Overcapacity in global iron ore production was a major factor in keeping construction costs low through the first four months of 2015. And for the first time in years, subcontractor labor costs showed signs of softening.

Those are two key findings in the latest assessment of current and future pricing from IHS, the Englewood, Colo.-based market analysis firm.

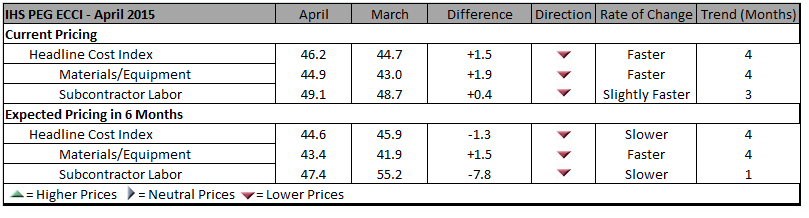

IHS derives its monthly Cost Index from information it receives from member procurement executives working for several of the world’s largest construction and engineering companies, including AECOM and Bechtel. It breaks down those data into current pricing trends and projections for six months forward.

In April, its Cost Index was 46.2, a bit higher than 44.7 in March, but still below what IHS would consider a “neutral” reading. Its sub index for Materials/Equipment costs in April was 44.9 compared to 43.0 in March. And the April sub index for Subcontractor Labor costs stood at 49.1, compared to 48.7 in March.

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

IHS notes that eight of 12 construction components it tracks registered falling prices in April, led by carbon steel pipe and fabricated structural steel. Both are victims of “bloated capacity, weak profit growth, and lackluster demand,” explains John Anton, IHS’s Director of Steel Services. Iron ore companies that, in response to demand from China’s steel industry, have initiated massive projects whose capacity, so far, “is far ahead of demand,” and is holding prices down.

Anton adds that while the iron ore market may have some ostensible similarities to the recent decline of crude oil prices, what’s different is that iron ore producers have shown no inclinations toward cutting production to match demand. (IHS points out that three quarters of China’s mines are losing money.)

IHS also notes that several global construction and engineering firms, particularly those in the oil and gas sectors, have been taking a “wait and see” approach to investing in larger capital projects. “The capex environment has yet to thaw,” asserts Mark Eisinger, IHS’s senior economist.

While some markets, like the U.S. South, are still experiencing shortages in skilled subcontractor labor, manpower costs have been receding. For the third consecutive month, the U.S. did not register higher month-to-month labor costs in April. And for the first time in this survey’s history, projections about labor costs over the next six months are below the neutral mark. The six-month cost index for subcontractor labor fell to 47.4 in April, compared to 55.2 in March.

The forward-looking index for materials and equipment, at 43.4 April, rose from March’s record low of 41.9, even as 10 of 12 components showed falling price expectations.

Related Stories

Designers | Oct 19, 2022

Architecture Billings Index moderates but remains healthy

For the twentieth consecutive month architecture firms reported increasing demand for design services in September, according to a new report today from The American Institute of Architects (AIA).

Building Team | Oct 18, 2022

Brasfield & Gorrie chairman’s home vandalized by anti-development activists

Activists vandalized the home and vehicles of Miller Gorrie, chairman of Birmingham-based Brasfield & Gorrie, in protest of a planned $90 million, 85-acre police, fire and public safety training center in Atlanta.

Mixed-Use | Oct 18, 2022

Mixed-use San Diego tower inspired by coastal experience and luxury travel

The new 525 Olive mixed use San Diego tower was inspired by the coastal experience and luxury travel.

University Buildings | Oct 18, 2022

A carbon-neutral-ready university campus opens in Hong Kong

In early September, the Hong Kong University of Science and Technology (HKUST) officially opened its new, KPF-designed campus in Nansha, Guangzhou (GZ).

Market Data | Oct 17, 2022

Calling all AEC professionals! BD+C editors need your expertise for our 2023 market forecast survey

The BD+C editorial team needs your help with an important research project. We are conducting research to understand the current state of the U.S. design and construction industry.

Codes and Standards | Oct 17, 2022

Ambitious state EV adoption goals put pressure on multifamily owners to provide chargers

California’s recently announced ban on the sale of new gas-powered vehicles starting in 2035—and New York’s recent decision to follow suit—are putting pressure on multifamily property owners to install charging stations for tenants.

Contractors | Oct 17, 2022

Interior Investments, LLC, joins PARIC Holdings family of companies

PARIC Holdings announced that Interior Investments, LLC, has joined the PARIC Holdings family of companies. This strategic collaboration will leverage the strengths and expertise of each organization to deliver a comprehensive suite of turnkey services to best support their customers.

Justice Facilities | Oct 17, 2022

San Antonio’s new courthouse aims to provide safety and security while also welcoming the public

The San Antonio Federal Courthouse, which opened earlier this year, replaces a courthouse that had been constructed as a pavilion for the 1968 World’s Fair.

Market Data | Oct 14, 2022

ABC’s Construction Backlog Indicator Jumps in September; Contractor Confidence Remains Steady

Associated Builders and Contractors reports today that its Construction Backlog Indicator increased to 9.0 months in September, according to an ABC member survey conducted Sept. 20 to Oct. 5.

| Oct 13, 2022

Boston’s proposed net-zero emissions code has developers concerned

Developers have raised serious concerns over a proposed new energy code by the City of Boston that would require newly constructed buildings over 20,000 sf to immediately hit net-zero emissions goals.