According to the year-end Lodging Econometrics (LE) Construction Pipeline Trend Report for Canada, analysts at LE state that Canada’s hotel construction pipeline ended 2021’s fourth quarter at 262 projects/35,325 rooms. The pipeline is down a mere 3% by projects and up 2% by rooms, year-over-year (YOY).

At the close of 2021, projects under construction stand at 62 projects/8,100 rooms. Projects scheduled to start construction in the next 12 months stand at 85 projects/10,536 rooms and projects in the early planning stage are at an all-time high at Q4 with 115 projects/16,689 rooms, a 15% increase by projects and 14% by rooms YOY.

Leisure and business travel has increased in recent months thanks to the holiday season and the country’s COVID booster rollout program, that was executed more quickly than expected.

Ontario continues to lead Canada’s construction pipeline in Q4, reaching the province’s highest project count since Q4‘19, with 154 projects/19,818 rooms. Ontario accounts for 59% of the projects and 56% of the rooms in Canada’s total pipeline. British Columbia follows with 37 projects/5,675 rooms, then Alberta with 24 projects/3,739 rooms, and Quebec with 18 projects/2,481 rooms.

Markets with the most projects in the pipeline continue to be led by Toronto, at an all-time high, with 65 projects/9,621 rooms. Toronto, alone, has 25% of all the projects in Canada’s construction pipeline. Distantly following are Vancouver with 14 projects/2,016, then Niagara Falls with 13 projects/2,341 rooms, Montreal with 13 projects/1,956 rooms, and Ottawa with 10 projects/1,694 rooms. These top five cities, combined, account for 44% of the projects and 50% of the rooms in Canada’s total pipeline.

The top hotel franchise company in Canada's construction pipeline at Q4‘21 is Marriott International, at all-time high of 71 projects/8,890 rooms. Hilton Worldwide follows closely with 65 projects/7,870 rooms, then InterContinental Hotels Group (IHG) with 47 projects/4,732 rooms. These three companies claim 70% of the projects and 61% of the rooms in the country’s total construction pipeline.

The top brands in Canada’s pipeline are Hampton by Hilton, with 26 projects/2,946 rooms and IHG’s Holiday Inn Express, with 24 projects/2,461 rooms. Next is Marriott’s TownePlace Suites, at record counts, with 17 projects/1,817 rooms. This is followed by Hilton’s Home2Suites with 16 projects/1,706 rooms, then Marriott’s Fairfield Inn brand with 16 projects/1,533 rooms.

Canada had 35 new hotels with 3,742 rooms open in 2021 at a growth rate of 1.1%. In 2022, the country is forecast to have a growth rate of 1.2% with 38 new hotels/4,251 rooms expected to open. LE is forecasting a slight increase in Canada’s growth rate to 1.3% in 2023 and expects 41 new hotels/4,632 rooms to open by year-end.

Related Stories

Market Data | Oct 31, 2016

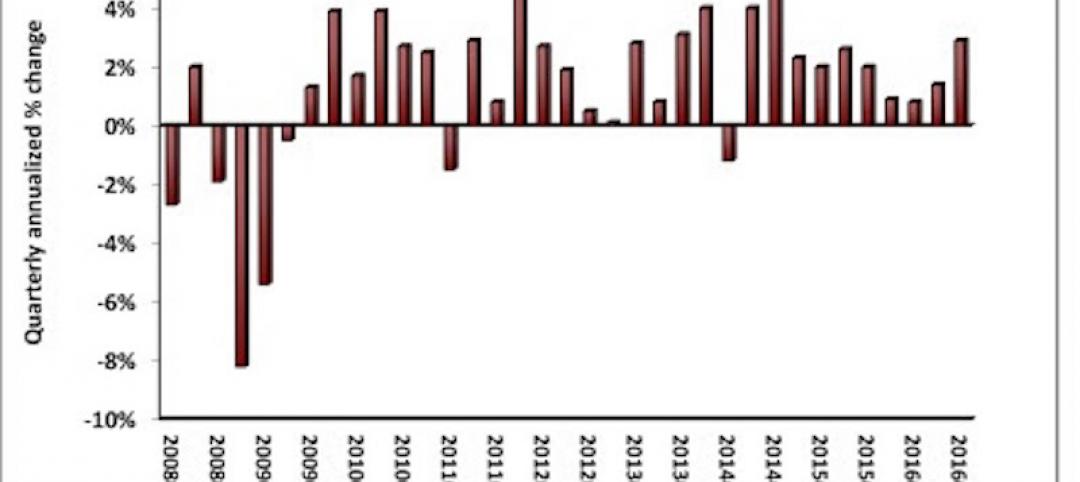

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.

Industry Research | Sep 27, 2016

Sterling Risk Sentiment Index indicates risk exposure perception remains stable in construction industry

Nearly half (45%) of those polled say election year uncertainty has a negative effect on risk perception in the construction market.