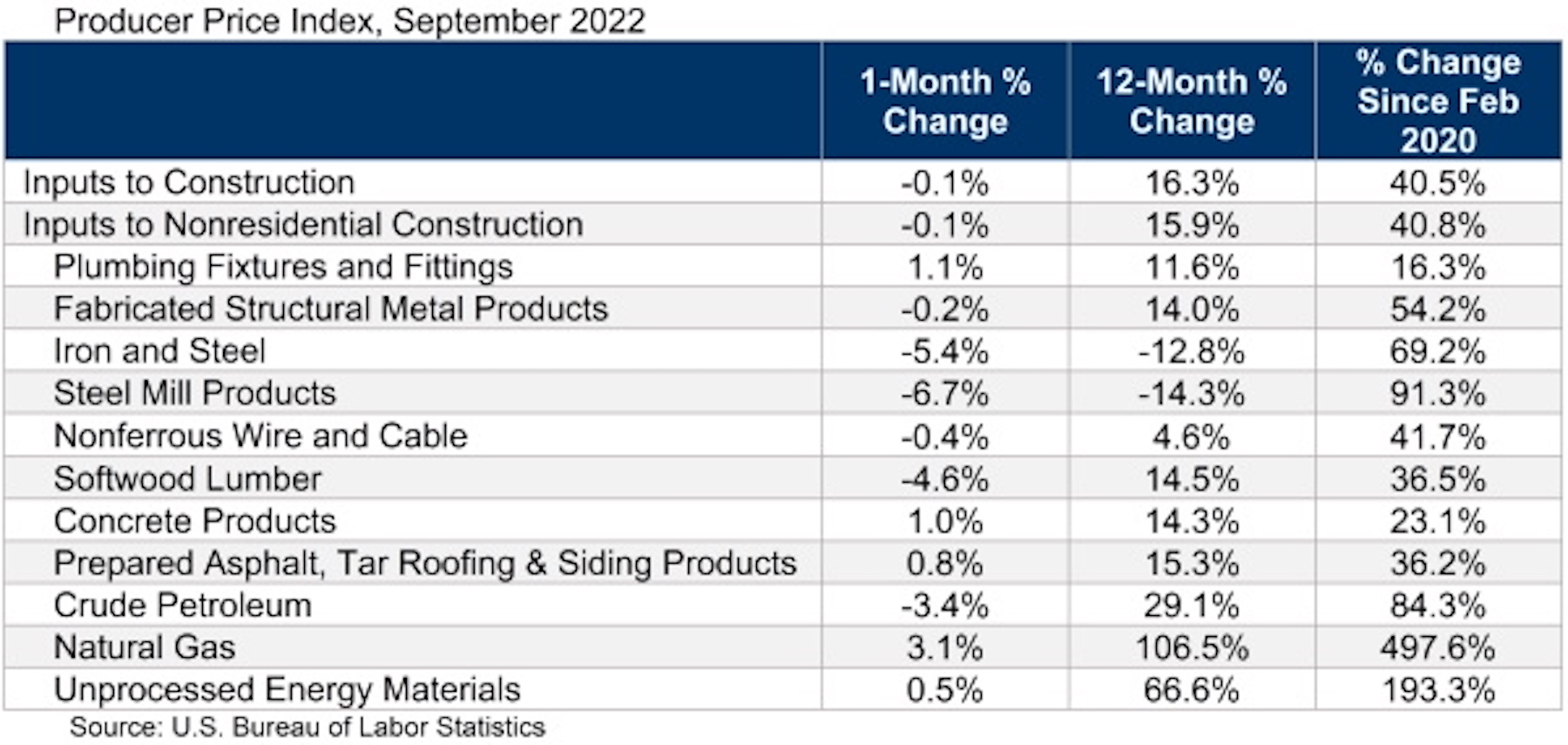

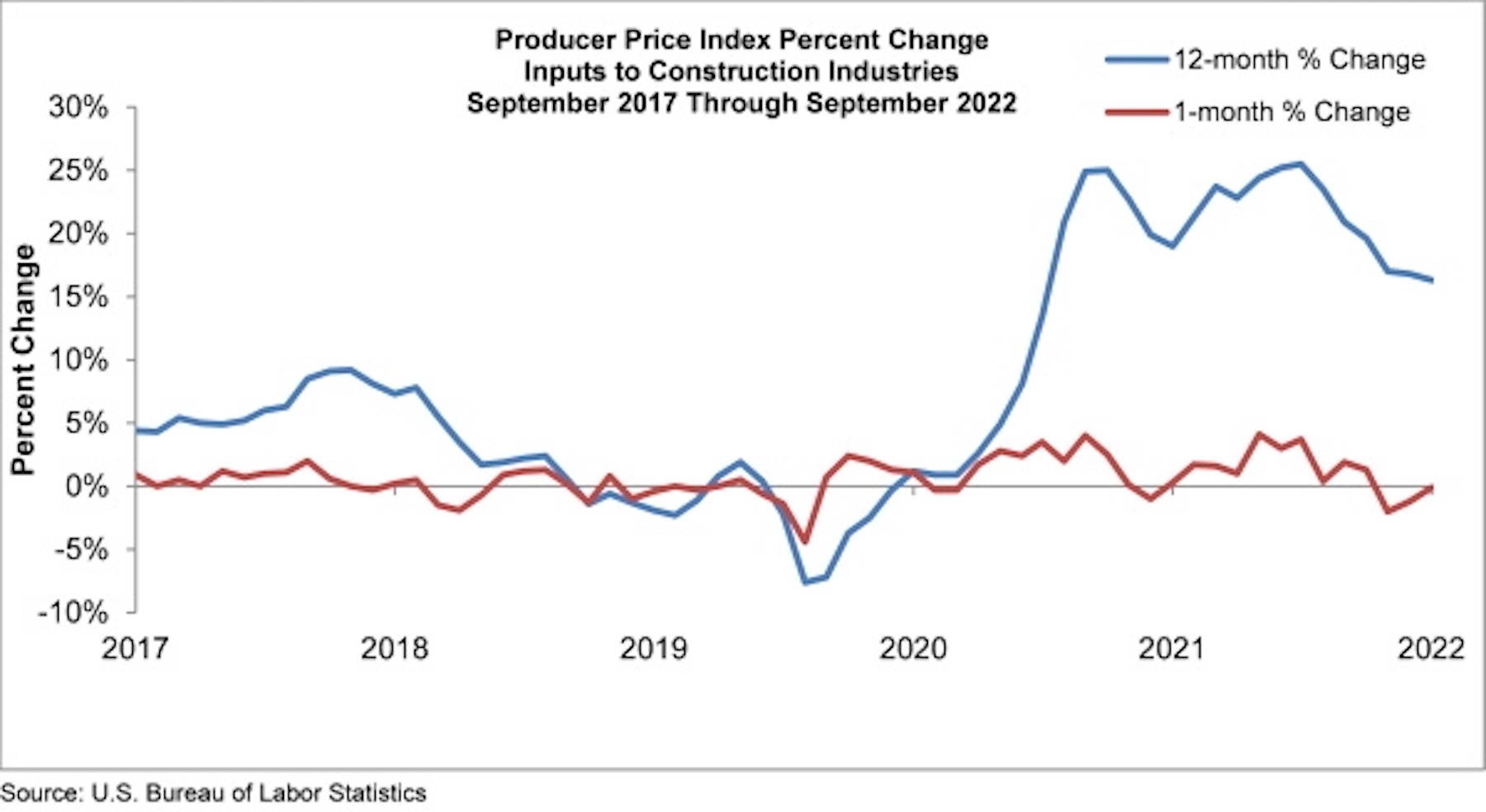

Construction input prices dipped 0.1% in September compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics’ Producer Price Index data released today. Nonresidential construction input prices also fell 0.1% for the month.

Construction input prices are up 16.3% from a year ago, while nonresidential construction input prices are 15.9% higher. Input prices were down in six of 11 subcategories on a monthly basis. Steel mill prices fell 6.7% and iron and steel prices dropped 5.4%. Natural gas prices rose 3.1%, while crude petroleum prices were down 3.4% in September. Overall producer prices expanded 0.4% in September, a larger increase than the consensus estimate of 0.2%.

“Investors and other stakeholders are eagerly awaiting any indications of meaningful declines in inflationary pressures,” said ABC Chief Economist Anirban Basu. “Elevated inflation and interest rate increases have not only undone momentum in America’s homebuilding industry but also threaten the entire global economy. There are already indications of growing financial stress, including at banking giant Credit Suisse. This is bad news for the heavily financed real estate and construction segments.

“While many American nonresidential contractors remain upbeat, according to ABC’s Construction Confidence Index, there are significant threats looming over the industry,” said Basu. “Next year stands to be a weak one for the U.S. economy as it continues to absorb the impacts of rapidly rising borrowing costs.

“Today’s PPI release strongly suggests that there is no impending end to the Federal Reserve’s rate-tightening, which means that negative factors threatening the broader economy and nonresidential construction are only getting stronger,” said Basu. “While nonresidential input prices fell slightly, inflation came in hotter than anticipated in the overall report. For contractors, the upshot is that they should be actively preparing their respective balance sheets for a downturn, even as many firms presently operate at capacity.”

Related Stories

Market Data | Nov 10, 2021

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.

Market Data | Nov 3, 2021

One-fifth of metro areas lost construction jobs between September 2020 and 2021

Beaumont-Port Arthur, Texas and Sacramento--Roseville--Arden-Arcade Calif. top lists of gainers.

Market Data | Nov 2, 2021

Construction spending slumps in September

A drop in residential work projects adds to ongoing downturn in private and public nonresidential.

Hotel Facilities | Oct 28, 2021

Marriott leads with the largest U.S. hotel construction pipeline at Q3 2021 close

In the third quarter alone, Marriott opened 60 new hotels/7,882 rooms accounting for 30% of all new hotel rooms that opened in the U.S.

Hotel Facilities | Oct 28, 2021

At the end of Q3 2021, Dallas tops the U.S. hotel construction pipeline

The top 25 U.S. markets account for 33% of all pipeline projects and 37% of all rooms in the U.S. hotel construction pipeline.

Market Data | Oct 27, 2021

Only 14 states and D.C. added construction jobs since the pandemic began

Supply problems, lack of infrastructure bill undermine recovery.

Market Data | Oct 26, 2021

U.S. construction pipeline experiences highs and lows in the third quarter

Renovation and conversion pipeline activity remains steady at the end of Q3 ‘21, with conversion projects hitting a cyclical peak, and ending the quarter at 752 projects/79,024 rooms.

Market Data | Oct 19, 2021

Demand for design services continues to increase

The Architecture Billings Index (ABI) score for September was 56.6.