Though news reports and predictions painted a gloomy picture, the U.S. economy actually ended 2013 with a record setting year on Wall Street. The Dow Jones Industrial Average finished up 26.5%, its best return since 1995, and the S&P up nearly 30%, shattering previous records.

(See past articles from CBRE Healthcare)

Momentum continues to build in the housing market with positive trends in pricing, new housing starts, and inventory volume across the country. The U.S. economy added 74,000 jobs in December, as the unemployment rate fell to 6.7%, according to the Bureau of Labor Statistics.

With an improving economy and an unprecedented stimulus from the Federal Reserve continuing through 2014, the macro-economic outlook is good.

Healthcare Reform

Meanwhile, the healthcare industry has been rapidly evolving under the Affordable Care Act (ACA). Healthcare reform has compelled health systems, hospitals and physician groups to rein in sky-high costs while improving the quality of care, often coping with more regulatory requirements and less money.

Changes to reimbursement methods and reductions in healthcare provider compensation combined with an increased demand for healthcare services over the next five years, from an estimated 79 million aging baby boomers and 30 million newly insured patients, is forcing health systems to rethink their approach to balance sheet assets and liabilities, including health care real estate.

As health systems and physician groups change their delivery network, both healthcare service operators and owners of healthcare real estate are repositioning their portfolio requirements based on their growth needs. This has led to the highest medical office sales volume in the healthcare capital markets since 2007.

Healthcare reform incentives are driving consolidation of services in the industry, which has produced a robust mergers and acquisitions environment. As hospitals and healthcare organizations face mounting competitive, regulatory and financial challenges, leadership is seeking ways to capitalize on the increase of privately insured patients and Medicaid expansion while effectively serving the interests of their communities.

Healthcare operators need to diversify and expand their patient base while also becoming more efficient and leaner. This is most effectively achieved through greater economies of scale by merging with other health systems, hospitals, and physician groups, leading to a consolidation in the industry.

Consolidation is taking on two forms that are impacting real estate. First, is a unification of real estate assets as a result of health system mergers and physician employment, which has caused a consolidation of physician practices into fewer facilities that are strategically dispersed throughout the community. The other is consolidation among the hospitals and health systems seeking to concentrate operations in a single Metropolitan Statistical Area (MSA), region or state.

Off-Campus Healthcare

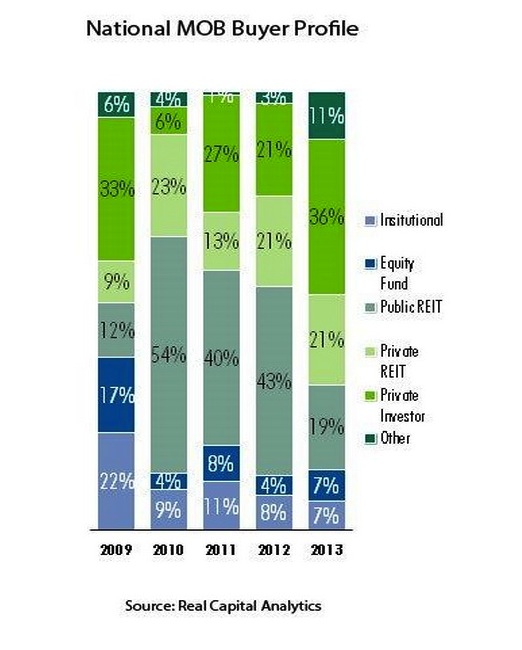

Healthcare investors are monitoring the consolidation trends and strategically aligning themselves through real estate transactions with market dominant hospitals and health systems, specifically those with investment grade credit ratings. Historically, investment in medical office properties revealed an institutional and REIT investor preference for core on-campus properties only.

However, over the past 12-18 months, we have witnessed little difference between core on-campus and core off-campus medical office buildings with meaningful hospital tenancy. This is a direct result of the health system shift to high quality healthcare delivered in outpatient facilities further away from traditional acute-care hospital campuses.

The care delivery network is moving from the busy, compact hospital campuses to off-campus outpatient settings with convenient access where patients live, work and shop. In response to healthcare providers commitment to off-campus destinations located near traditional retail properties and close to residential neighborhoods, investors have modified their investment criteria with a focus on off-campus properties.

The buyer pool for healthcare real estate has steadily increased over the last couple of years as investors continue to realize the inherent stability and higher returns for medical properties when compared to the more competitive multi-family, office, retail, and industrial real estate markets.

Public healthcare REITs have historically dominated the medical office investment market share, but in 2013 the private healthcare REITs and private capital investors took over the top slots. Listed and non-listed U.S. equity REITs (including both Public and Private) raised a total of $76.96 billion of equity and debt in 2013, an amount that surpassed 2012’s prior record of $73.33 billion, according to the National Association of Real Estate Investment Trusts (NAREIT). Nearly $9.3 billion, or roughly 12% was attributed to the Healthcare sector.

Conclusion

We anticipate another active year in healthcare capital markets for 2014. All investors will have stable access to capital and interest rates will likely remain at historic lows.

The favorable macro-economic outlook and consolidation among healthcare providers and continuous modification of the healthcare delivery model will continue to fuel the investment engine for what could be another record year in medical office sales.

About the authors

Lee Asher (Lee.Asher@cbre.com) and Chris Bodnar (Chris.Bodnar@cbre.com) are both Senior Vice Presidents with CBRE Healthcare Capital Markets Group. For more on CBRE Healthcare, visit www.cbre.com/healthcare.

Related Stories

Student Housing | Feb 19, 2024

UC Law San Francisco’s newest building provides student housing at below-market rental rates

Located in San Francisco’s Tenderloin and Civic Center neighborhoods, UC Law SF’s newest building helps address the city’s housing crisis by providing student housing at below-market rental rates. The $282 million, 365,000-sf facility at 198 McAllister Street enables students to live on campus while also helping to regenerate the neighborhood.

MFPRO+ News | Feb 15, 2024

UL Solutions launches indoor environmental quality verification designation for building construction projects

UL Solutions recently launched UL Verified Healthy Building Mark for New Construction, an indoor environmental quality verification designation for building construction projects.

MFPRO+ News | Feb 15, 2024

Nine states pledge to transition to heat pumps for residential HVAC and water heating

Nine states have signed a joint agreement to accelerate the transition to residential building electrification by significantly expanding heat pump sales to meet heating, cooling, and water heating demand. The Memorandum of Understanding was signed by directors of environmental agencies from California, Colorado, Maine, Maryland, Massachusetts, New Jersey, New York, Oregon, and Rhode Island.

MFPRO+ News | Feb 15, 2024

Oregon, California, Maine among states enacting policies to spur construction of missing middle housing

Although the number of new apartment building units recently reached the highest point in nearly 50 years, construction of duplexes, triplexes, and other buildings of from two to nine units made up just 1% of new housing units built in 2022. A few states have recently enacted new laws to spur more construction of these missing middle housing options.

Green | Feb 15, 2024

FEMA issues guidance on funding for net zero buildings

The Federal Emergency Management Agency (FEMA) recently unveiled new guidance on additional assistance funding for net zero buildings. The funding is available for implementing net-zero energy projects with a tie to disaster recovery or mitigation.

Hospital Design Trends | Feb 14, 2024

Plans for a massive research hospital in Dallas anticipates need for child healthcare

Children’s Health and the UT Southwestern Medical Center have unveiled their plans for a new $5 billion pediatric health campus and research hospital on more than 33 acres within Dallas’ Southwestern Medical District.

Architects | Feb 13, 2024

Pierluca Maffey joins Carrier Johnson + Culture as new Firmwide Head of Design

Carrier Johnson + Culture (CJ+C) has hired Pierluca “Luca” Maffey, International Assoc. AIA, as the firm's new Firmwide Head of Design and Design Principal.

K-12 Schools | Feb 13, 2024

K-12 school design trends for 2024: health, wellness, net zero energy

K-12 school sector experts are seeing “healthiness” for schools expand beyond air quality or the ease of cleaning interior surfaces. In this post-Covid era, “healthy” and “wellness” are intersecting expectations that, for many school districts, encompass the physical and mental wellbeing of students and teachers, greater access to outdoor spaces for play and learning, and the school’s connection to its community as a hub and resource.

Office Buildings | Feb 13, 2024

Creating thoughtful tech workplace design

It’s important for office design to be inspiring, but there are some practical principles that can be incorporated into the design of real-world tech workplaces to ensure they convey an exciting, sophisticated allure that accommodates progressive thinking and inventiveness.

")

Airports | Feb 13, 2024

New airport terminal by KPF aims to slash curb-to-gate walking time for passengers

The new Terminal A at Zayed International Airport in the United Arab Emirates features an efficient X-shape design with an average curb-to-gate walking time of just 12 minutes. The airport terminal was designed by Kohn Pedersen Fox (KPF), with Arup and Naco as engineering leads.