Commercial construction is in high demand across the country and contractors are confident in the trajectory of the industry, according to the USG + U.S. Chamber of Commerce Commercial Construction Index (‘Index’), that launched recently. Nearly all contractors surveyed – 96 percent – expect revenues to grow or remain stable this year compared to 2016, with 40 percent expecting an increase and only 3 percent expecting a decrease in revenue.

The Index is a new quarterly economic indicator designed to gauge what drives the commercial construction industry and its leaders, including specific issues like backlog of work, new business pipeline, revenue projections, workforce issues, and access to financing. Given the sector’s importance to the U.S. economy and the outsized role it could play in years to come, the data contained in the Index will be vital to better understanding trends, challenges and opportunities. The research was developed with Dodge Data & Analytics (DD&A), the leading provider of insights and data for the construction industry, by surveying commercial and institutional contractors.

“This first-of-its-kind Index was born out of a need to understand the issues that affect commercial construction. The Index will deliver critical insights into the future health of the industry,” said Jennifer Scanlon, president and chief executive officer of USG Corporation. “USG is committed to providing solutions for our customers in order to help the entire industry make strong contributions to the U.S. economy. Through the Index we are able to identify areas of strength and pinpoint areas of improvement where industry leaders must focus.”

Two-thirds (66 percent) of contractors said they expect to employ more workers in the next six months, indicating growth in a sector that employs approximately 3 million Americans. But 61 percent of Index respondents reported difficultly finding skilled workers. The contractors reported the biggest shortages in the concrete, interior finishes/millwork, masonry, electrical and plumbing trades.

“The commercial construction industry is a vital engine for the American economy,” said Tom Donohue, president and CEO of the U.S. Chamber. “The projected growth uncovered in this research is good news for employers and workers, but there is reason for concern in the lack of qualified talent available in vital specialties. To get our economy growing to its full potential, we must ensure that we have a workforce that is ready to fill the available jobs. Each quarter, this first-of-its-kind research will make us smarter about future challenges and inform solutions for our country’s leaders.”

The report looks at the results of three leading indicators – backlog levels, new business opportunities and revenue forecasts – to generate a composite index on a scale of 0-100 that serves as an indicator of health for the contractor segment on a quarterly basis. The Q2 2017 composite index score was 76, representing continued health in the sector. This composite score is up two points from a 74 in the Q1 survey, driven primarily by a bump in the ratio between actual and ideal backlog. New business and revenue results also saw slight increases quarter-over-quarter.

The composite scores from the three drivers of confidence were:

Backlog: 81, up four points in Q2 over Q1

Contractors’ current average backlog levels represent 81 percent of their ideal backlog levels, up from 77 percent in Q1. On average, contractors currently hold 9.9 months of backlog, while the ideal amount is 12 months.

New Business: 77, up two points in Q2

Nearly all contractors continue to report high or moderate confidence in the market. Well over half of contractors (59 percent) reported high confidence in new business over the next 12 months (up from 51 percent in Q1), indicating a shift to higher levels of confidence among some respondents.

Revenues: 71, up two points in Q2

An overwhelming 96 percent of contractors expect revenues to grow or remain stable in 2017 over 2016. Of those expecting revenue increases, the actual percentage of expected increases varies widely. Forty percent expect revenue increases of 7 percent or more in the next 12 months.

The Index findings are compiled using survey results from contractors within a DD&A panel of more than 2,700 decision makers from across key facets of the commercial construction industry. This first public report was developed using research from previous quarters, which puts into context the state of contractor sentiment in the U.S. building industry.

Related Stories

Market Data | May 1, 2017

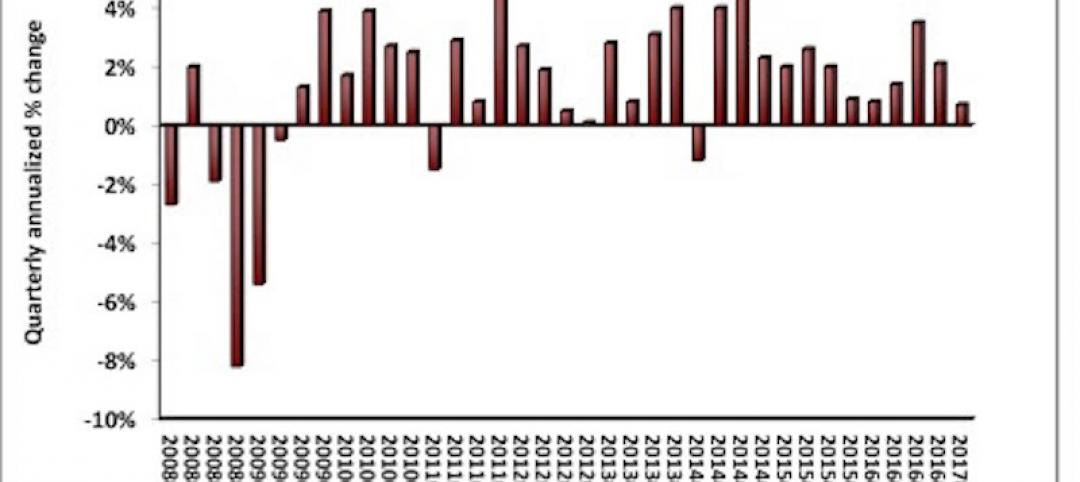

Nonresidential Fixed Investment surges despite sluggish economic in first quarter

Real gross domestic product (GDP) expanded 0.7 percent on a seasonally adjusted annualized rate during the first three months of the year.

Industry Research | Apr 28, 2017

A/E Industry lacks planning, but still spending large on hiring

The average 200-person A/E Firm is spending $200,000 on hiring, and not budgeting at all.

Architects | Apr 27, 2017

Number of U.S. architects holds steady, while professional mobility increases

New data from NCARB reveals that while the number of architects remains consistent, practitioners are looking to get licensed in multiple states.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

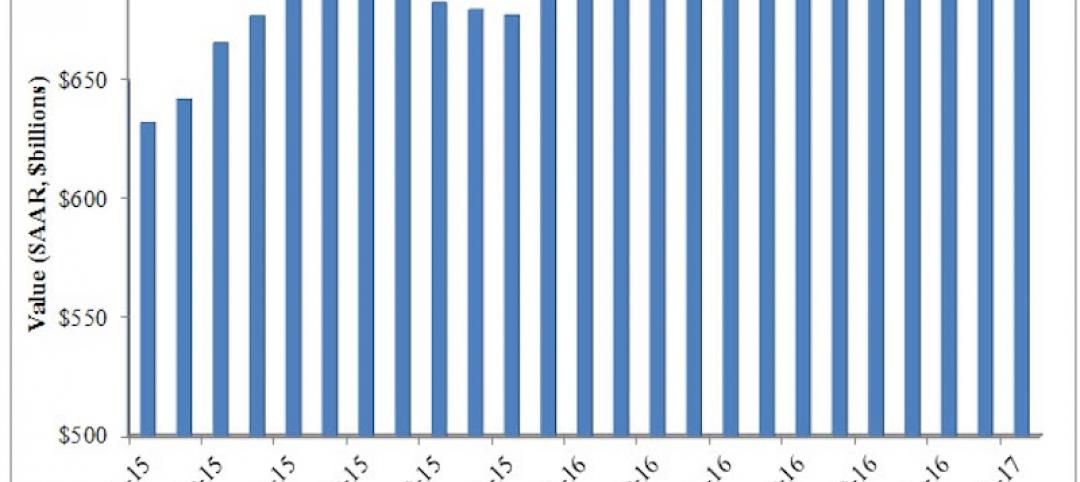

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Industry Research | Mar 24, 2017

The business costs and benefits of restroom maintenance

Businesses that have pleasant, well-maintained restrooms can turn into customer magnets.

Industry Research | Mar 22, 2017

Progress on addressing US infrastructure gap likely to be slow despite calls to action

Due to a lack of bipartisan agreement over funding mechanisms, as well as regulatory hurdles and practical constraints, Moody’s expects additional spending to be modest in 2017 and 2018.

Industry Research | Mar 21, 2017

Staff recruitment and retention is main concern among respondents of State of Senior Living 2017 survey

The survey asks respondents to share their expertise and insights on Baby Boomer expectations, healthcare reform, staff recruitment and retention, for-profit competitive growth, and the needs of middle-income residents.

Industry Research | Mar 14, 2017

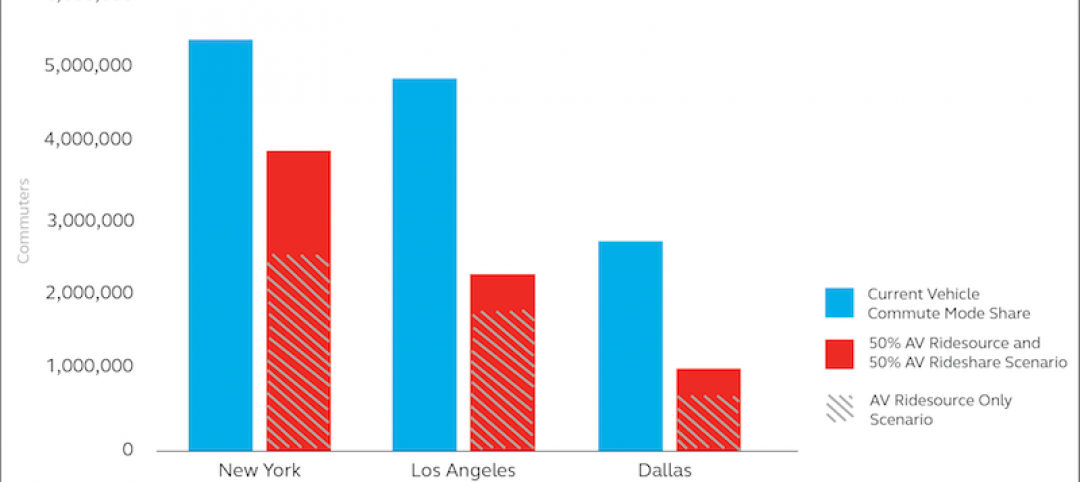

6 ways cities can prepare for a driverless future

A new report estimates 7 million drivers will shift to autonomous vehicles in 3 U.S. cities.