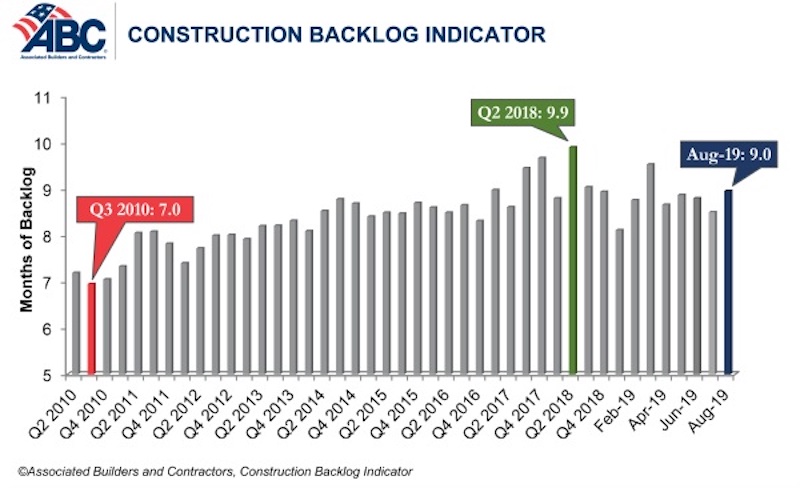

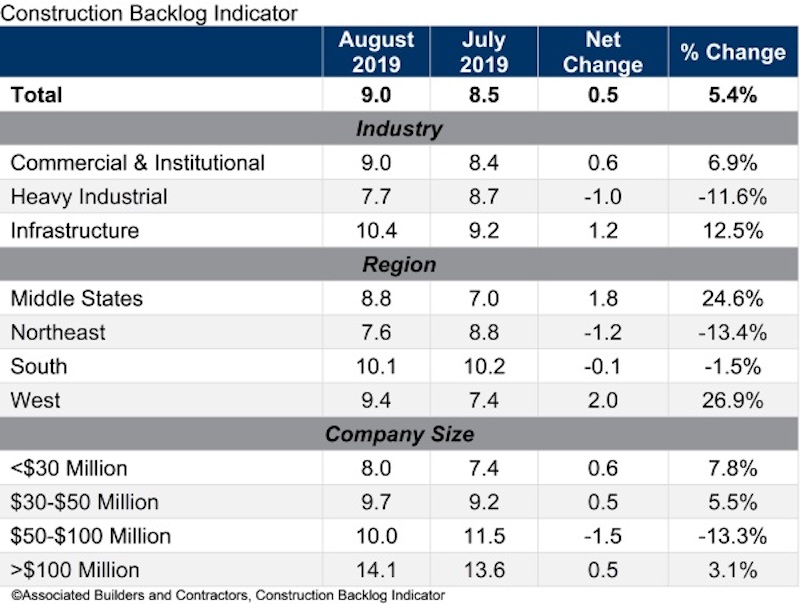

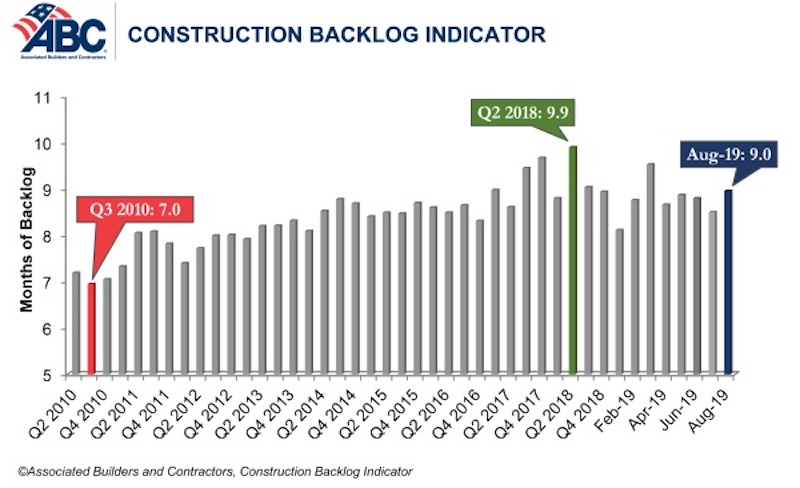

Associated Builders and Contractors reported today that its Construction Backlog Indicator climbed to nine months in August 2019, up 0.5 months or 5.4% from July 2019, when CBI stood at 8.5 months.

“Despite some other leading indicators suggesting weakening in nonresidential construction spending, our most recent backlog readings show that contractors are still experiencing significant demand for construction services” said ABC Chief Economist Anirban Basu. “The primary issue for most contractors is not a lack of demand, but an ongoing and worsening shortage of skilled workers available to meet contractual requirements.

“Though this month’s report was generally positive, softening activity in the nation’s manufacturing sector is becoming more apparent in construction data,” said Basu. “Specifically, backlog in the heavy industrial category slipped to 7.7 months in August, a decline of 12%. A number of key manufacturing indicators have been weakening of late, including capacity utilization and the Institute for Supply Management’s index for manufacturing. It appears that the slowdown in factory activity is now being reflected in construction spending data.

“By contrast, backlog for those involved in heavy highway projects or other forms of infrastructure reached 10.4 months, an increase of nearly 13%,” said Basu. “The implication is that state and local governments are leveraging stronger fiscal positions and lower borrowing costs to move forward with more infrastructure projects. Not only is this a source of strength for the U.S. economy, it is helping to support overall nonresidential construction spending. Growing contractual volume in the infrastructure category helped to push backlog among Middle States contractors up to 8.8 months, a 1.8-month gain. Overall, backlog continues to be lengthiest in the South and West.”

Related Stories

Multifamily Housing | May 18, 2021

Multifamily housing sector sees near record proposal activity in early 2021

The multifamily sector led all housing submarkets, and was third among all 58 submarkets tracked by PSMJ in the first quarter of 2021.

Market Data | May 18, 2021

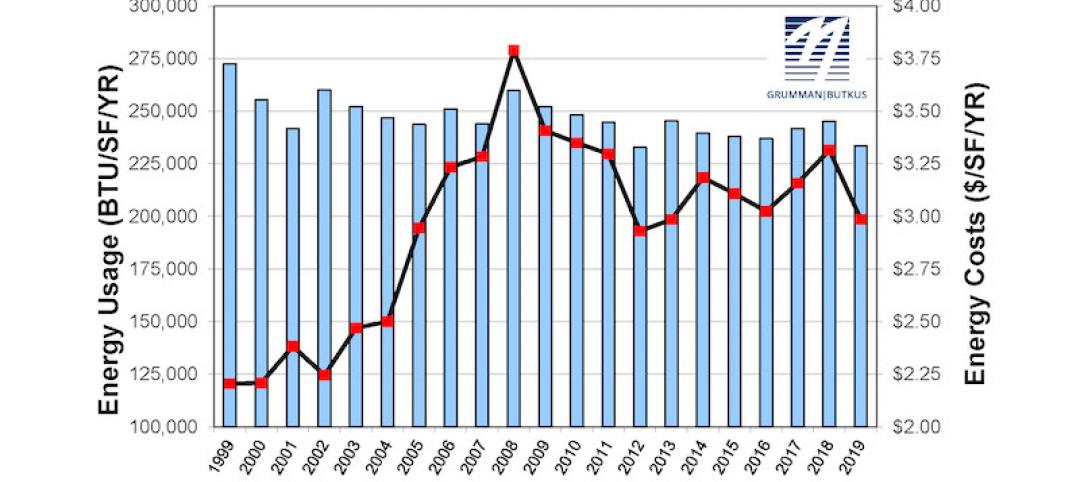

Grumman|Butkus Associates publishes 2020 edition of Hospital Benchmarking Survey

The report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | May 13, 2021

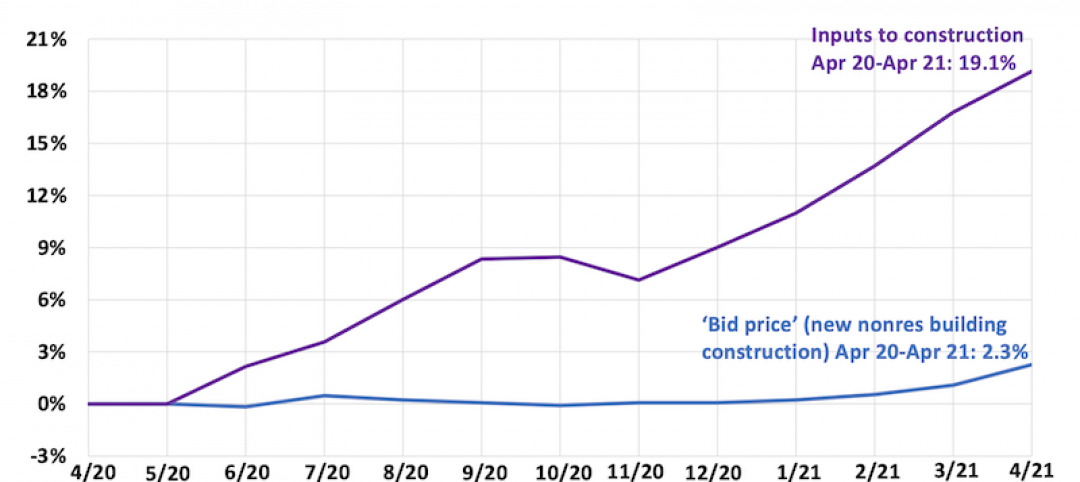

Proliferating materials price increases and supply chain disruptions squeeze contractors and threaten to undermine economic recovery

Producer price index data for April shows wide variety of materials with double-digit price increases.

Market Data | May 7, 2021

Construction employment stalls in April

Soaring costs, supply-chain challenges, and workforce shortages undermine industry's recovery.

Market Data | May 4, 2021

Nonresidential construction outlays drop in March for fourth-straight month

Weak demand, supply-chain woes make further declines likely.

Market Data | May 3, 2021

Nonresidential construction spending decreases 1.1% in March

Spending was down on a monthly basis in 11 of the 16 nonresidential subcategories.

Market Data | Apr 30, 2021

New York City market continues to lead the U.S. Construction Pipeline

New York City has the greatest number of projects under construction with 110 projects/19,457 rooms.

Market Data | Apr 29, 2021

U.S. Hotel Construction pipeline beings 2021 with 4,967 projects/622,218 rooms at Q1 close

Although hotel development may still be tepid in Q1, continued government support and the extension of programs has aided many businesses to get back on their feet as more and more are working to re-staff and re-open.

Market Data | Apr 28, 2021

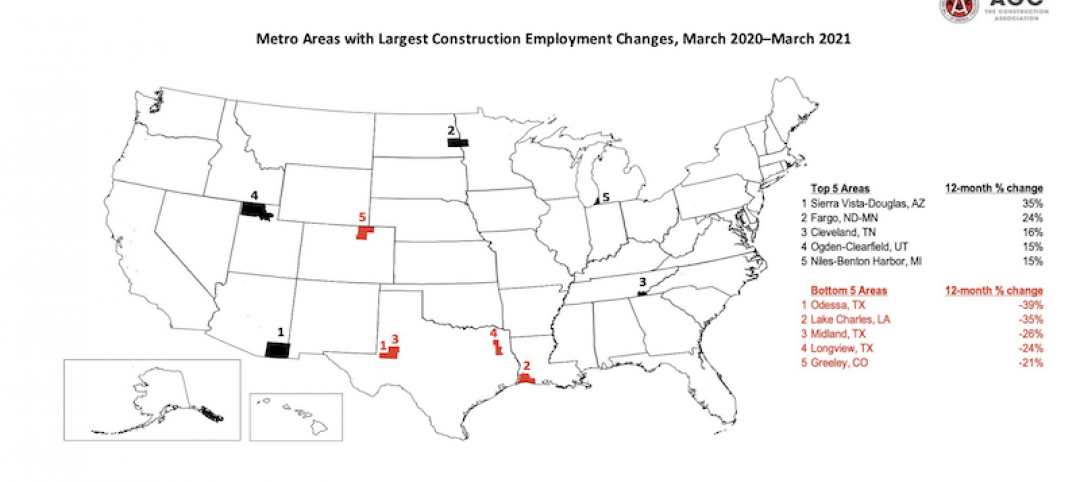

Construction employment declines in 203 metro areas from March 2020 to March 2021

The decline occurs despite homebuilding boom and improving economy.

Market Data | Apr 20, 2021

The pandemic moves subs and vendors closer to technology

Consigli’s latest market outlook identifies building products that are high risk for future price increases.