Construction industry leaders remained confident regarding nonresidential construction prospects in February 2019, according to the latest Construction Confidence Index released by Associated Builders and Contractors.

All three principal components measured by the survey—sales, profit margins, and staffing levels—remain well above the diffusion index threshold of 50, signaling ongoing expansion in construction activity.

Only 3.4% of contractors expect to reduce staffing levels over the next six months, and more than 70% of survey respondents expect their sales to increase through the initial half of 2019.

Still, 31.4% of contractors expect profit margins to remain unchanged, likely due in large measure to rising worker compensation costs.

Index breakdown:

• The CCI for sales expectations increased from 68.4 to 69.4 in February.

• The CCI for profit margin expectations increased from 60.6 to 63.3.

• The CCI for staffing levels increased from 68.2 to 68.5.

“Confidence seems to be making a comeback in America,” said ABC Chief Economist Anirban Basu. “There was a time when consumer, small business and investor confidence was falling. For now, that dynamic has evaporated, with job growth continuing and U.S. equity prices heading higher of late. Contractors understand the performance of the broader economy today helps shape the construction environment of tomorrow. Accordingly, with strong economic data like the Construction Backlog Indicator—which stood at 8.8 months in February 2019—and nonresidential construction spending, which increased 4.8% year over year, contractor confidence remains elevated.

“That said, contractors continue to wrestle with ever-larger skilled workforce shortfalls, which are making it more difficult to deliver construction services on time and on budget,” said Basu. “This helps explain why the CCI reading for profit margins remains meaningfully lower than the corresponding reading for sales expectations. Despite expanding compensation costs, contractors expect to significantly increase staffing levels going forward, an indication that many busy contractors expect to get busier. The fact that the profit margin reading remains above 50 also suggests that contractors enjoy a degree of pricing power and are able to pass at least some of their higher costs along to customers. Slower growth in construction materials prices relative to last year represents another likely factor shaping survey results.”

CCI is a diffusion index. Readings above 50 indicate growth, while readings below 50 are unfavorable.

Related Stories

Multifamily Housing | May 18, 2021

Multifamily housing sector sees near record proposal activity in early 2021

The multifamily sector led all housing submarkets, and was third among all 58 submarkets tracked by PSMJ in the first quarter of 2021.

Market Data | May 18, 2021

Grumman|Butkus Associates publishes 2020 edition of Hospital Benchmarking Survey

The report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | May 13, 2021

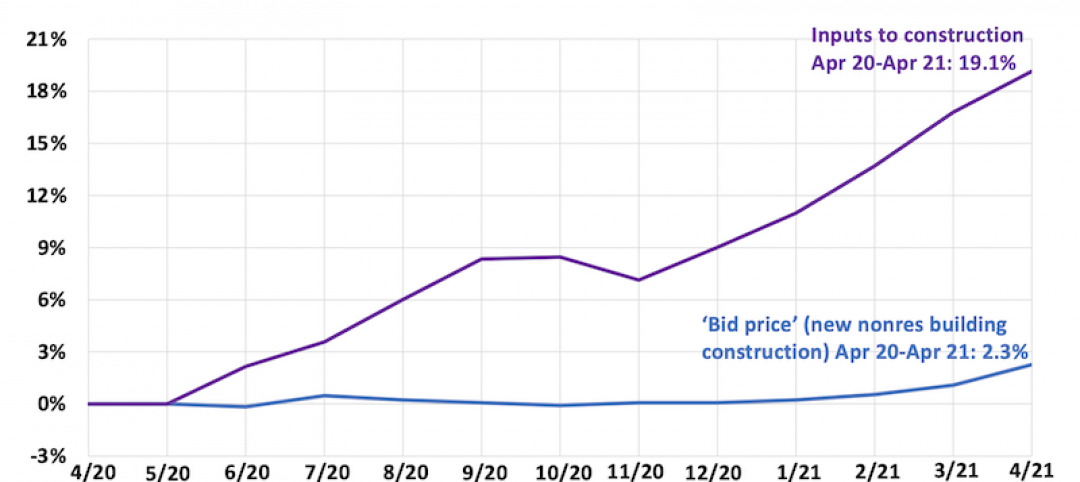

Proliferating materials price increases and supply chain disruptions squeeze contractors and threaten to undermine economic recovery

Producer price index data for April shows wide variety of materials with double-digit price increases.

Market Data | May 7, 2021

Construction employment stalls in April

Soaring costs, supply-chain challenges, and workforce shortages undermine industry's recovery.

Market Data | May 4, 2021

Nonresidential construction outlays drop in March for fourth-straight month

Weak demand, supply-chain woes make further declines likely.

Market Data | May 3, 2021

Nonresidential construction spending decreases 1.1% in March

Spending was down on a monthly basis in 11 of the 16 nonresidential subcategories.

Market Data | Apr 30, 2021

New York City market continues to lead the U.S. Construction Pipeline

New York City has the greatest number of projects under construction with 110 projects/19,457 rooms.

Market Data | Apr 29, 2021

U.S. Hotel Construction pipeline beings 2021 with 4,967 projects/622,218 rooms at Q1 close

Although hotel development may still be tepid in Q1, continued government support and the extension of programs has aided many businesses to get back on their feet as more and more are working to re-staff and re-open.

Market Data | Apr 28, 2021

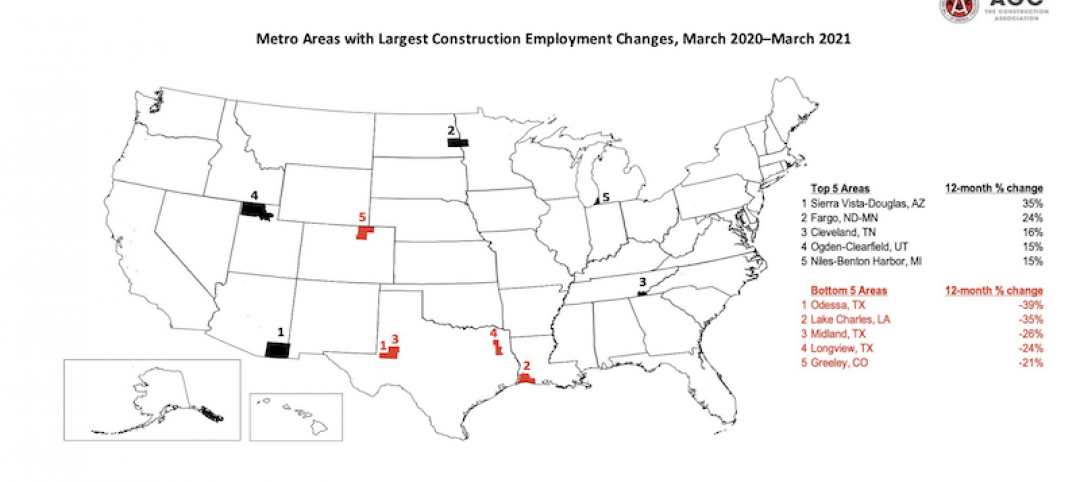

Construction employment declines in 203 metro areas from March 2020 to March 2021

The decline occurs despite homebuilding boom and improving economy.

Market Data | Apr 20, 2021

The pandemic moves subs and vendors closer to technology

Consigli’s latest market outlook identifies building products that are high risk for future price increases.