Prices for inputs to construction fell 0.5% in August but are 8.1% higher than at the same time one year ago, according to an Associated Builders and Contractors analysis of Bureau of Labor Statistics data released today. Nonresidential construction input prices fell 0.4% in August but are up 8.3% year-over-year. Softwood lumber prices plummeted 9.6% in August yet are up 5% on a yearly basis (down from a 19.5% increase year-over-year in July).

“Stakeholders will be tempted to look upon this month’s inputs to the construction Producer Price Index report as evidence that the cycle of rapidly rising prices is nearing an end,” said ABC Chief Economist Anirban Basu. “Prices of key inputs have been high for quite some time, which would tend to induce a larger supply of these items and, in turn, moderate prices.

“Some may also conclude that ongoing progress in trade negotiations with nations including Mexico and Canada has helped to moderate input prices. Still others might point to growing economic turmoil in nations like Turkey and Argentina. Economists would also note the likely impact of a strong U.S. dollar on import and commodity prices. While all of these are potential explanations, another possibility is that the August data are largely statistical aberrations. Metal prices continue to move higher on a monthly basis, with recently enacted tariffs representing a likely explanation.

“Softwood lumber, the subject of an ongoing trade dispute with the Canadians, experienced a significant dip in price on a monthly basis,” said Basu. “The price of softwood may have fallen in response to a weakening single-family residential construction market, as home builders have been wrestling with a combination of labor shortages, higher land prices and weakening demand due to higher mortgage rates.

“In the final analysis, the falling input prices trend likely won’t continue,” said Basu. “The economy is still strong, and ABC’s Construction Backlog Indicator remains elevated in both public and private construction segments. Inflation expectations have shifted, with purchasers of construction services now anticipating price increases and therefore more willing to accommodate them. Moreover, issues related to tariffs and trade wars persist. Accordingly, estimators and construction companies continue to consider the likelihood of additional input price increases for the balance of 2018 and into 2019.”

Related Stories

Contractors | Sep 12, 2023

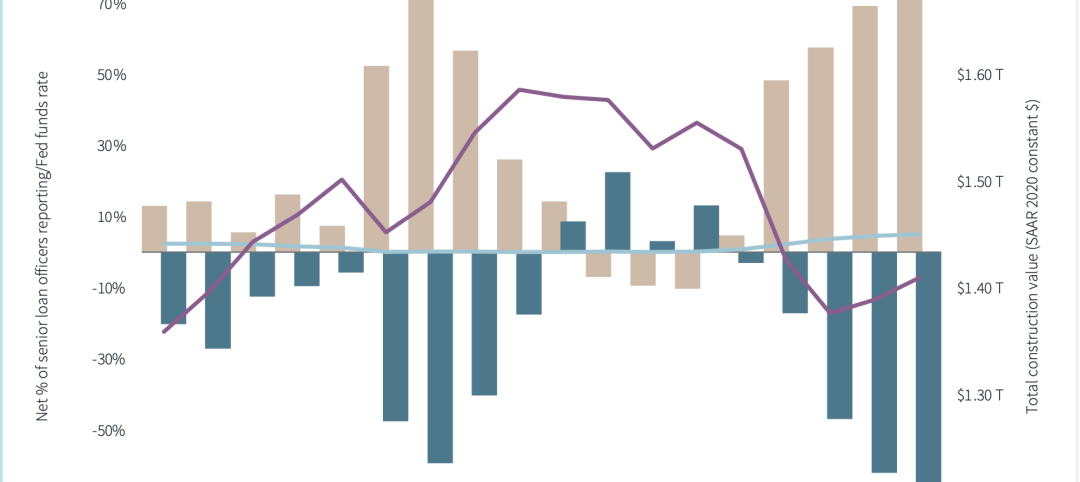

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of August 2023

Associated Builders and Contractors' Construction Backlog Indicator declined to 9.2 months in August, down 0.1 month, according to an ABC member survey conducted from Aug. 21 to Sept. 6. The reading is 0.5 months above the August 2022 level.

Contractors | Sep 11, 2023

Construction industry skills shortage is contributing to project delays

Relatively few candidates looking for work in the construction industry have the necessary skills to do the job well, according to a survey of construction industry managers by the Associated General Contractors of America (AGC) and Autodesk.

Market Data | Sep 6, 2023

Far slower construction activity forecast in JLL’s Midyear update

The good news is that market data indicate total construction costs are leveling off.

Giants 400 | Sep 5, 2023

Top 80 Construction Management Firms for 2023

Alfa Tech, CBRE Group, Skyline Construction, Hill International, and JLL top the rankings of the nation's largest construction management (as agent) and program/project management firms for nonresidential buildings and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Sep 5, 2023

Top 150 Contractors for 2023

Turner Construction, STO Building Group, DPR Construction, Whiting-Turner Contracting Co., and Clark Group head the ranking of the nation's largest general contractors, CM at risk firms, and design-builders for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Market Data | Sep 5, 2023

Nonresidential construction spending increased 0.1% in July 2023

National nonresidential construction spending grew 0.1% in July, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.08 trillion and is up 16.5% year over year.

Giants 400 | Aug 31, 2023

Top 35 Engineering Architecture Firms for 2023

Jacobs, AECOM, Alfa Tech, Burns & McDonnell, and Ramboll top the rankings of the nation's largest engineering architecture (EA) firms for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.