Proposal activity for architecture, engineering and construction (A/E/C) firms increased significantly in the 1st Quarter of 2023, according to PSMJ’s Quarterly Market Forecast (QMF) survey. The predictive measure of the industry’s health rebounded to a net plus/minus index (NPMI) of 32.8 in the first three months of the year. This followed the 8.0 NPMI in the 4th Quarter of 2022, which marked the lowest level since the final quarter of 2020 and the second-lowest NPMI recorded in the last 10 years.

PSMJ President Greg Hart noted that the 1st quarter results are a pleasant surprise, especially since data was collected after the Silicon Valley Bank collapse and amid continuing interest rate hikes and recession predictions. “I don’t think anybody expected this kind of recovery,” he said. “But inflation is cooling and there are some positive signs in the housing market, so maybe we’ve found the bottom.”

First quarter results have historically been the strongest throughout the history of the QMF survey, which may play some part in the jump in project opportunities. In the last 10 years, the first quarter NPMI averaged 45.2, with the results weakening in subsequent quarters. The average NPMI for the 2nd quarter since 2013 is 36.5, with the third and fourth quarters averaging 29.0 and 25.7, respectively. Year-over-year, the NPMI for the first three months of 2023 was down substantially from a near-record NPMI of 60.2 reported in the first quarter of 2022.

PSMJ’s proprietary NPMI is the difference between the percentage of respondents who say that proposal opportunities are growing and those reporting a decrease. In addition to overall activity, the QMF surveys A/E/C firm leaders about their proposal activity experience in 12 major markets and 58 submarkets.

Private Sector Construction Markets Struggle, Publics Thrive

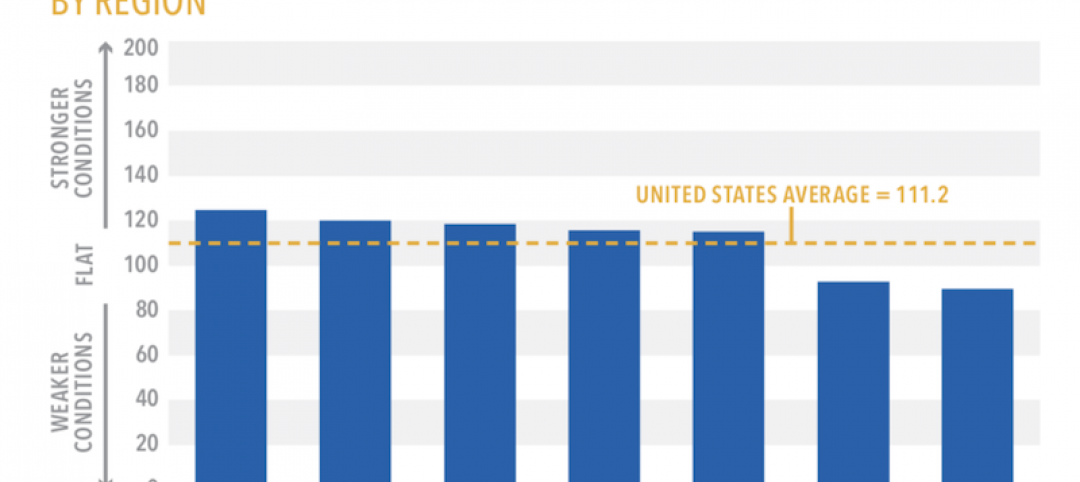

Firms working in private-sector markets continue to report historically low levels of proposal activity, while those in the public sector perform better, as the chart below indicates. Environmental topped all 12 major markets with an NPMI of 71.4, followed by Water/Wastewater at 70.8. Transportation continues to thrive, aided by the Infrastructure Investment and Jobs Act (IIJA), with an NPMI of 65.5. Energy/Utilities remains solid, repeating its fourth-place finish from the prior quarter and a near-exact NPMI of 55.1 (down from 55.2).

Since the 1st quarter of 2019, the Energy/Utilities market has been out of the top five only once (the 2nd quarter of 2021), and the Water/Wastewater market has missed the top five just twice.

The biggest surprise of the 1st Quarter may be that Education was the fifth-strongest among the major markets with an NPMI of 42.2. This is the first time that Education hit the top five since the 2nd quarter of 2018. The Higher Education (NPMI of 45.3) and K-12 (42.3) submarkets drove the resurgence.

Related Stories

Market Data | Dec 19, 2018

Brokers look forward to a commercial real estate market that mirrors 2018’s solid results

Respondents to a recent Transwestern poll expect flat to modest growth for rents and investment in offices, MOBs, and industrial buildings.

Market Data | Dec 19, 2018

When it comes to economic clout, New York will far outpace other U.S. metros for decades to come

But San Jose, Calif., is expected to have the best annual growth rate through 2035, according to Oxford Economics’ latest Global Cities report.

Market Data | Dec 19, 2018

Run of positive billings continues at architecture firms

November marked the fourteenth consecutive month of increasing demand for architectural firm services.

Market Data | Dec 5, 2018

ABC predicts construction sector will remain strong in 2019

Job growth, high backlog and healthy infrastructure investment all spell good news for the industry.

Market Data | Dec 4, 2018

Nonresidential spending rises modestly in October

Thirteen out of 16 subsectors are associated with year-over-year increases.

Market Data | Nov 20, 2018

Construction employment rises from October 2017 to October 2018 in 44 states and D.C.

Texas has biggest annual job increase while New Jersey continues losses; Iowa, Florida and California have largest one-month gains as Mississippi and Louisiana trail.

Market Data | Nov 15, 2018

Architecture firm billings continue to slow, but remain positive in October

Southern region reports decline in billings for the first time since June 2012.

Market Data | Nov 14, 2018

A new Joint Center report finds aging Americans less prepared to afford housing

The study foresees a significant segment of seniors struggling to buy or rent on their own or with other people.

Market Data | Nov 12, 2018

Leading hotel markets in the U.S. construction pipeline

Projects already under construction and those scheduled to start construction in the next 12 months, combined, have a total of 3,782 projects/213,798 rooms and are at cyclical highs.

Market Data | Nov 6, 2018

Unflagging national office market enjoys economic tailwinds

Stable vacancy helped push asking rents 4% higher in third quarter.