Contractors continue to face a shortage of building materials like lumber and steel, while cost fluctuations for the building products are having increasing impact on business, according to second quarter data from the U.S. Chamber of Commerce Commercial Construction (Index). This quarter, 84% of contractors are facing at least one material shortage. Almost half (46%) of contractors say less availability of building products has been a top concern lately, up from 33% who said the same last quarter.

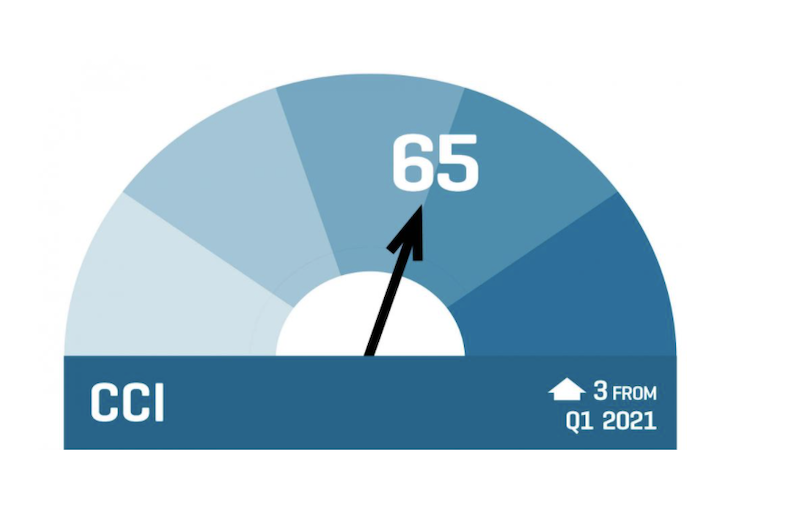

Despite the materials challenges, the overall Index score rose three points to 65 (its highest reading since a score of 74 in Q1 2020 ahead of the pandemic) and contractors are optimistic on outlook for revenue expectations, new business

— 89% of contractors report a moderate to high level of confidence in new business opportunities in the next 12 months, up from 86% in Q1. Those indicating a high level of confidence jumped 10 points to 34% from last quarter.

— Over half (52%) of contractors say they will hire more employees in the next six months, up from 46% in Q1.

— More contractors (39%) expect

— For the first time in a year, the percentage of contractors planning to spend more on tools and equipment in the next six months (44%) is higher than those who say they will not spend more (42%).

“Businesses are experiencing a great resurgence as vaccines allow the economy to fully reopen. Rising optimism from the commercial construction industry reflects what we’re seeing across the broader economy,” said U.S. Chamber of Commerce Executive Vice President and Chief Policy Officer Neil Bradley. “However, contractors continue to face challenges navigating materials shortages and

Materials Shortages Worsen

Most (84%) contractors say they face at least one material shortage, up from 71% in Q1. One in three (33%) are experiencing a shortage in wood/lumber, and 29% are seeing a shortage of steel. Of those contractors experiencing shortages, 46% say they are having a high impact on projects, up from 20% saying the same in Q1.

Additionally, almost all (94%) contractors say cost fluctuations are having a moderate to high impact on their business, up 12 percentage points from Q1 and up 35 points year-over-year. Wood/lumber and steel are the products of highest concern.

Contractors Face Worker Shortage Crisis

In the midst of a deepening workforce crisis, finding skilled labor continues to be a challenge for contractors. This quarter, 88% report moderate to high levels of difficulty finding skilled workers, of which, nearly half (45%) report a high level of difficulty. Of those who reported difficulty finding skilled labor, over a third (35%) have turned down work because of skilled labor shortages.

Most (87%) contractors also report a moderate to high level of concern about the cost of skilled labor. Of those who expressed concern, 64% say the cost has increased over the past six months, and more than three-quarters (77%) expect it to continue to increase over the next year.

Trade and Tariff Concerns are Up

This quarter, contractors expressed increasing concern about the potential effect of tariffs and trade wars on access to materials over the next three years.

More (45%) say steel and aluminum tariffs will have a high to very-high degree of impact, up from 35% in Q1. Forty percent now say new construction material and equipment tariffs will have a high to very-high degree of impact, up from 29% in Q1. And 30% expect high impacts from trade conflicts with other countries, up from 19% in Q1.

About the Index

The U.S. Chamber of Commerce Commercial Construction Index is a quarterly economic index designed to gauge the outlook for, and resulting confidence in, the commercial construction industry. The Index comprises three leading indicators to gauge confidence in the commercial construction industry, generating a composite Index on the scale of 0 to 100 that serves as an indicator of health of the contractor segment on a quarterly basis.

The Q2 2021 results from the three key drivers are:

— Revenue: Contractors’ revenue expectations over the next 12 months increased to 61 (up four points from Q1).

— New Business Confidence: The overall level of contractor confidence increased to 62 (up three points from Q1).

— Backlog: The ratio of average current to ideal backlog rose three points to 72 (up three points from Q1).

The research was developed with Dodge Data & Analytics (DD&A), the leading provider of insights and data for the construction industry, by surveying commercial and institutional contractors.

Visit www.

Related Stories

Contractors | Sep 12, 2023

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of August 2023

Associated Builders and Contractors' Construction Backlog Indicator declined to 9.2 months in August, down 0.1 month, according to an ABC member survey conducted from Aug. 21 to Sept. 6. The reading is 0.5 months above the August 2022 level.

Contractors | Sep 11, 2023

Construction industry skills shortage is contributing to project delays

Relatively few candidates looking for work in the construction industry have the necessary skills to do the job well, according to a survey of construction industry managers by the Associated General Contractors of America (AGC) and Autodesk.

Market Data | Sep 6, 2023

Far slower construction activity forecast in JLL’s Midyear update

The good news is that market data indicate total construction costs are leveling off.

Giants 400 | Sep 5, 2023

Top 80 Construction Management Firms for 2023

Alfa Tech, CBRE Group, Skyline Construction, Hill International, and JLL top the rankings of the nation's largest construction management (as agent) and program/project management firms for nonresidential buildings and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Sep 5, 2023

Top 150 Contractors for 2023

Turner Construction, STO Building Group, DPR Construction, Whiting-Turner Contracting Co., and Clark Group head the ranking of the nation's largest general contractors, CM at risk firms, and design-builders for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Market Data | Sep 5, 2023

Nonresidential construction spending increased 0.1% in July 2023

National nonresidential construction spending grew 0.1% in July, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.08 trillion and is up 16.5% year over year.

Giants 400 | Aug 31, 2023

Top 35 Engineering Architecture Firms for 2023

Jacobs, AECOM, Alfa Tech, Burns & McDonnell, and Ramboll top the rankings of the nation's largest engineering architecture (EA) firms for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.