Though news reports and predictions painted a gloomy picture, the U.S. economy actually ended 2013 with a record setting year on Wall Street. The Dow Jones Industrial Average finished up 26.5%, its best return since 1995, and the S&P up nearly 30%, shattering previous records.

(See past articles from CBRE Healthcare)

Momentum continues to build in the housing market with positive trends in pricing, new housing starts, and inventory volume across the country. The U.S. economy added 74,000 jobs in December, as the unemployment rate fell to 6.7%, according to the Bureau of Labor Statistics.

With an improving economy and an unprecedented stimulus from the Federal Reserve continuing through 2014, the macro-economic outlook is good.

Healthcare Reform

Meanwhile, the healthcare industry has been rapidly evolving under the Affordable Care Act (ACA). Healthcare reform has compelled health systems, hospitals and physician groups to rein in sky-high costs while improving the quality of care, often coping with more regulatory requirements and less money.

Changes to reimbursement methods and reductions in healthcare provider compensation combined with an increased demand for healthcare services over the next five years, from an estimated 79 million aging baby boomers and 30 million newly insured patients, is forcing health systems to rethink their approach to balance sheet assets and liabilities, including health care real estate.

As health systems and physician groups change their delivery network, both healthcare service operators and owners of healthcare real estate are repositioning their portfolio requirements based on their growth needs. This has led to the highest medical office sales volume in the healthcare capital markets since 2007.

Healthcare reform incentives are driving consolidation of services in the industry, which has produced a robust mergers and acquisitions environment. As hospitals and healthcare organizations face mounting competitive, regulatory and financial challenges, leadership is seeking ways to capitalize on the increase of privately insured patients and Medicaid expansion while effectively serving the interests of their communities.

Healthcare operators need to diversify and expand their patient base while also becoming more efficient and leaner. This is most effectively achieved through greater economies of scale by merging with other health systems, hospitals, and physician groups, leading to a consolidation in the industry.

Consolidation is taking on two forms that are impacting real estate. First, is a unification of real estate assets as a result of health system mergers and physician employment, which has caused a consolidation of physician practices into fewer facilities that are strategically dispersed throughout the community. The other is consolidation among the hospitals and health systems seeking to concentrate operations in a single Metropolitan Statistical Area (MSA), region or state.

Off-Campus Healthcare

Healthcare investors are monitoring the consolidation trends and strategically aligning themselves through real estate transactions with market dominant hospitals and health systems, specifically those with investment grade credit ratings. Historically, investment in medical office properties revealed an institutional and REIT investor preference for core on-campus properties only.

However, over the past 12-18 months, we have witnessed little difference between core on-campus and core off-campus medical office buildings with meaningful hospital tenancy. This is a direct result of the health system shift to high quality healthcare delivered in outpatient facilities further away from traditional acute-care hospital campuses.

The care delivery network is moving from the busy, compact hospital campuses to off-campus outpatient settings with convenient access where patients live, work and shop. In response to healthcare providers commitment to off-campus destinations located near traditional retail properties and close to residential neighborhoods, investors have modified their investment criteria with a focus on off-campus properties.

The buyer pool for healthcare real estate has steadily increased over the last couple of years as investors continue to realize the inherent stability and higher returns for medical properties when compared to the more competitive multi-family, office, retail, and industrial real estate markets.

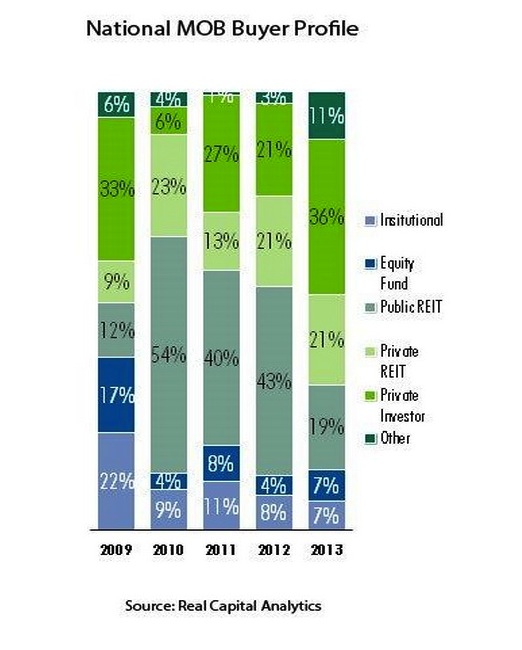

Public healthcare REITs have historically dominated the medical office investment market share, but in 2013 the private healthcare REITs and private capital investors took over the top slots. Listed and non-listed U.S. equity REITs (including both Public and Private) raised a total of $76.96 billion of equity and debt in 2013, an amount that surpassed 2012’s prior record of $73.33 billion, according to the National Association of Real Estate Investment Trusts (NAREIT). Nearly $9.3 billion, or roughly 12% was attributed to the Healthcare sector.

Conclusion

We anticipate another active year in healthcare capital markets for 2014. All investors will have stable access to capital and interest rates will likely remain at historic lows.

The favorable macro-economic outlook and consolidation among healthcare providers and continuous modification of the healthcare delivery model will continue to fuel the investment engine for what could be another record year in medical office sales.

About the authors

Lee Asher (Lee.Asher@cbre.com) and Chris Bodnar (Chris.Bodnar@cbre.com) are both Senior Vice Presidents with CBRE Healthcare Capital Markets Group. For more on CBRE Healthcare, visit www.cbre.com/healthcare.

Related Stories

| Nov 16, 2010

Architecture Billings Index: inquiries for new projects remain extremely high

The new projects inquiry index was 61.7, down slightly from a nearly three-year high mark of 62.3 in September, according to the Architecture Billings Index (ABI). However, the ABI dropped nearly two points in October; the October ABI score was 48.7, down from a reading of 50.4 the previous month. The ABI reflects the approximate nine to 12 month lag time between architecture billings and construction spending.

| Nov 16, 2010

Brazil Olympics spurring green construction

Brazil's green building industry will expand in the coming years, spurred by construction of low-impact venues being built for the 2016 Olympics. The International Olympic Committee requires arenas built for the 2016 games in Rio de Janeiro meet international standards for low-carbon emissions and energy efficiency. This has boosted local interest in developing real estate with lower environmental impact than existing buildings. The timing couldn’t be better: the Brazilian government is just beginning its long-term infrastructure expansion program.

| Nov 16, 2010

Green building market grows 50% in two years; Green Outlook 2011 report

The U.S. green building market is up 50% from 2008 to 2010—from $42 billion to $55 billion-$71 billion, according to McGraw-Hill Construction's Green Outlook 2011: Green Trends Driving Growth report. Today, a third of all new nonresidential construction is green; in five years, nonresidential green building activity is expected to triple, representing $120 billion to $145 billion in new construction.

| Nov 16, 2010

Calculating office building performance? Yep, there’s an app for that

123 Zero build is a free tool for calculating the performance of a market-ready carbon-neutral office building design. The app estimates the discounted payback for constructing a zero emissions office building in any U.S. location, including the investment needed for photovoltaics to offset annual carbon emissions, payback calculations, estimated first costs for a highly energy efficient building, photovoltaic costs, discount rates, and user-specified fuel escalation rates.

| Nov 16, 2010

CityCenter’s new Harmon Hotel targeted for demolition

MGM Resorts officials want to demolish the unopened 27-story Harmon Hotel—one of the main components of its brand new $8.5 billion CityCenter development in Las Vegas. In 2008, inspectors found structural work on the Harmon didn’t match building plans submitted to the county, with construction issues focused on improperly placed steel reinforcing bar. In January 2009, MGM scrapped the building’s 200 condo units on the upper floors and stopped the tower at 27 stories, focusing on the Harmon having just 400 hotel rooms. With the Lord Norman Foster-designed building mired in litigation, construction has since been halted on the interior, and the blue-glass tower is essentially a 27-story empty shell.

| Nov 16, 2010

Where can your firm beat the recession? Try any of these 10 places

Wondering where condos and rental apartments will be needed? Where companies are looking to rent office space? Where people will need hotel rooms, retail stores, and restaurants? Newsweek compiled a list of the 10 American cities best situated for economic recovery. The cities fall into three basic groups: Texas, the New Silicon Valleys, and the Heartland Honeys. Welcome to the recovery.

| Nov 16, 2010

Landscape architecture challenges Andrés Duany’s Congress for New Urbanism

Andrés Duany, founder of the Congress for the New Urbanism, adopted the ideas, vision, and values of the early 20th Century landscape architects/planners John Nolen and Frederick Law Olmsted, Jr., to launch a movement that led to more than 300 new towns, regional plans, and community revitalization project commissions for his firm. However, now that there’s a societal buyer’s remorse about New Urbanism, Duany is coming up against a movement that sees landscape architecture—not architecture—as the design medium more capable of organizing the city and enhancing the urban experience.

| Nov 16, 2010

Just for fun: Words that architects use

If you regularly use such words as juxtaposition, folly, truncated, and articulation, you may be an architect. Architects tend to use words rarely uttered during normal conversations. In fact, 62% of all the words that come out of an architects mouth could be replaced by a simpler and more widely known word, according to this “report.” Review this list of designer words, and once you manage to work them into daily conversation, you’re on your way to becoming a bonafide architect.

| Nov 16, 2010

NFRC approves technical procedures for attachment product ratings

The NFRC Board of Directors has approved technical procedures for the development of U-factor, solar heat gain coefficient (SHGC), and visible transmittance (VT) ratings for co-planar interior and exterior attachment products. The new procedures, approved by unanimous voice vote last week at NFRC’s Fall Membership Meeting in San Francisco, will add co-planar attachments such as blinds and shades to the group’s existing portfolio of windows, doors, skylights, curtain walls, and window film.