The office, education, amusement and recreation, manufacturing, and transportation sectors are expected to be the impetus behind a projected 3% increase in spending on engineering and construction in the United States, according to the recently released 2019 FMI Overview, which features the management consulting and investment banking firm’s predictions, through 2022, for residential and nonresidential building and nonbuilding structure construction put in place, both nationally and across nine geographic regions.

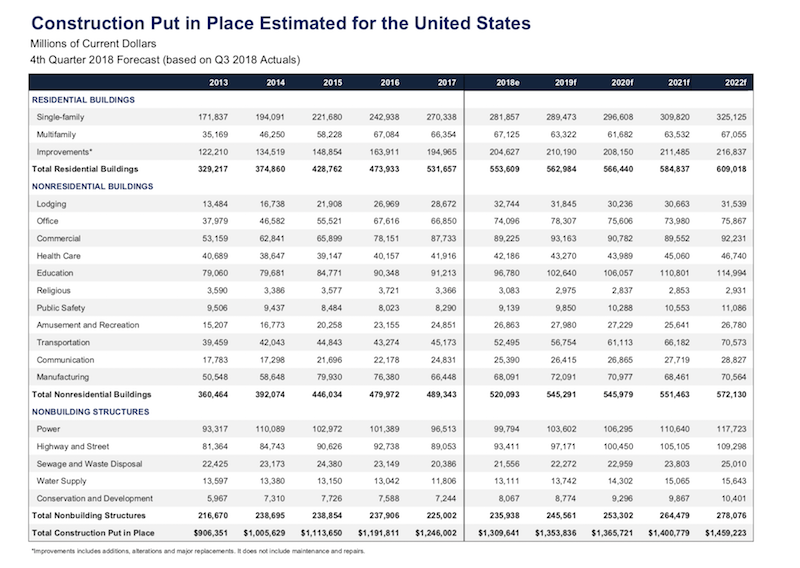

FMI projects U.S. construction spending for all sectors to hit $1.35 trillion in 2019, and to increase incrementally to $1.46 trillion in 2022. Spending for nonresidential buildings is projected to account for 40% of the total this year, and 39.2% of spending in 2022.

In FMI’s breakdown of spending by sectors, one of the biggest anticipated winners is transportation, which was up 16% last year, is expected to grow at the same percentage to $52 billion this year, and continue to rise annually by 2022, when FMI predicts 7% growth to $71 billion.

“Large airports all over the country are refocusing capital programs on the redesign of terminals and their amenities,” FMI writes. And while several mega transit projects are expected to break ground in 2019, growing demand for new infrastructure and system maintenance, along with increasing construction costs, is outweighing and outpacing growth in funding sources. This sector’s growth could also be adversely impacted by “political uncertainty.”

FMI reports more winners than losers in engineering and constuction spending in 2018. Image: FMI

FMI reports more winners than losers in engineering and constuction spending in 2018. Image: FMI

Construction spending for amusements and recreation was up 8% last year, and should rise by the same percentage in 2019 to $28 billion. FMI expects a downturn in the following two years, with spending leveling off at $27 billion in 2022. Several big-budget stadiums, arenas, and amusement parks have been active through 2018, with several more expecting to break ground in 2019. Casino construction, on the other hand, is expected to plateau and ultimately slow in the coming years.

Lodging, which at plus 14% was one of the industry’s genuine growth sectors last year, will be down this year and next, by FMI’s calculations, and even out in 2021 and 2022 to $32 billion.

Among the bigger-ticket sectors, office spending, which rose by 11% last year to $74 billion, will be up this year again by 6% to $78 billion in 2019, decline over the following two years, and stabilize at 3% growth to $76 billion in 2022. Suburban and rural project activity has progressively slowed of late.

This graph charts FMI's projections for compound annual growth rates for residential, nonresidential, and nonbuilding structure sectors. Image: FMI

This graph charts FMI's projections for compound annual growth rates for residential, nonresidential, and nonbuilding structure sectors. Image: FMI

Education was up last year by 6% and should rise at that same pace this year to $103 billion. By 2022, spending in this sector could hit $115 billion. FMI points out that within higher education, tuition revenue growth in private schools (led by larger comprehensives) is expected to nearly double the revenue growth seen at public institutions.

As the shift from bricks and mortar retailing to ecommerce marches forward unabatedly, spending for commercial projects is projected to grow 4% to $93 billion this year, but also decline over the next two years, and then even out to $92 billion in 2022.

The manufacturing sector will be stable this year, down the next two years, and stable again in 2022, when FMI sees spending growth at 3%. But FMI also worries about volatility in manufacturing construction if the Trump administration continues to use tariffs to achieve its policy objectives.

FMI’s report also provides sector breakdowns for non-building structures and residential. It notes, for example, that multifamily construction in the U.S., which for much of the past decade drove the housing industry, plateaued toward the end of 2018. Declining investment is expected through 2019 and 2020, although this trend should vary regionally. Going into 2019, as an increasing number of markets recognize oversupply, rents are expected to decline and starts will taper.

Last year there were over 400 mergers and acquisitions of engineering or construction firms announced or closed, a 33% increase over 2017. But in 2019 and beyond, FMI expects buyers to be more cautious, or at the very least more selective.

FMI anticipates more investment activity for construction technology, which over the past decade has attracted in excess of $10 billion. But FMI also warns “while many of today’s construction tech startups may be in growth mode right now, E&C is an unpredictable sector. Where venture capital firms may be involved with it during the ‘boom’ times, the real test comes with E&C startups must maintain growth during a downturn. That’s where the rubber meets the road, and it’s a scenario we could be experiencing sometime in the next 12 to 24 months.”

Related Stories

Market Data | Nov 27, 2023

Number of employees returning to the office varies significantly by city

While the return-to-the-office trend is felt across the country, the percentage of employees moving back to their offices varies significantly according to geography, according to Eptura’s Q3 Workplace Index.

Market Data | Nov 14, 2023

The average U.S. contractor has 8.4 months worth of construction work in the pipeline, as of September 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator declined to 8.4 months in October from 9.0 months in September, according to an ABC member survey conducted from Oct. 19 to Nov. 2. The reading is down 0.4 months from October 2022. Backlog now stands at its lowest level since the first quarter of 2022.

Multifamily Housing | Nov 9, 2023

Multifamily project completions forecast to slow starting 2026

Yardi Matrix has released its Q4 2023 Multifamily Supply Forecast, emphasizing a short-term spike and plateau of new construction.

Contractors | Nov 1, 2023

Nonresidential construction spending increases for the 16th straight month, in September 2023

National nonresidential construction spending increased 0.3% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.1 trillion.

Market Data | Oct 23, 2023

New data finds that the majority of renters are cost-burdened

The most recent data derived from the 2022 Census American Community Survey reveals that the proportion of American renters facing housing cost burdens has reached its highest point since 2012, undoing the progress made in the ten years leading up to the pandemic.

Contractors | Oct 19, 2023

Crane Index indicates slowing private-sector construction

Private-sector construction in major North American cities is slowing, according to the latest RLB Crane Index. The number of tower cranes in use declined 10% since the first quarter of 2023. The index, compiled by consulting firm Rider Levett Bucknall (RLB), found that only two of 14 cities—Boston and Toronto—saw increased crane counts.

Market Data | Oct 2, 2023

Nonresidential construction spending rises 0.4% in August 2023, led by manufacturing and public works sectors

National nonresidential construction spending increased 0.4% in August, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.09 trillion.

Giants 400 | Sep 28, 2023

Top 100 University Building Construction Firms for 2023

Turner Construction, Whiting-Turner Contracting Co., STO Building Group, Suffolk Construction, and Skanska USA top BD+C's ranking of the nation's largest university sector contractors and construction management firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all university/college-related buildings except student residence halls, sports/recreation facilities, laboratories, S+T-related buildings, parking facilities, and performing arts centers (revenue for those buildings are reported in their respective Giants 400 ranking).

Construction Costs | Sep 28, 2023

U.S. construction market moves toward building material price stabilization

The newly released Quarterly Construction Cost Insights Report for Q3 2023 from Gordian reveals material costs remain high compared to prior years, but there is a move towards price stabilization for building and construction materials after years of significant fluctuations. In this report, top industry experts from Gordian, as well as from Gilbane, McCarthy Building Companies, and DPR Construction weigh in on the overall trends seen for construction material costs, and offer innovative solutions to navigate this terrain.

Data Centers | Sep 21, 2023

North American data center construction rises 25% to record high in first half of 2023, driven by growth of artificial intelligence

CBRE’s latest North American Data Center Trends Report found there is 2,287.6 megawatts (MW) of data center supply currently under construction in primary markets, reaching a new all-time high with more than 70% already preleased.