In the first half of 2024, construction costs stabilized. And through the remainder of this year, total cost growth is projected to be modest, and matched by an overall increase in construction spending.

That prediction can be found in JLL’s 2024 Midyear Construction Update and Reforecast, released today. JLL bases its market analyses on insights gleaned from its global team of more than 550 research professionals who track economic and property trends and forecast future conditions in over 60 countries.

The Update acknowledges that the industry has been adjusting to new patterns of demand, as not all sectors are performing equally well. Interest in projects in general has increased, lending regulations are not tightening, and spending is up more than originally anticipated.

Still, the trajectory of interest rates “continues to elude forecasters,” observes JLL, “making ‘higher for longer’ the correct operating paradigm.” Yet despite financial constraints, JLL expects cost growth and development to continue. Stakeholders need to account for maturing debt, lease expirations, and emerging global advantages as they navigate the realities of sustained higher interest rates and varied local outcomes.

One area of opportunity for AEC firms, under these circumstances, is resilient and sustainable design and construction, says JLL.

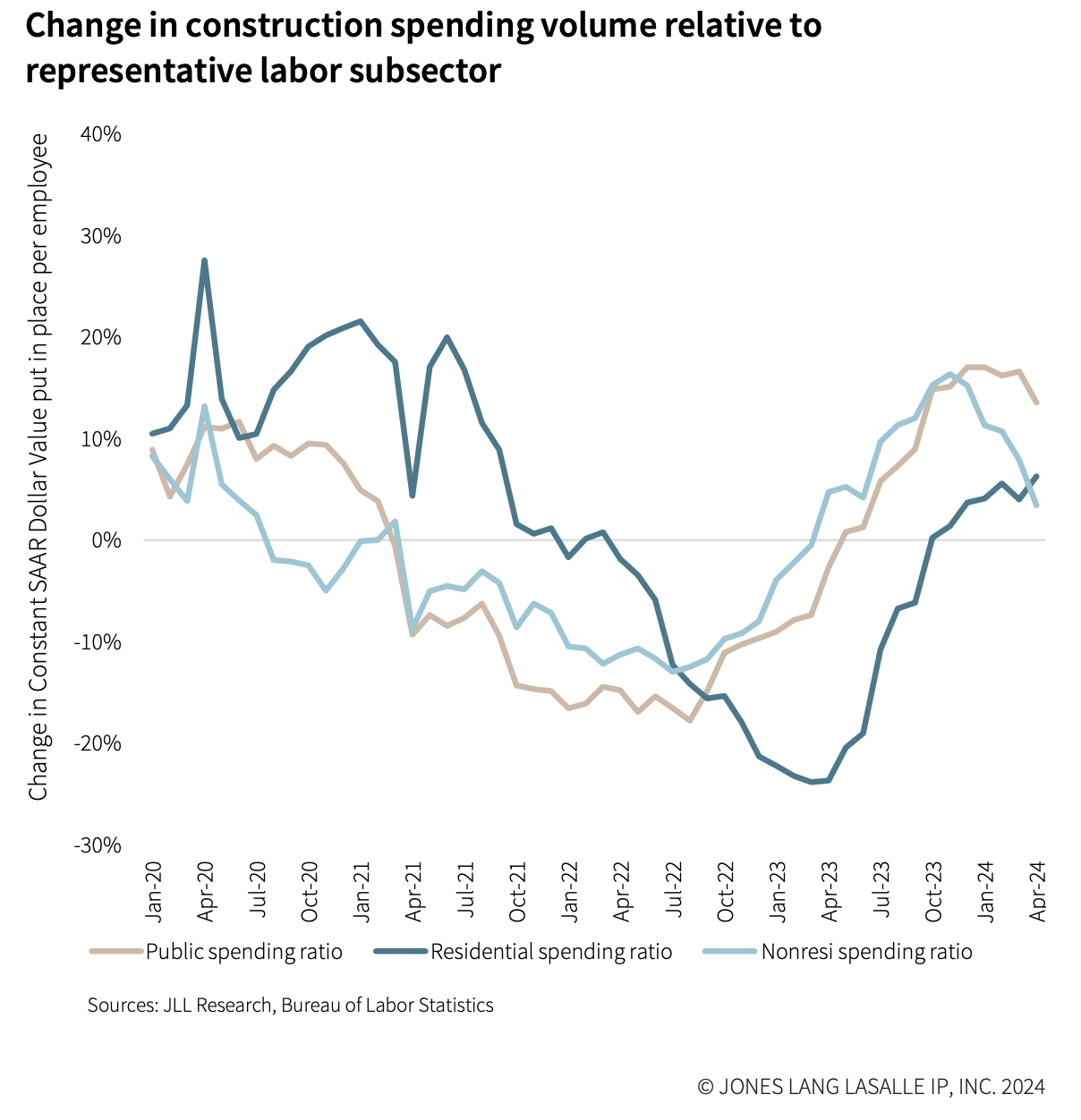

Spending is outpacing employment availability

With these positive outlooks, construction employment has risen, along with compensation. Labor costs driven by limited availability continue to provide a growth floor for broader industry costs. JLL states that its predictions of wage growth at moderately higher than historical rates remain unchanged.

This is because construction spending has been outpacing employment. “Relative strain in production value required per employee is returning to pre-pandemic points [but] with a very different workforce, and remains heavily concentrated in select metros,” JLL states.

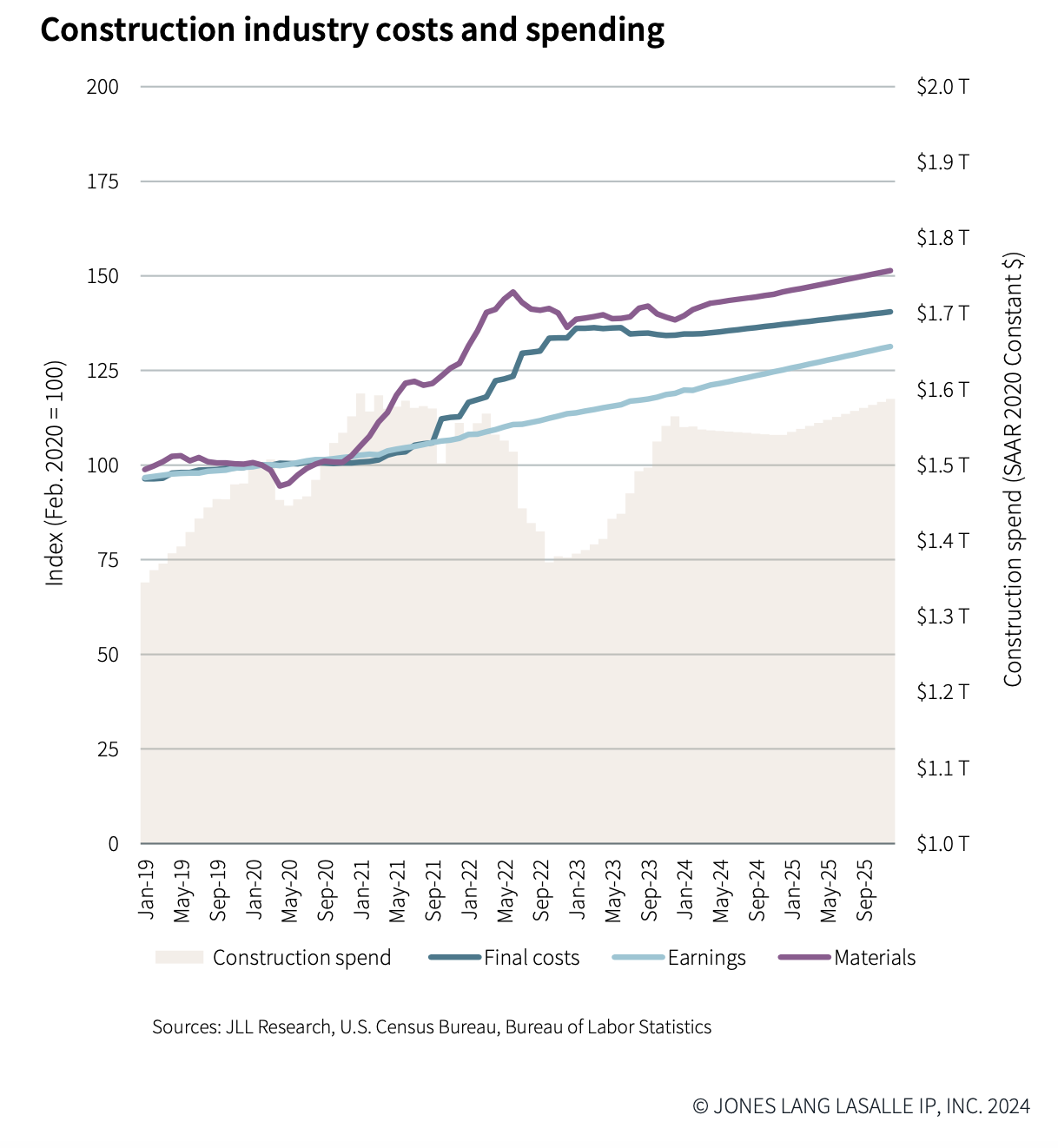

While overall growth has been restrained to average below expectations, volatility persists, notably on the cost of materials. Demand for finished goods remains high, especially for MEP products as more sectors electrify and upgrade their operating systems.

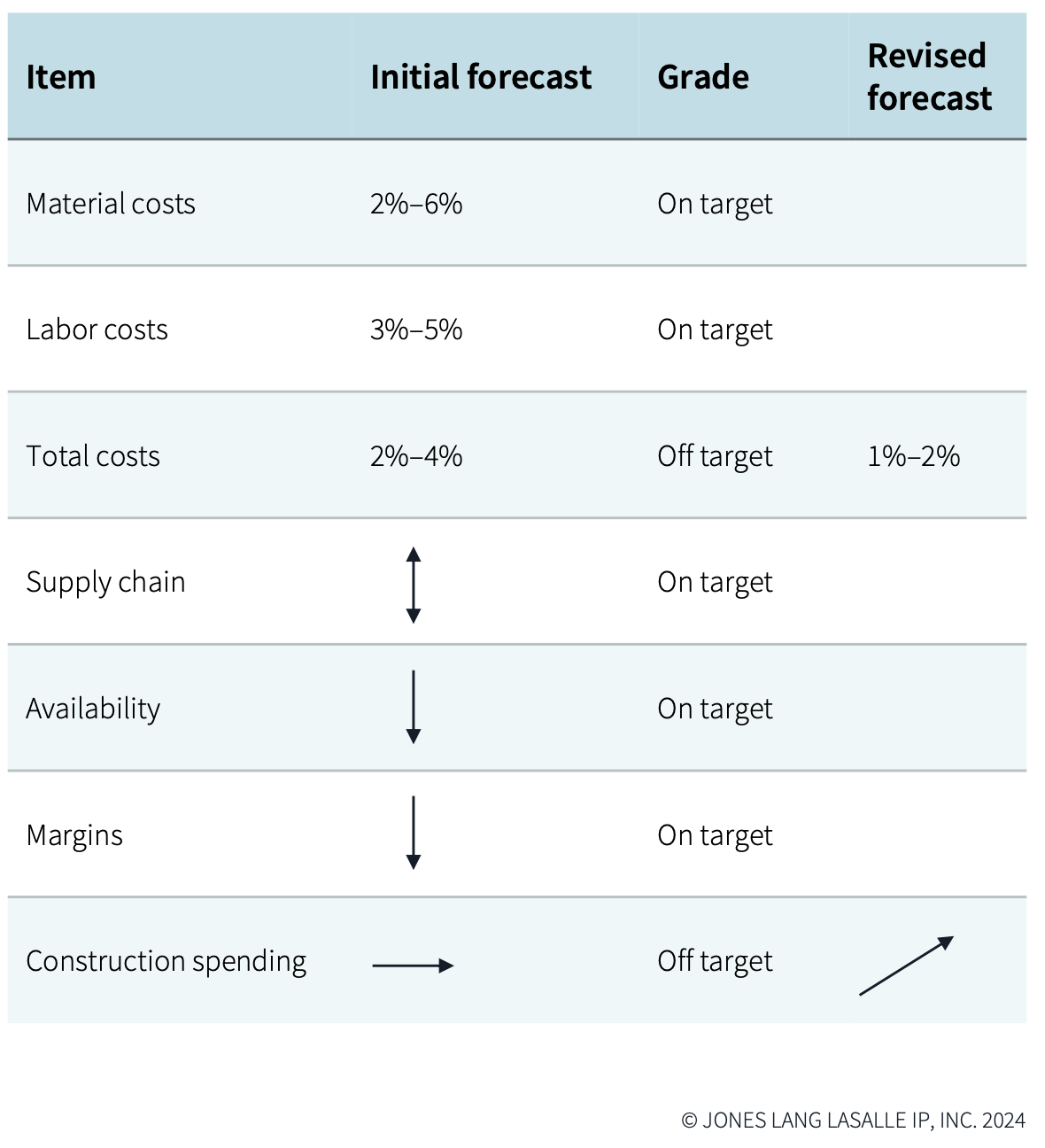

Staples of demand are changing and, with them, expectations for price moderation and normal market behavior. For example, bid prices for staple materials such as metals and concrete are at their lowest average monthly movement since 2020. JLL observes that price stability reflects efforts to develop backlogs and secure work and margins. But with global events being so unpredictable, this current period of price stability, says JLL, is transient “and likely short-lived.”

Big question: continued infrastructure investment

JLL believes that market participants, namely developers, suppliers, and AEC firms, are going to hold their current growth pace over the short term. Its Update advises stakeholders to engage the nuances of local markets and design demands “as early as possible” to determine market direction and to navigate disruptions.

So far, firms have been able to compress their margins, mainly because material costs have trended lower than expected, which in turn has allowed for higher-than-anticipated construction spending. But labor challenges continue unabated and are expected to exert pressure on costs into 2025 and beyond.

Consequently, JLL has revised some of its forecasts for the remainder of 2024, most prominently that total costs would increase just 1-2% for the year, and that construction spending (which JLL previously thought would be flat) will increase.

JLL notes, too, that aggregate materials, currently on the low end of price increases, might experience more volatility. JLL also states that anticipating spending increases—and the price floor that such demand would set—will depend on continued public investment in infrastructure and other construction projects.

Related Stories

Market Data | Oct 31, 2016

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.

Industry Research | Sep 27, 2016

Sterling Risk Sentiment Index indicates risk exposure perception remains stable in construction industry

Nearly half (45%) of those polled say election year uncertainty has a negative effect on risk perception in the construction market.