Gilbane has released its Spring 2014 edition of the periodic report "Construction Economics: Market Conditions in Construction" (download the full report).

Among the findings from the Executive Summary:

CONSTRUCTION GROWTH IS LOOKING UP

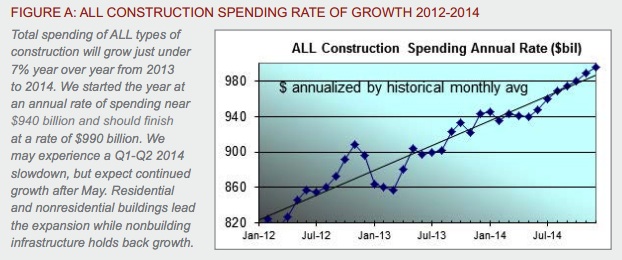

- Construction Spending for 2014 will finish the year 6.6% higher than 2013. Nonresidential buildings will contribute substantially to the growth.

- The Architecture Billings Index (ABI) in 2013 dropped below 50 in April, November and December briefly, indicating declining workload. Overall the ABI portrays a good leading indicator for future new construction work.

- Selling price data for 2013 shows contractors adding to their margins.

- Construction jobs grew by 156,000 in 2013, less than anticipated. However, hours worked also grew by 3%, the equivalent of another 150,000+ jobs.

SOME ECONOMIC FACTORS ARE STILL NEGATIVE

- We are experiencing a slight slowdown in construction spending that could last through May, influenced by a slight dip in nonresidential buildings and a brief flattening in residential, but more so by a steep decline in nonbuilding infrastructure spending. The monthly rate of spending for nonbuilding infrastructure may decline by 10% through Q3 2014.

- The construction workforce and hours worked is still 22% below the 2006 peak. At peak average growth rates, it will take a minimum of five more years to return to previous peak levels.

- Construction volume is 23% below peak inflation adjusted spending, which was almost constant from 2000 through 2006. At average peak growth rates of 8% per year, and factoring out inflation to get real volume growth, it will take eight more years to regain previous peak volume levels.

- As workload expands in the next few years, a shortage of available skilled workers may have a detrimental effect on cost, productivity and the ability to readily increase construction volume.

THE EFFECTS OF GROWTH

- Construction spending during the first five months of 2013 declined from the rate of spending in Q4 2012. Growth has been inconsistent, even in the booming residential sector, which has seen recent declines. We see more consistent growth in 2014 for buildings.

- As spending continues to increase, contractors gain more ability to pass along costs and increase margins. The growth in contractor margins slowed since last year. However, expected increases in volume should reverse that in 2014.

- ENR’s Third Quarter 2013 Cost Report shows general purpose and material cost indices increased on average about 2% to 2.5% year over year. However, selling price indices increased 4% on average. The difference between these indices is increased margins.

IMPACT OF RECENT EVENTS

- There are several reasons why spending is not rapidly increasing: public sector construction remains depressed as sequestration continues; the government is spending less on schools and infrastructure; lenders are just beginning to loosen lending criteria; consumers are still cautious about increasing debt load, including the consumers’ share of public debt and we may be constrained by a skilled labor shortage.

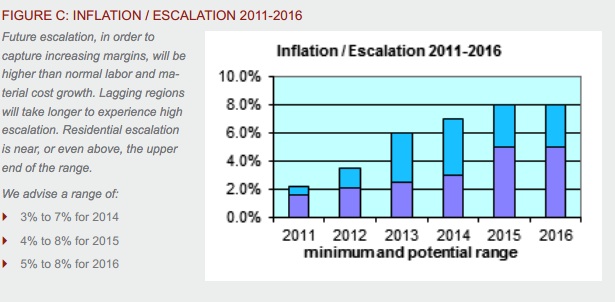

- Supported by overall positive growth trends for year 2014, Gilbane expects margins and overall escalation to climb more rapidly than we have seen in six years.

- Growth in nonresidential buildings and residential construction in 2014 will lead to more significant labor demand, resulting in labor shortages and productivity losses. Margins regained a positive footing in 2012 and extended those gains in 2013. Expect margins to grow stronger in 2014. When activity picks up in all sectors, escalation will begin to advance rapidly.

Click here to download the complete report and a list of data sources.

ABOUT THIS REPORT

Gilbane Inc. is a full service construction and real estate development company, composed of Gilbane Building Company and Gilbane Development Company. The company (www.gilbaneco.com) is one of the nation’s largest construction and program managers providing a full slate of facilities related services for clients in education, healthcare, life sciences, mission critical, corporate, sports and recreation, criminal justice, public and aviation markets. Gilbane has more than 50 offices worldwide, with its corporate office located in Providence, Rhode Island. The information in this report is not specific to any one region.

Related Stories

| Aug 11, 2010

Gensler, HOK, HDR among the nation's leading reconstruction design firms, according to BD+C's Giants 300 report

A ranking of the Top 100 Reconstruction Design Firms based on Building Design+Construction's 2009 Giants 300 survey. For more Giants 300 rankings, visit http://www.BDCnetwork.com/Giants

| Aug 11, 2010

Gensler, Arup, HOK among the largest office sector design firms

A ranking of the Top 100 Office Design firms based on Building Design+Construction's 2009 Giants 300 survey. For more Giants 300 rankings, visit http://www.BDCnetwork.com/Giants

| Aug 11, 2010

Callison strengthens retail design presence with RYA acquisition

Callison LLC on June 1 acquired RYA Design Consultancy, a Dallas-based retail architecture and design firm with offices in New York City. The new “Callison RYA Studio” will merge staff and clients into Callison ’s existing retail practice at their Dallas and New York offices.

| Aug 11, 2010

Prism-shaped design unveiled for five-star hotel in Saudi Arabia

Goettsch Partners has been commissioned by Saudi Oger Ltd. to design a new five-star, 214-key business hotel in the King Abdullah Financial District in Riyadh, Saudi Arabia. As a design-build assignment, Saudi Oger is serving as the contractor, selected by developer Rayadah Investment Company. The project is sited on Parcel 1.08, one of the first 10 parcels currently under development in the massive new master-planned district.

| Aug 11, 2010

Construction Specifications Institute to end support of MasterFormat 95 on December 31, 2009

The Construction Specifications Institute (CSI) announced that the organization will cease to license and support MasterFormat 95 as of December 31, 2009. The CSI Board of Directors voted to stop licensing and supporting MasterFormat 95 during its June 16, 2009, meeting at the CSI Annual Convention in Indianapolis.

| Aug 11, 2010

Gensler among eight teams named finalists in 'classroom of the future' design competition

Eight teams were recognized today as finalists of the 2009 Open Architecture Challenge: Classroom. Finalists submitted designs ranging from an outdoor classroom for children in inner-city Chicago, learning spaces for the children of salt pan workers in India, safe spaces for youth in Bogota, Colombia and a bamboo classroom in the Himalayan mountains.

| Aug 11, 2010

F&S Partners merges with SmithGroup

F&S Partners, a Dallas architecture firm specializing in the design of educational, recreational, and religious projects, has merged with SmithGroup, a top 10 U.S. architecture/engineering firm. The 40-person office in Dallas will carry the name SmithGroup/F&S.