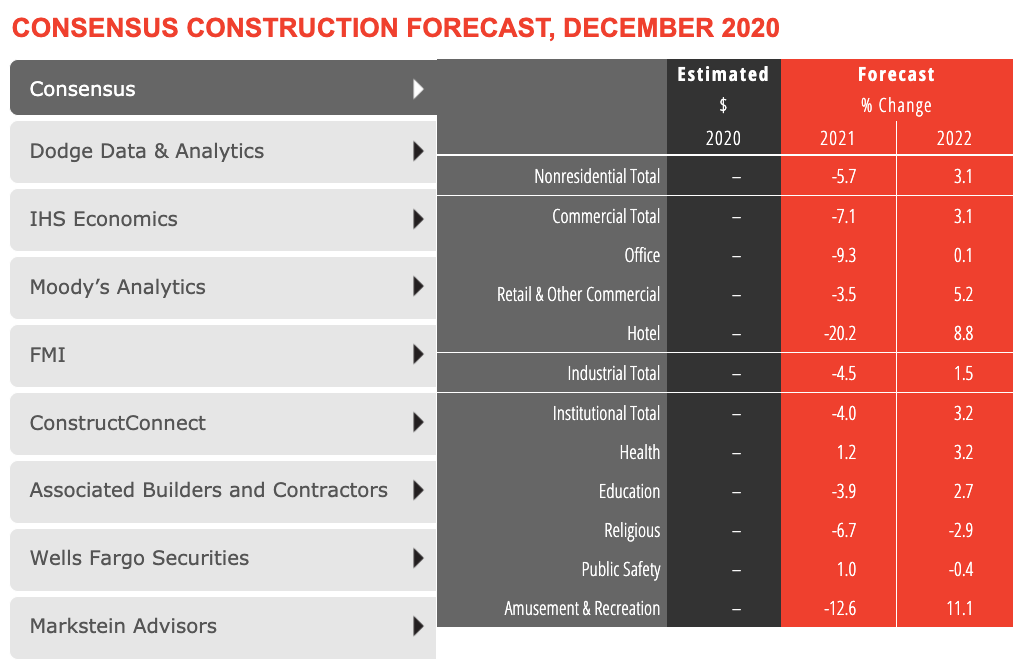

Slowing demand at architecture firms last year is expected to contribute to a projected 5.7% decline in construction spending for 2021, according to a new consensus forecast from The American Institute of Architects (AIA).

The AIA Consensus Construction Forecast Panel—comprised of leading economic forecasters—expects steep declines this year in construction spending on office buildings, hotels, and amusement and recreation centers. Health care and public safety are the only major sectors that are slated to produce gains in 2021.

Growth in nonresidential construction is expected for 2022, with 3% gains projected for the overall building market matched by both the commercial and institutional sectors.

“The December jobs report confirmed that the economy needs additional support in order to move to a sustainable economic expansion,” said AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “As pandemic concerns begin to wane and economic activity begins to pick up later in 2021, there is likely to be considerable pent-up demand for nonresidential space, leading to anticipated growth in construction spending in 2022.”

CLICK CHART TO LAUNCH INTERACTIVE CHART FROM AIA

Here are some takeaways from AIA's Chief Economist Kermit Baker, Hon. AIA:

• Hotel, airlines, and recreation industry jobs have been decimated by the pandemic. "The December jobs report confirmed that the economy needs additional support in order to move to a sustainable economic expansion. Of particular concern were the 500,000 payroll positions lost in the leisure and hospitality sector. That means that this sector has lost almost 25% of payroll positions since February 2020, matching losses in the airline industry."

• The $900 billion stimulus package passed in December 2020 is not nearly enough to sustain economic growth. "Key elements of this package include another $600 in direct payments to qualifying individuals, $300 per week in supplemental unemployment insurance for up to 11 weeks, and $280 billion designated for the Paycheck Protection Program, which provided incentives for small businesses to keep employees on their payrolls. These initiatives were generally very effective in providing a safety net for impacted households and small businesses last spring. However, they weren’t designed to provide sufficient support for an extended period of economic weakness, and the December jobs report suggests that we may already be heading into another down cycle. Even this additional funding is unlikely to provide sufficient financial support for economic growth through the entire vaccination period, suggesting that even more stimulus will be needed in the coming months or else our economy likely will be in for an extended period of stagnant growth or modest declines."

• Biden win bodes well for infrastructure investment. "With the two Georgia senate seats now in the democratic column, there are a new set of policy options for the Biden administration. Still, given the razor thin margins in both the House and the Senate, programs likely to be enacted will need to have at least modest levels of bipartisan support. An infrastructure program is likely near the top of the list of programs that both parties could support, and the Biden Administration seems ready to make this a priority, in part because it would be viewed as a stimulus program, but also because borrowing costs are near historical lows."

• Architecture firms are seeing more positive signs for the long-term. "Project inquiries from prospective and former clients have been strong recently, suggesting that new work may be picking up. More concretely, new design work coming into architecture firms has generally been more positive than billings in recent months, suggesting that firms are bringing in more project activity than they are completing. However, firms are seeing different business conditions regionally. Firms in the northeast saw the steepest downturns as the pandemic hit, and conditions remained the weakest for the remainder of the year. Business conditions at firms in the other three regions – all modestly declining – are fairly comparable."

Related Stories

Contractors | Sep 12, 2023

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of August 2023

Associated Builders and Contractors' Construction Backlog Indicator declined to 9.2 months in August, down 0.1 month, according to an ABC member survey conducted from Aug. 21 to Sept. 6. The reading is 0.5 months above the August 2022 level.

Contractors | Sep 11, 2023

Construction industry skills shortage is contributing to project delays

Relatively few candidates looking for work in the construction industry have the necessary skills to do the job well, according to a survey of construction industry managers by the Associated General Contractors of America (AGC) and Autodesk.

Market Data | Sep 6, 2023

Far slower construction activity forecast in JLL’s Midyear update

The good news is that market data indicate total construction costs are leveling off.

Giants 400 | Sep 5, 2023

Top 80 Construction Management Firms for 2023

Alfa Tech, CBRE Group, Skyline Construction, Hill International, and JLL top the rankings of the nation's largest construction management (as agent) and program/project management firms for nonresidential buildings and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Sep 5, 2023

Top 150 Contractors for 2023

Turner Construction, STO Building Group, DPR Construction, Whiting-Turner Contracting Co., and Clark Group head the ranking of the nation's largest general contractors, CM at risk firms, and design-builders for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Market Data | Sep 5, 2023

Nonresidential construction spending increased 0.1% in July 2023

National nonresidential construction spending grew 0.1% in July, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.08 trillion and is up 16.5% year over year.

Giants 400 | Aug 31, 2023

Top 35 Engineering Architecture Firms for 2023

Jacobs, AECOM, Alfa Tech, Burns & McDonnell, and Ramboll top the rankings of the nation's largest engineering architecture (EA) firms for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.