The relatively steep slowdown in the growth in construction spending in recent years might suggest that this year might result in a decline in overall spending. However, quite the contrary, the AIA Consensus Construction Forecast panel is projecting a modest pick-up in the growth rate, and another solid performance in 2019. There appear to be several factors behind this optimism:

1. Rebuilding and repairs from natural disasters: The National Oceanographic and Atmospheric Administration recently reported its 2017 estimate of losses from major natural disasters like hurricanes, wildfires, and flooding. At $306 billion, it easily shattered the previous record of $215 billion (adjusted for inflation) set in 2005 from the impacts of Katrina, Rita, Wilma, and Dennis. While the totality of these loss figures won’t be directly translated into rebuilding and repair activity, they will produce significant opportunities for the construction sector. Existing research suggests that the duration of rebuilding activity after natural disasters is significant, with the peak in spending generally occurring two to three years after the event.

2. Tax reform implications for construction: The recently enacted tax reform package dramatically reduced the nominal tax rates for businesses, and some of these savings will likely be reinvested back into the businesses. With capital expenditures able to be expensed rather than depreciated under the tax act, businesses have even more incentive to invest in their businesses. The impact of tax reform on business profitability will vary by industry, with more capital intensive industries (e.g. utilities, real estate, and transportation) and those with higher effective tax rates (e.g. agriculture, financial services) potentially benefiting the most. In contrast, the single-family housing market recovery is likely to be slowed by the tax package. The lower limits for the deductibility of mortgage interest, as well as the cap set on state and local tax deductions (including property taxes) reduce the tax preferences for homeownership, and likely will moderate growth in house prices, particularly for upper-end homes in areas with high state and local tax rates.

3. Possibility of an infrastructure package: A priority of the Trump administration has been an infrastructure investment program. There have been several versions floated, with the current iteration calling for a $200-billion federal investment over the coming decade leveraging and additional $800 billion in state, local, and private investment. The details of such a program, and the likelihood of its being implemented, should unfold over the coming weeks.

4. Strong consumer and business confidence levels: Consumer sentiment—as measured by the University of Michigan consumer sentiment index—turned up in the latter part of 2017, with fourth-quarter figures at their highest levels in almost two decades. Likewise, business confidence levels in 2017, as measured by the Conference Board’s CEO business confidence survey, were at their highest point since before the last recession. These indicators suggest broad confidence in economic conditions across both households and businesses, and a willingness to spend and invest.

5. Leading economic indicators for the construction sector: While there are several “special circumstances” that may provide growth opportunities for the construction sector this year, there are other more basic indicators that point to growth. AIA’s ABI has been signaling growth in design activity for most of the past year, which would point to a comparable upturn in construction activity throughout 2018. Even more significant, the AIA’s index for new design projects coming into architecture firms saw an even sharper upturn than the overall ABI in 2017, demonstrating a growing pipeline for design activity. Additionally, both Dodge Data and Analytics and ConstructConnect reported strong gains in nonresidential building starts in 2017, demonstrating considerable building activity currently under way.

Related Stories

Industry Research | Jun 15, 2017

Commercial Construction Index indicates high revenue and employment expectations for 2017

USG Corporation (USG) and U.S. Chamber of Commerce release survey results gauging confidence among industry leaders.

Industry Research | Jun 13, 2017

Gender, racial, and ethnic diversity increases among emerging professionals

For the first time since NCARB began collecting demographics data, gender equity improved along every career stage.

Industry Research | May 25, 2017

Project labor agreement mandates inflate cost of construction 13%

Ohio schools built under government-mandated project labor agreements (PLAs) cost 13.12 percent more than schools that were bid and constructed through fair and open competition.

Market Data | May 24, 2017

Design billings increasing entering height of construction season

All regions report positive business conditions.

Market Data | May 24, 2017

The top franchise companies in the construction pipeline

3 franchise companies comprise 65% of all rooms in the Total Pipeline.

Industry Research | May 24, 2017

These buildings paid the highest property taxes in 2016

Office buildings dominate the list, but a residential community climbed as high as number two on the list.

Market Data | May 16, 2017

Construction firms add 5,000 jobs in April

Unemployment down to 4.4%; Specialty trade jobs dip slightly.

Industry Research | May 4, 2017

How your AEC firm can go from the shortlist to winning new business

Here are four key lessons to help you close more business.

Engineers | May 3, 2017

At first buoyed by Trump election, U.S. engineers now less optimistic about markets, new survey shows

The first quarter 2017 (Q1/17) of ACEC’s Engineering Business Index (EBI) dipped slightly (0.5 points) to 66.0.

Market Data | May 2, 2017

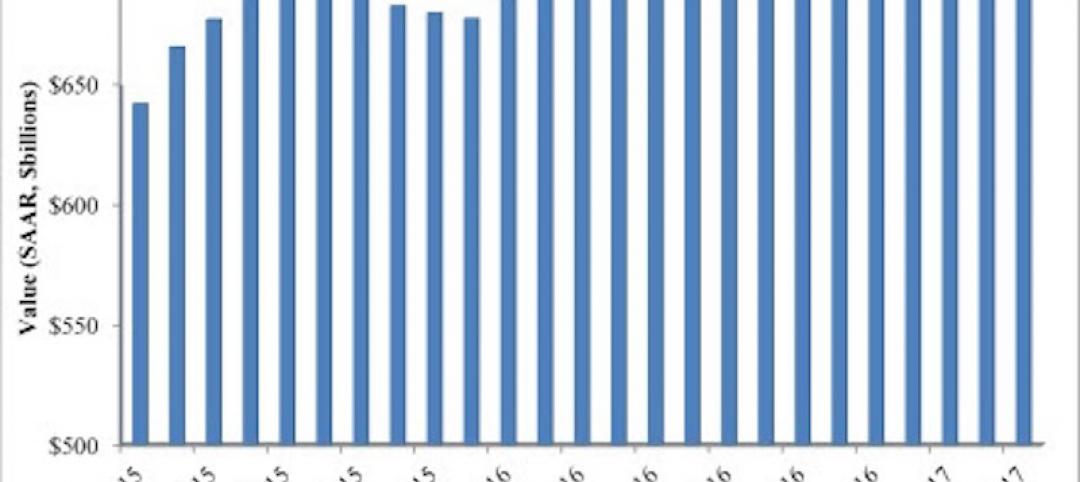

Nonresidential Spending loses steam after strong start to year

Spending in the segment totaled $708.6 billion on a seasonally adjusted, annualized basis.