Stories

| Dec 17, 2010

5 Tips on Building with SIPs

Structural insulated panels are gaining the attention of Building Teams interested in achieving high-performance building envelopes in commercial, industrial, and institutional projects.

| Dec 17, 2010

How to Win More University Projects

University architects representing four prominent institutions of higher learning tell how your firm can get the inside track on major projects.

| Dec 13, 2010

Energy efficiency No. 1 priority for commercial office tenants

Green building initiatives are a key influencer when tenants decide to sign a commercial real estate lease, according to a survey by GE Capital Real Estate. The survey, which was conducted over the past year and included more than 2,220 office tenants in the U.S., Canada, France, Germany, Sweden, the UK, Spain, and Japan, shows that energy efficiency remains the No. 1 priority in most countries. Also ranking near the top: waste reduction programs and indoor air.

| Dec 7, 2010

Are green building RFPs more important than contracts?

The Request for Proposal (RFP) process is key to managing a successful LEED project, according to Green Building Law Update. While most people think a contract is the key element to a successful construction project, successfully managing a LEED project requires a clear RFP that addresses many of the problems that can lead to litigation.

| Dec 7, 2010

Blue is the future of green design

Blue design creates places that are not just neutral, but actually add back to the world and is the future of sustainable design and architecture, according to an interview with Paul Eagle, managing director of Perkins+Will, New York; and Janice Barnes, principal at the firm and global discipline leader for planning and strategies.

| Dec 7, 2010

Green building thrives in shaky economy

Green building’s momentum hasn’t been stopped by the economic recession and will keep speeding through the recovery, while at the same time building owners are looking to go green more for economic reasons than environmental ones. Green building has grown 50% in the past two years; total construction starts have shrunk 26% over the same time period, according to “Green Outlook 2011” report. The green-building sector is expected to nearly triple by 2015, representing as much as $145 billion in new construction activity.

| Dec 7, 2010

USGBC: Wood-certification benchmarks fail to pass

The proposed Forest Certification Benchmark to determine when wood-certification groups would have their certification qualify for points in the LEED rating systemdid not pass the USGBC member ballot. As a result, the Certified Wood credit in LEED will remain as it is currently written. To date, only wood certified by the Forest Stewardship Council qualifies for a point in the LEED, while other organizations, such as the Sustainable Forestry Initiative, the Canadian Standards Association, and the American Tree Farm System, are excluded.

| Dec 7, 2010

AGC of A Survey: 2011 Construction Industry Hiring and Business Outlook

The Associated General Contractors of America wants to know about your construction company’s business outlook for 2011. Help out the Association by answering a few quick questions in their 2011 Construction Industry Hiring and Business Outlook survey.

| Dec 7, 2010

Prospects for multifamily sector improve greatly

The multifamily sector is showing signs of a real recovery, with nearly 22,000 new apartment units delivered to the market. Net absorption in the third quarter surged by 94,000 units, dropping the national vacancy rate from 7.8% to 7.1%, one of the largest quarterly drops on record, and rents increased for the second quarter in a row.