Commercial and institutional construction spending is projected to be down 6.9 percent and 13 percent, respectively, in 2022, impacted by macroeconomic factors that include increasing demand for long-lead equipment, material shortages caused by supply-chain snags and the Russia-Ukraine war, and the instability of costs for fuel and labor.

That easing of demand has allowed key commodity prices to stabilize, and there is reason for optimism despite uncertainty about the health of the U.S economy that is only expected to expand by 1 percent next year.

This is the perspective of Linesight, a multinational construction consultant, which has released its Third Quarter Commodity Report for the United States. Patrick Ryan, Linesight’s Executive Vice President for the Americas, states that the “medium to long-term outlook remains positive, with [economic] growth expected in the coming years as inflation comes under control.”

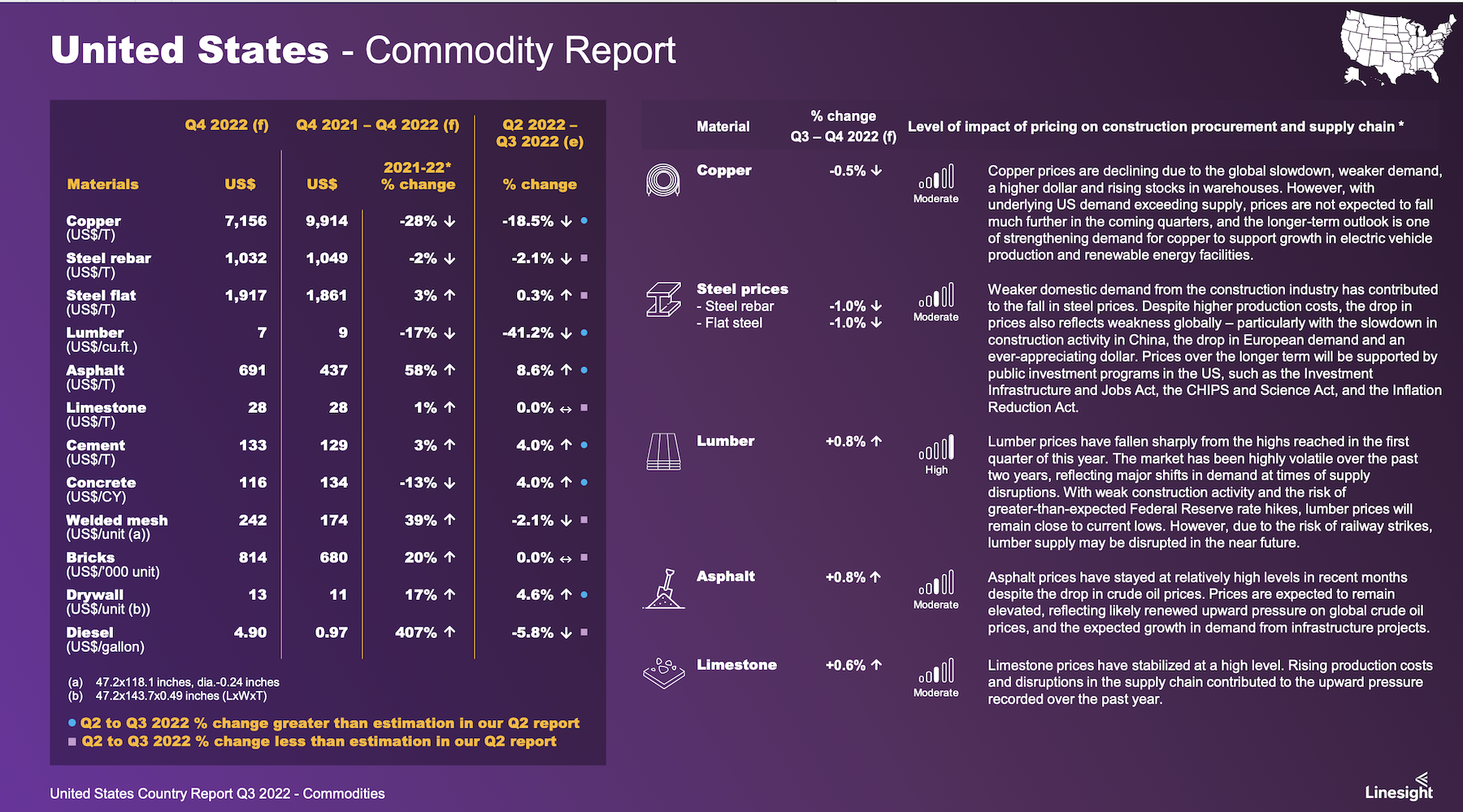

The Report focuses on five key commodities:

•Lumber, whose prices have been on a downward trend since the first quarter. Supply-side fragilities have eased, as post-flood mill inventory in British Columbia is rebuilding.

•Cement and aggregates, whose prices have been affected by oil price turbulence. Linesight sees the slowdown in residential construction as easing pressure on this commodity’s demand, although that could also be negated by commercial demand spurred by the Infrastructure Investment and Jobs Act of 2021.

•Concrete blocks and bricks, whose prices are waning along with residential construction demand that is tamped by rising mortgage interest rates.

•Rebar and structural steel, whose prices had flattened during the previous quarter, and whose weakening future demand, especially from China, anticipates falling prices. However, Linesight also cautions that high energy prices continue to drive up steel’s production costs.

•Copper, whose price declines of late have stabilized. Supply disruptions and the lack of investment in new mining operations continue to contribute to production shortfalls, and demand remains “resilient,” especially as the manufacture of electric vehicle batteries expands.

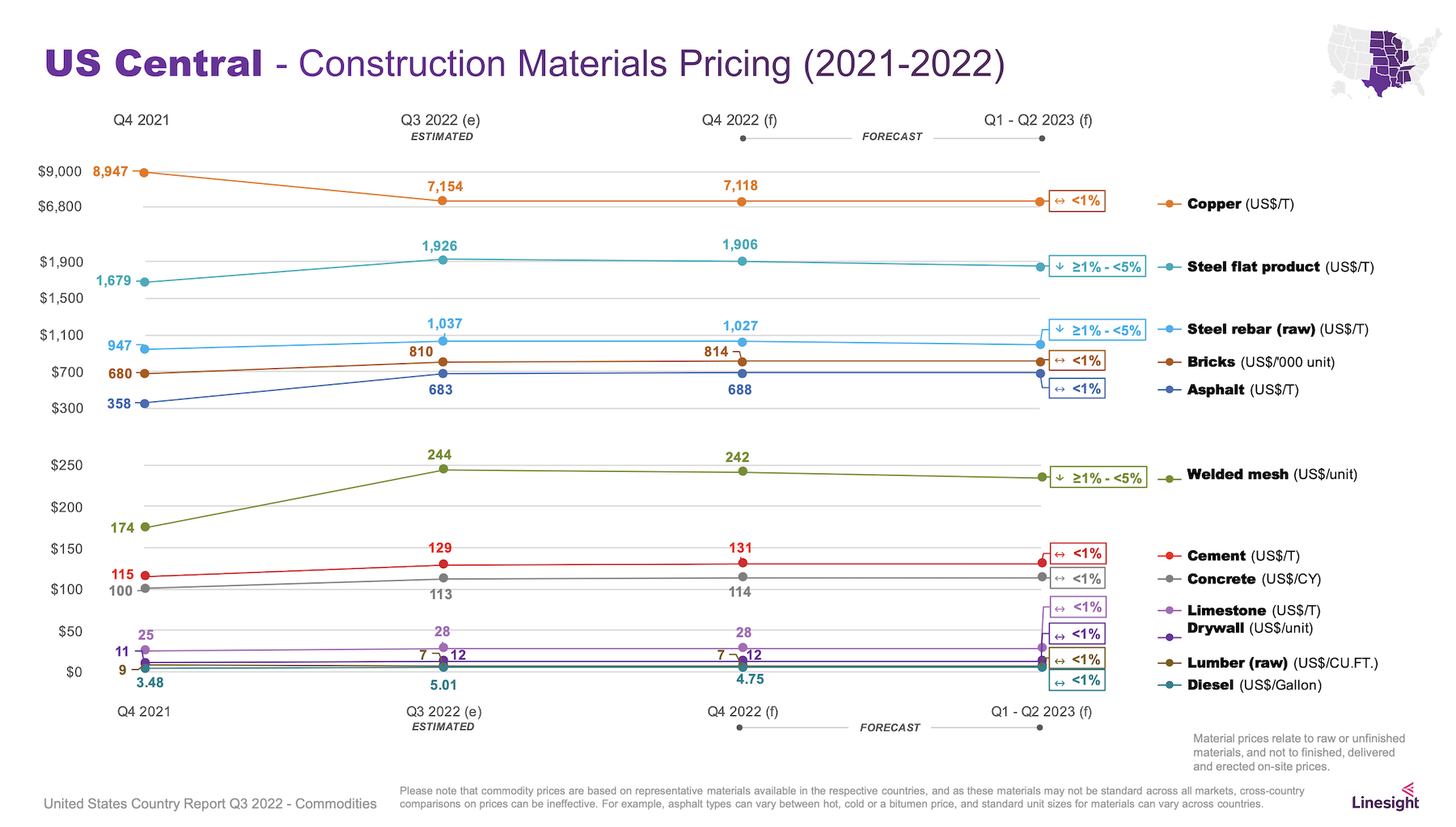

The Report prognosticates as well about pricing for asphalt, limestone, welded mesh, drywall, and diesel fuel. It also forecasts commodity prices by regions of the country, although the geographic variations are, for the most part, marginal.

Perhaps the most important issue right now affecting commodity prices, says Ryan, is mixed data on the economy. Despite two consecutive quarterly declines, “there are positive indicators being recorded to suggest economic resilience in some key areas,” such as the lowest unemployment rate in five decades, and the Federal Reserve’s aggressive actions to curb inflation.

Another bright spot is labor productivity in the U.S., which still outpaces Germany, the United Kingdom, Hong Kong, Taiwan, South Korea, and Japan.

Related Stories

Market Data | May 12, 2022

Monthly construction input prices increase in April

Construction input prices increased 0.8% in April compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics’ Producer Price Index data released today.

Market Data | May 10, 2022

Hybrid work could result in 20% less demand for office space

Global office demand could drop by between 10% and 20% as companies continue to develop policies around hybrid work arrangements, a Barclays analyst recently stated on CNBC.

Market Data | May 6, 2022

Nonresidential construction spending down 1% in March

National nonresidential construction spending was down 0.8% in March, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau.

Market Data | Apr 29, 2022

Global forces push construction prices higher

Consigli’s latest forecast predicts high single-digit increases for this year.

Market Data | Apr 29, 2022

U.S. economy contracts, investment in structures down, says ABC

The U.S. economy contracted at a 1.4% annualized rate during the first quarter of 2022.

Market Data | Apr 20, 2022

Pace of demand for design services rapidly accelerates

Demand for design services in March expanded sharply from February according to a new report today from The American Institute of Architects (AIA).

Market Data | Apr 14, 2022

FMI 2022 construction spending forecast: 7% growth despite economic turmoil

Growth will be offset by inflation, supply chain snarls, a shortage of workers, project delays, and economic turmoil caused by international events such as the Russia-Ukraine war.

Industrial Facilities | Apr 14, 2022

JLL's take on the race for industrial space

In the previous decade, the inventory of industrial space couldn’t keep up with demand that was driven by the dual surges of the coronavirus and online shopping. Vacancies declined and rents rose. JLL has just published a research report on this sector called “The Race for Industrial Space.” Mehtab Randhawa, JLL’s Americas Head of Industrial Research, shares the highlights of a new report on the industrial sector's growth.

Codes and Standards | Apr 4, 2022

Construction of industrial space continues robust growth

Construction and development of new industrial space in the U.S. remains robust, with all signs pointing to another big year in this market segment

Reconstruction & Renovation | Mar 28, 2022

Is your firm a reconstruction sector giant?

Is your firm active in the U.S. building reconstruction, renovation, historic preservation, and adaptive reuse markets? We invite you to participate in BD+C's inaugural Reconstruction Market Research Report.