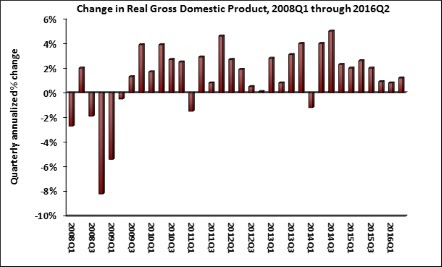

Real gross domestic product (GDP) expanded 1.2% (seasonally adjusted annual rate) during 2016’s second quarter according to according to an analysis of Bureau of Economic Analysis data released by Associated Builders and Contractors (ABC).

This modest figure follows a 0.8% annualized rate of output growth registered during the year’s first quarter.

Nonresidential fixed investment, a category closely tied to construction and other forms of business investment, fell for a third consecutive quarter, slipping 2.2% from the first quarter, with investment in structures declining 7.9%. Residential investment fell for the first time since the first quarter of 2014. Nonresidential investment in equipment fell 3.5% for the quarter, while nonresidential fixed investment in intellectual property expanded 3.5% and has now expanded for 12 consecutive quarters.

“Construction industry stakeholders should not have been anticipating a solid GDP report given previous weak construction spending and employment numbers that were recently released and they did not get one,” said Anirban Basu, ABC’s chief economist. “Today’s report suggests that construction activity has stalled a bit more than thought, largely due to slowing residential investment growth and low levels of public sector investment. With apartment rents no longer rising in a number of markets, the nation’s apartment building boom has taken a bit of a pause.

“Only those who sell directly to consumers and certain technology firms are likely to glean some sense of satisfaction from today’s release,” said Basu. “The balance of the economy continues to disappoint, though the lack of inventory building during the second quarter may help position the economy for a bounce-back during the third. It will be interesting to see if ABC’s Construction Backlog Indicator begins to show that average nonresidential construction firm backlog is now in decline, though many contractors continue to indicate that they remain busy due to previously secured work.

“It should be noted that the 7.9% decline in spending on structures during the second quarter transpired despite some very positive economic circumstances,” said Basu. “For instance, interest rates remain shockingly low, foreign investment continues to pour into U.S. commercial real estate, and there are positive wealth effects being generated by both housing and equity markets. However, it appears that even these conditions are no longer enough to support growing demand for construction spending. One could theorize that uncertainty originating from the current presidential election cycle is partially responsible.”

The following highlights emerged from today’s second quarter GDP release. All growth figures are seasonally adjusted annual rates:

- Personal consumption expenditures expanded 4.2% on an annualized basis during the second quarter of 2016 after growing 1.6% during the first quarter of 2016.

- Spending on goods rose 6.8% during the first quarter after expanding by 1.2% during the previous quarter.

- Real final sales of domestically produced output increased 2.4% in the second quarter after increasing 1.2% in the first.

- Federal government spending inched down by 0.2% in the year’s second quarter after contracting 1.5% in the first quarter of 2016.

- Nondefense government spending increased by 3.9% for the quarter following an increase of 0.9% in the first.

- National defense spending fell by 3% during the second quarter after registering a 3.2% decline in the previous quarter.

- State and local government spending fell by 1.3% in the second quarter after expanding 3.5% in the first quarter.

Related Stories

Market Data | Nov 27, 2023

Number of employees returning to the office varies significantly by city

While the return-to-the-office trend is felt across the country, the percentage of employees moving back to their offices varies significantly according to geography, according to Eptura’s Q3 Workplace Index.

Market Data | Nov 14, 2023

The average U.S. contractor has 8.4 months worth of construction work in the pipeline, as of September 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator declined to 8.4 months in October from 9.0 months in September, according to an ABC member survey conducted from Oct. 19 to Nov. 2. The reading is down 0.4 months from October 2022. Backlog now stands at its lowest level since the first quarter of 2022.

Multifamily Housing | Nov 9, 2023

Multifamily project completions forecast to slow starting 2026

Yardi Matrix has released its Q4 2023 Multifamily Supply Forecast, emphasizing a short-term spike and plateau of new construction.

Contractors | Nov 1, 2023

Nonresidential construction spending increases for the 16th straight month, in September 2023

National nonresidential construction spending increased 0.3% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.1 trillion.

Market Data | Oct 23, 2023

New data finds that the majority of renters are cost-burdened

The most recent data derived from the 2022 Census American Community Survey reveals that the proportion of American renters facing housing cost burdens has reached its highest point since 2012, undoing the progress made in the ten years leading up to the pandemic.

Contractors | Oct 19, 2023

Crane Index indicates slowing private-sector construction

Private-sector construction in major North American cities is slowing, according to the latest RLB Crane Index. The number of tower cranes in use declined 10% since the first quarter of 2023. The index, compiled by consulting firm Rider Levett Bucknall (RLB), found that only two of 14 cities—Boston and Toronto—saw increased crane counts.

Market Data | Oct 2, 2023

Nonresidential construction spending rises 0.4% in August 2023, led by manufacturing and public works sectors

National nonresidential construction spending increased 0.4% in August, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.09 trillion.

Giants 400 | Sep 28, 2023

Top 100 University Building Construction Firms for 2023

Turner Construction, Whiting-Turner Contracting Co., STO Building Group, Suffolk Construction, and Skanska USA top BD+C's ranking of the nation's largest university sector contractors and construction management firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all university/college-related buildings except student residence halls, sports/recreation facilities, laboratories, S+T-related buildings, parking facilities, and performing arts centers (revenue for those buildings are reported in their respective Giants 400 ranking).

Construction Costs | Sep 28, 2023

U.S. construction market moves toward building material price stabilization

The newly released Quarterly Construction Cost Insights Report for Q3 2023 from Gordian reveals material costs remain high compared to prior years, but there is a move towards price stabilization for building and construction materials after years of significant fluctuations. In this report, top industry experts from Gordian, as well as from Gilbane, McCarthy Building Companies, and DPR Construction weigh in on the overall trends seen for construction material costs, and offer innovative solutions to navigate this terrain.

Data Centers | Sep 21, 2023

North American data center construction rises 25% to record high in first half of 2023, driven by growth of artificial intelligence

CBRE’s latest North American Data Center Trends Report found there is 2,287.6 megawatts (MW) of data center supply currently under construction in primary markets, reaching a new all-time high with more than 70% already preleased.